How Aggressive Should My KiwiSaver Be? The Definitive Guide to a Common Question

An aggressive KiwiSaver fund isn't a one-way ticket to prosperity, nor is a conservative fund the universal path to security - our guide reveals everything you need to know to choose the right KiwiSaver fund for your needs.

Updated 10 November 2023

Introduction

Our Guide Covers:

MoneyHub Disclosures:

- While most New Zealanders know that it’s extremely important to save for retirement, and the KiwiSaver scheme is a huge portion of that, many are far less sure what type of fund they should be invested in (especially relative to their age or risk appetite).

- Words like "aggressive", "conservative", and "balanced" are thrown around, but these are extremely broad terms and don't help to describe what the fund is made up of. What's considered "aggressive" to one New Zealander may be completely different from another’s view of "aggressive".

- Choosing the right level of aggressiveness for your KiwiSaver fund is a blend of understanding your financial goals, recognising your risk tolerance, and grasping market dynamics. It's not a 'set and forget' decision. Additionally, it can significantly impact the volatility of your KiwiSaver portfolio and the ultimate size of your nest egg when you hit retirement age. In that sense, your fund type is essential.

- Helpfully, the New Zealand Retirement Commission has outsourced analysis to an external consultant to generate key insights and shed some light on how New Zealanders position their KiwiSaver investments.

Our Guide Covers:

- What Are the Main Types of Kiwisaver Funds?

- What Type of Fund is the Typical New Zealander Invested In?

- Understanding the Gap Between Men and Women’s KiwiSaver Balances

- Must-Know Facts and Considerations about KiwiSaver and Risk

- Frequently Asked Questions Related to KiwiSaver Aggressiveness

MoneyHub Disclosures:

- This page extensively references the MJW report, a prominent and detailed recent examination of KiwiSaver account statistics and member demographics.

- The MJW report utilised data samples and, as with any conclusions drawn from sample surveys, comes with caveats and limitations when trying to generate insights.

- The information in this resource isn't designed to provide an exhaustive overview of KiwiSaver-related matters. Rather, the findings from the MJW report are intended to act as a foundational reference for starting conversations about finances, allocations and risk appetite.

- MoneyHub has included commentary on an example of what might be the optimal fund type for each age range or bracket. Note that this is MