Average KiwiSaver Balance by Age - What You Need to Know

Explore the latest data on KiwiSaver balance by age and understand why there's a risk that the balances may be insufficient for a comfortable retirement.

Updated 10 August 2023

Summary:

Our guide covers:

- As the financial strain on Kiwi households grows with record-breaking inflation and higher mortgage interest rates, many New Zealanders resort to pausing or withdrawing funds (via hardship) from their KiwiSaver accounts to cover essential living costs.

- While the increasing cost of living is a concern for almost everyone, how Kiwis deal with these rising costs can significantly affect our retirement years.

- For many New Zealanders grappling with these economic conditions, saving for retirement is likely to be a distant thought. However, for these Kiwis, securing their retirement savings shouldn't be shelved indefinitely. With declining rates of home ownership in younger generations and lower KiwiSaver balances across the board, young Kiwis might struggle to benchmark their own KiwiSaver balance with what others in their peer/age group are at.

- This guide has been published to make sense of government-sourced data and present it in a way to help every New Zealander make an informed investing decision.

Our guide covers:

- Why Does this KiwiSaver Analysis and Review Exist? What are the Key Findings?

- How Many KiwiSaver Members are there in New Zealand?

- What’s the Average KiwiSaver Balance for the Typical New Zealander?

- Must-Know Facts About KiwiSaver Segmented By Age

- Frequently Asked Questions Related to KiwiSaver Balances by Age

Know This First: What is KiwiSaver? What are the basics of it? How does it work?

KiwiSaver is designed for New Zealand citizens and permanent residents, with enrolment available from birth. When an eligible individual starts a new job, they're automatically enrolled in KiwiSaver, although they can opt out within a specified period. Members can choose between several KiwiSaver providers, each offering a range of funds to invest in. A few key characteristics of KiwiSaver include:

Contributions

Employers must contribute at least 3% to their employee's KiwiSaver account. Additionally, as of 2023, the government provides an annual member tax credit of up to $521.43 if the member contributes at least $1,042.86 during the year.

The Three Main Types of KiwiSaver Funds

KiwiSaver funds are typically designed with three risk/reward tolerances: growth, balanced, and conservative. The growth stage aims for higher returns by investing in riskier assets (predominantly shares). The balanced stage provides a mix of growth and income assets, while the conservative stage focuses on preserving capital by investing in low-risk assets like bonds and cash.

Retirement Withdrawal

KiwiSaver funds can be accessed when a member reaches the age of eligibility for New Zealand Superannuation, currently at 65 years. Members can withdraw their funds as a lump sum or in regular payments to supplement their retirement income. However, there are certain situations where Kiwis can withdraw their KiwiSaver early.

More details:

Contributions

Employers must contribute at least 3% to their employee's KiwiSaver account. Additionally, as of 2023, the government provides an annual member tax credit of up to $521.43 if the member contributes at least $1,042.86 during the year.

The Three Main Types of KiwiSaver Funds

KiwiSaver funds are typically designed with three risk/reward tolerances: growth, balanced, and conservative. The growth stage aims for higher returns by investing in riskier assets (predominantly shares). The balanced stage provides a mix of growth and income assets, while the conservative stage focuses on preserving capital by investing in low-risk assets like bonds and cash.

Retirement Withdrawal

KiwiSaver funds can be accessed when a member reaches the age of eligibility for New Zealand Superannuation, currently at 65 years. Members can withdraw their funds as a lump sum or in regular payments to supplement their retirement income. However, there are certain situations where Kiwis can withdraw their KiwiSaver early.

More details:

MoneyHub Founder Christopher Walsh shares his views on KiwiSaver (and the low balances currently invested):

|

"Our number crunching is designed to make sense of where KiwiSaver (as a program) is at (and where it should be going). I make no apology about being pro-KiwiSaver: I believe it is the only tool to ensure New Zealanders are properly equipped for retirement. For this reason, I believe it should also be compulsory.

However, what matters is where things are now. The good news is that younger New Zealanders (Generation Z and Millennials) have a significant KiwiSaver membership, with the 18-25 age group leading the pack. However, I don't believe KiwiSaver delivers sufficient balances for a comfortable retirement. For example, the average balance for those aged 61-65 sits at around $54,000, arguably a small nest egg. Life expectancy in New Zealand is increasing, and there are potential discussions about extending the retirement age. Even if we don't see a change to 65, we need to prepare for a longer retirement and, therefore, more retirement savings. Most KiwiSaver balances are below the recommended amount for a comfortable retirement. The typical balance is below $60,000, but the recommended lump sum is upwards of $600,000 (as per Massey Research), so today's situation isn't good news. We're in a cost of living crisis - I believe those aged between 40 and 50 will face challenges in accumulating sufficient KiwiSaver savings for retirement due to high household expenses, rising interest rates, and having less time for compounding returns. It's never too late to double down on KiwiSaver contributions, but getting in early makes a difference. I'm pleased that the government is actively ensuring default KiwiSaver schemes encourage default fund members into more suitable funds. This means there's more hope for more young people to be in growth funds and, over time, maximise their balances. Ensuring the right fund allocation, consistent contributions, and taking advantage of employer and government contributions are essential strategies for optimising KiwiSaver benefits". |

Christopher Walsh

MoneyHub Founder |

Why Does this KiwiSaver Analysis and Review Exist? What are the Key Findings?

- New Zealand law requires, through the New Zealand Superannuation and Retirement Income Act 2001, that every three years, the Office of the Retirement Commissioner must conduct a Review of the Retirement Income Policies (also known as the RRIP). The most recent study was published in March 2022.

- According to a KiwiSaver Demographic Study conducted by Financial Advisor Melville Jessup Weaver (which was commissioned by the Government Retirement Commission - known as Te Ara Ahunga Ora), the average KiwiSaver balance is $29,022 (as of the 31 December, 2021).

Disclosures on the MJW Study:

- This guide draws heavily from the Melville Jessup Weaver (MJW) study, one of the most recent comprehensive studies analysing KiwiSaver balances and demographics.

- However, despite MJW analysing a large sample size (almost 3 million KiwiSaver members), potential biases in the results may exist. Results should be interpreted with this in mind. The MJW study focused on average KiwiSaver balances. Averages tend to heavily skew graphs to the left or right (left-tailed or right-tailed). For example, average wealth or net worth balances tend to skew heavily to the right (right-tailed) due to the small percentage of people with outsized wealth or net worth (usually due to inheritances or other specific events).

- The MJW study was based on survey data and will come with all the usual caveats when extrapolating from surveys. Note that the data below may not reflect actual KiwiSaver balances.

- The data referenced in this guide isn’t intended to provide a full picture of everything related to KiwiSaver. Specifically, the MJW study should serve as a useful starting point for financial/saving discussions and prompt Kiwis to consider their desired lifestyle post-retirement and whether their current KiwiSaver investment strategy will get them close enough to support that lifestyle.

- Where possible, MoneyHub has attempted to show all sources.

- Small discrepancies in the MJW dataset may exist as the gender of some members was not disclosed. For example, MJW data sometimes excluded members of unknown gender (see the MJW study methodology for more info).

- KiwiSaver has only been around for 16 years (14 years from when the MJW survey was conducted), so this may be a potential reason why balances for older Kiwis are not as large as you would expect under traditional retirement/pension savings schemes (like those in the United States or the United Kingdom).

- MoneyHub has removed the 80+ age cohorts from the analysis below as the sample sizes were disproportionately smaller than other age brackets.

- All $ figures are in New Zealand Dollars unless stated otherwise.

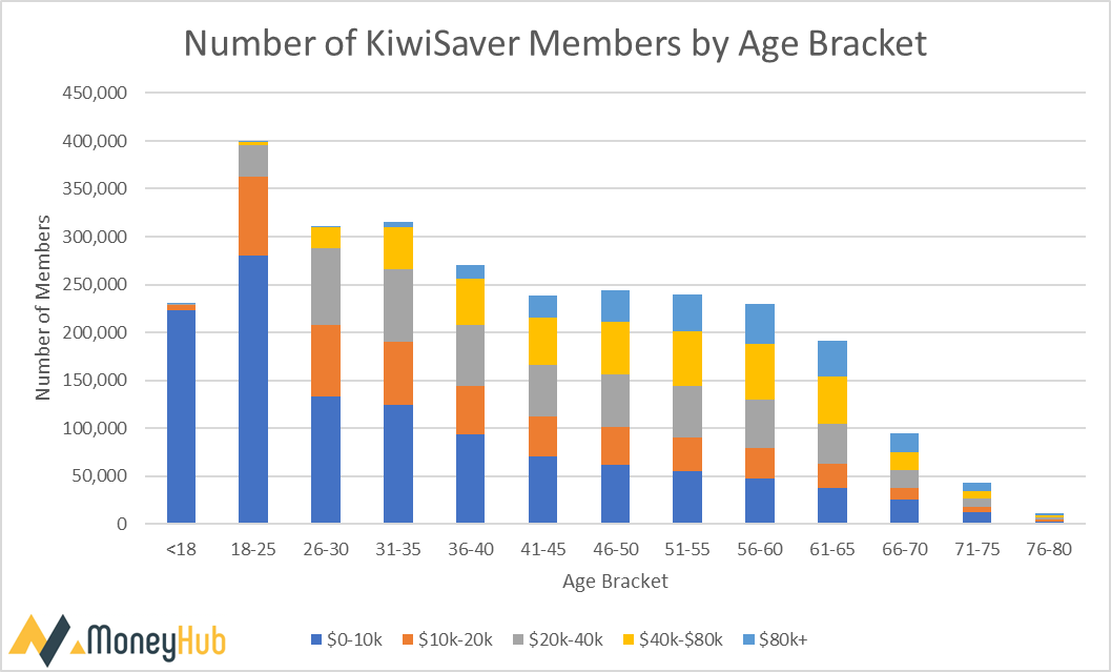

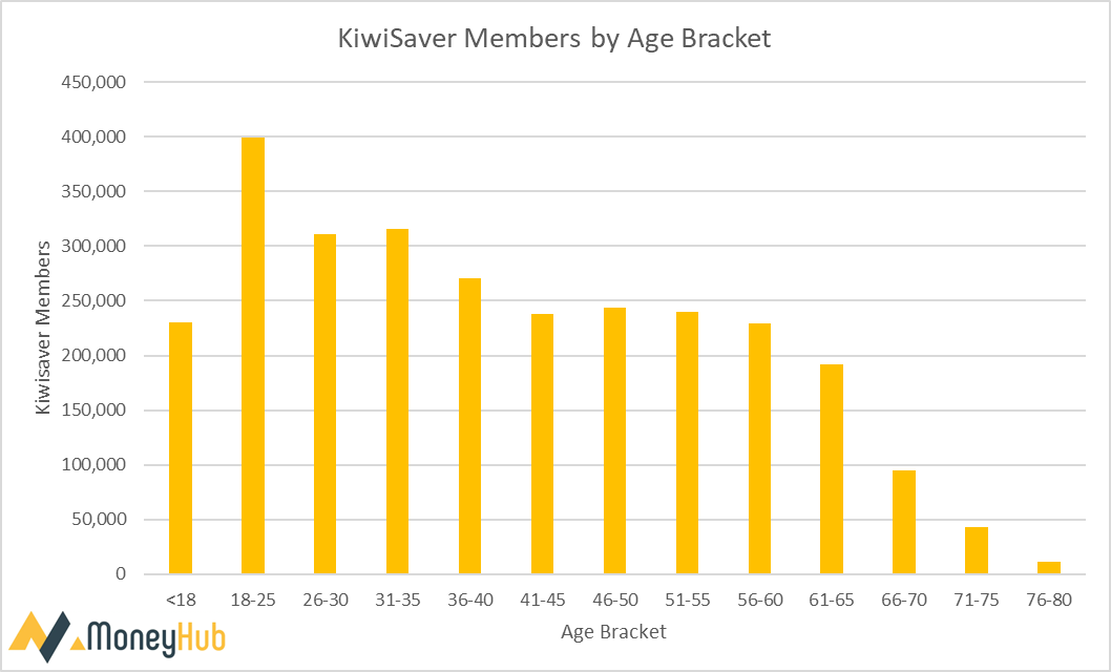

How Many KiwiSaver Members are there in New Zealand?

Source: MJW Study and MoneyHub Analysis

From the graphs above, a few insights can be observed:

From the graphs above, a few insights can be observed:

- The age group with the highest KiwiSaver membership is 18-25 (Generation Z). This cohort has around 400,000 members, or 14% of all enrolled KiwiSaver members. The second largest age cohort is the 31-35 age bracket (Millennials). Beyond this, the distribution of members remains relatively flat/even.

- The number of KiwiSaver members that still have their money in the KiwiSaver scheme once they’re eligible to withdraw it (aged 65+) drops drastically, indicating that almost all Kiwis withdraw their KiwiSaver balances (or unfortunately pass away) between the decade-long period of 65 to 75 years old.

- Approximately 153,000 members, equating to around 5.2% of the total, are over 65 and appear to be utilising KiwiSaver as an investment tool during retirement (rather than cashing it out).

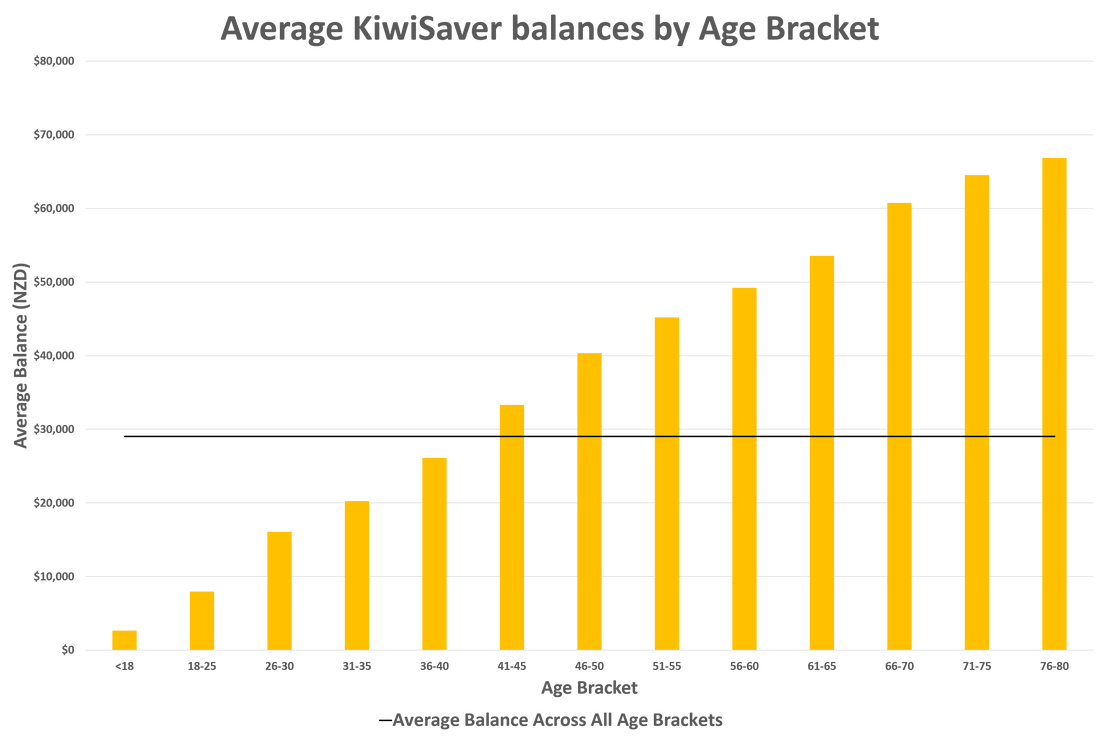

What’s the Average KiwiSaver Balance for the Typical New Zealander?

Source: MJW Study and MoneyHub Analysis.

From the above graph, a few insights can be observed:

From the above graph, a few insights can be observed:

- As you would expect, their KiwiSaver balances also grow as Kiwis get older. The largest percentage change between age cohorts happens earlier in life (for example, balances roughly double from 18 - 25 and 26 - 30). This would make sense, given lower balances compared to older Kiwis.

- The average KiwiSaver balance for those in the 61-65 age bracket (just before the retirement age of 65, where Kiwis can withdraw their KiwiSaver) is around $54,000.

- Those that haven't cashed out after age 65 (when you're eligible to withdraw) have the largest balances (likely because these individuals have had longer to compound their wealth).

- Those that don't withdraw their KiwiSaver after 65 may still view their KiwiSaver as a wealth-building vehicle and may still be contributing to their KiwiSaver (even if they aren't receiving the government contribution), hence why the balances are so much larger.

- The average KiwiSaver balance across all age cohorts is around $30,000.

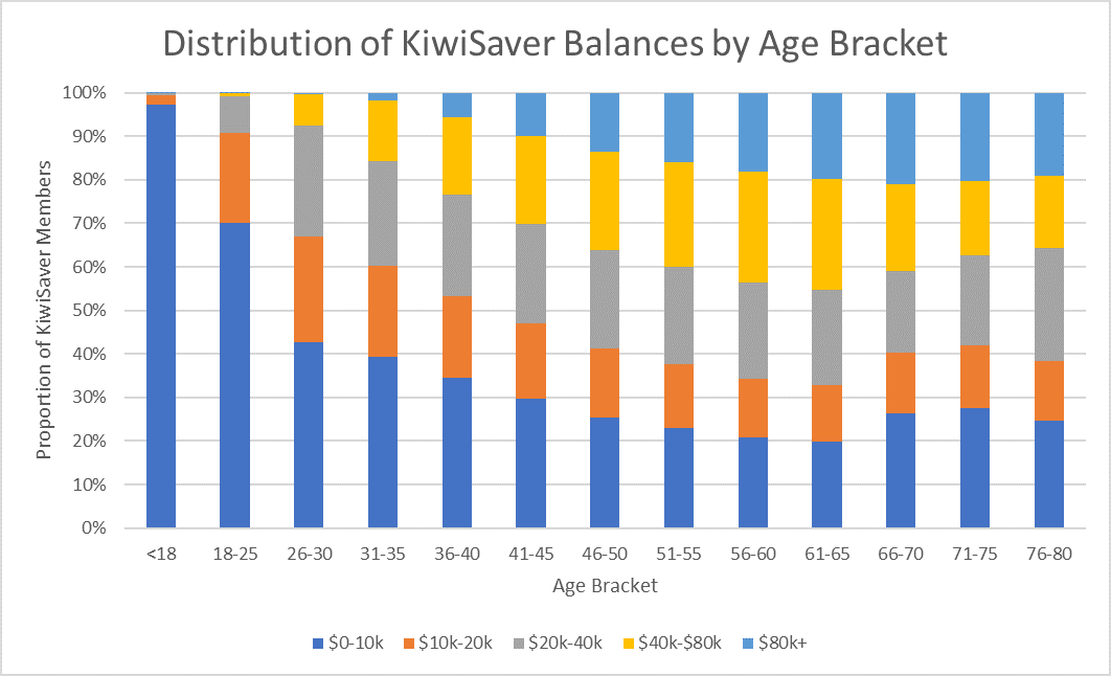

What's the KiwiSaver Balance of Someone in My Age Bracket?

Source: MJW Study and MoneyHub Analysis.

This graph shows the distribution of KiwiSaver balances among each age bracket. Key insights from the above include:

Further insights:

Two other key pieces of information were presented in the MJW study:

This graph shows the distribution of KiwiSaver balances among each age bracket. Key insights from the above include:

- Over 95% of KiwiSaver Members younger than 18 have less than $10,000.

- 70% of KiwiSaver members aged 18-25 have less than $10,000.

- Around 20% of KiwiSaver Members in the 56 - 80 age range have $80,000+.

- Almost all KiwiSaver members younger than 30 years old (with over 900,000 members in this age cohort) have KiwiSaver balances of less than $40,000.

Further insights:

Two other key pieces of information were presented in the MJW study:

- Roughly 40% of members hold less than $10,000 in their accounts (approximately 1.2 million out of the 2.8 million KiwiSaver members). In other words, don't feel discouraged if your KiwiSaver balance is <$10,000 - almost half of all Kiwis are in the same situation as you.

- Balances for Kiwis aged 80+ were significantly higher than those <80. For example, average balances for KiwiSaver members older than 80 years old were >$200,000 compared to around $60,000 for the 65 - 80 age range. This is likely attributable to survivorship bias. In other words, Kiwis <80 years old withdraw their KiwiSaver balances, and the Kiwis 80+ that chose not to withdraw their KiwiSaver balances are all left. Kiwis aged 80+ might not have needed to withdraw their KiwiSaver because they had other savings to draw down on and didn't need the cash, or they wanted to let their KiwiSaver balances grow and compound.

Must-Know Facts About KiwiSaver Segmented By Age

Important: Comparison is the thief of joy. Don’t fret if your KiwiSaver Balance is lower than the average for your age bracket.

Our view:

Differences between your KiwiSaver balance and the average for your age range based on the graph can potentially be attributed to several factors, including:

Remember that KiwiSaver is just one way for you to build your wealth. KiwiSaver is almost always a secondary wealth generation vehicle for Kiwis (compared to home ownership, brokerage investing or Term Deposits).

To help make sense of our KiwiSaver balance-by-age analysis, our must-know facts and figures are as follows:

Our view:

- While it can be useful to check in on how you're doing relative to some benchmark (other Kiwis, medians, averages, etc.) to maintain motivation, the best person you should compare yourself to is you yesterday, not other Kiwis today.

- While it can be useful to understand what other Kiwis in similar situations earn (to ensure you're not getting underpaid), every person will be in a unique financial situation.

- If comparisons to others are only causing you anxiety and stress, try to focus on comparing yourself to yourself from a few years ago rather than others.

- Try not to be discouraged when comparing your KiwiSaver balance to others. It doesn't mean you're worse off if you've got a lower KiwiSaver balance than the average displayed in the graphs above. There is a number of reasons why your numbers could be different from the balances displayed:

- You contributed a higher or lower percentage (e.g. 3% vs 5% vs 8% vs 10%) during your career.

- Your employer contributed the bare minimum of 3% (compared to other employers who may match a higher matching KiwiSaver rate).

- You decided to invest in a different investment vehicle (such as a house, share investing platform or term deposit) to grow your wealth outside of KiwiSaver.

Differences between your KiwiSaver balance and the average for your age range based on the graph can potentially be attributed to several factors, including:

- Withdrawals for first home deposits

- Withdrawals for hardship

- Savings suspensions

- Taking out your KiwiSaver due to moving abroad (then returning to New Zealand and restarting contributions)

- Kiwis may not have been participating in the scheme for the 14 years it has been accessible

Remember that KiwiSaver is just one way for you to build your wealth. KiwiSaver is almost always a secondary wealth generation vehicle for Kiwis (compared to home ownership, brokerage investing or Term Deposits).

To help make sense of our KiwiSaver balance-by-age analysis, our must-know facts and figures are as follows:

1. Prepare to need more KiwiSaver funds to pay for your retirement (when you eventually hit retirement age):

Kiwis live longer than ever before, with current life expectancy in New Zealand at just over 82 years (and young Kiwis in the Generation Z or Millennial age brackets are likely to live even longer than that). However, it's also likely that the retirement age of 65 will get pushed out when young Kiwis ultimately hit retirement age. For instance, some politicians have suggested pushing the retirement age to 67 as outlined in this May 2023 Stuff article . Both of these points mean younger Kiwis will likely live longer than ever and need more money to fund their retirement.

2. Kiwis in the 40 - 50 age bracket may be the most challenged age cohort (from a KiwiSaver perspective):

- The data suggests that Kiwis in their 40s might have difficulty putting away enough KiwiSaver savings for retirement.

- Kiwis in their 40s typically deal with high household expenses, with children at home and, if they're homeowners, rising interest rates on their mortgage payments.

- If they're renters, their rent is likely increasing (coupled with rising food inflation).

- This group also has less time to benefit from KiwiSaver's compounding returns before retirement compared to younger cohorts in their 20s or 30s.

3. Most KiwiSaver balances are significantly lower than the suggested amount for a comfortable retirement:

Most KiwiSaver balances across age cohorts <65 average less than $60,000. This figure is well below the New Zealand Retirement Expenditure Guidelines set out by Massey University, which recommends a $600,000 lump sum for a single-person household to live comfortably and have options in retirement in a metropolitan city. The recommended lump sum increases to $688,000 for a comfortable lifestyle in the provinces (according to the Massey University report).

4. It's common for Kiwis to "let their KiwiSaver ride" after age 65:

According to ANZ's research division, 71% of individuals who turned 65 in the year leading up to April did not withdraw any funds from their KiwiSaver account. Meanwhile, 17% partially withdrew, and 12% withdrew their entire savings.

5. Regardless of how distant retirement might seem, it’s extremely important to plan your retirement:

The current pressure on many Kiwi households due to rising living costs is not to be overlooked. However, there are a few steps Kiwis can take to better prepare for their future whilst ensuring stability in the present:

- Ensure you’re enrolled in the right fund that aligns with your age and risk profile.

- Aim to contribute as regularly as you can (without sacrificing the standard of living in the present).

- Take full advantage of any company matching (especially if your company offers >3% match).

- Don’t miss out on the yearly government contribution.

6. Overseas countries with higher savings rates are likely to have far higher retirement balances:

While we can't go back in time to introduce KiwiSaver in the early 1990s like Australia did with their superannuation, increasing the base savings rate from 3% could be beneficial. Australians have a far higher mandatory contribution (and employer match) rate, which is currently set at 10.5% but is set to increase to 12% in 2025. Additionally, Australia's superannuation system is mandatory for all Australians (compared to the optional "opt-out" for KiwiSaver.

7. Don't be disheartened if you're below your age bracket's average KiwiSaver balance:

Just because your KiwiSaver balance varies from the averages in this guide doesn't mean you're on the wrong track. However, suppose you feel you're not keeping up with peers in your same age bracket and want to grow your KiwiSaver balance faster. In that case, it may be helpful to consider increasing the amount you contribute to your KiwiSaver, changing industries or jobs to get a higher salary, or picking up a side hustle to increase your income.

For a deeper dive into these areas, check out our definitive guides:

For a deeper dive into these areas, check out our definitive guides:

Frequently Asked Questions Related to KiwiSaver Balances by Age

How much should I have in my investment or KiwiSaver accounts at different ages?

While there's no one-size-fits-all answer, the following milestones can serve as a general guideline for retirement or investment balances at different ages:

- Age 30: Aim to have at least the equivalent of your annual salary (1x) saved in your KiwiSaver/investment accounts. This will help you build a strong foundation for future savings and investment growth. For example, if you earn $60,000 a year, having $60,000 saved across your KiwiSaver and Sharesies/Stake accounts is a good rule of thumb.

- Age 40: Target a balance of about three times your annual salary (3x). By this stage, your KiwiSaver/investment accounts should have had ample time to grow and snowball.

- Age 50: Aim for a balance of approximately six times your annual salary (6x). As you approach retirement, you may want to adjust your investment strategy further to protect your savings and prepare for a steady income stream (in other words, reallocate your investments to more defensive assets like bonds or term deposits).

- Age 60: Save around ten times your annual salary (10x). This will help ensure you have sufficient funds to maintain your lifestyle during retirement. For example, if you make a $60,000 salary a year, saving $600,000 to supplement NZ Super will likely be sufficient for retirement (as per the New Zealand Retirement Expenditure Guidelines).

How can I increase my KiwiSaver savings?

There are several ways to increase your KiwiSaver savings:

- Increase your contribution rate: Boosting your contribution rate from a minimum of 3% to a higher percentage, such as 4%, 6%, 8% or 10%, can significantly impact your savings over time - you can see how this affects your after-tax earnings by using our PAYE calculator. Evaluate your financial situation and determine how much you can comfortably contribute without compromising your current lifestyle.

- Make voluntary contributions: Besides your regular contributions, consider making voluntary lump-sum payments or adding regular additional contributions. This will help accelerate your savings growth and take advantage of compounding.

- Choose the right fund: Ensure that your chosen fund aligns with your risk tolerance and investment goals. Periodically review your fund's performance and assess whether it suits your needs.

- Maximise government incentives: Contribute at least $1,042.86 per year to your KiwiSaver account to receive the maximum annual member tax credit of $521.43.

Can I access my KiwiSaver funds in case of financial hardship?

In certain circumstances, you may be able to access your KiwiSaver funds if you're experiencing significant financial hardship. To qualify, you must demonstrate that you cannot meet essential living expenses, mortgage repayments on your principal family residence, or the cost of medical treatment for yourself or a dependent.

To access your KiwiSaver funds due to financial hardship, you'll need to apply to your KiwiSaver provider, who will assess your application based on the criteria set by the government. Remember that the withdrawal amount will be limited to the minimum required to alleviate your hardship.

To access your KiwiSaver funds due to financial hardship, you'll need to apply to your KiwiSaver provider, who will assess your application based on the criteria set by the government. Remember that the withdrawal amount will be limited to the minimum required to alleviate your hardship.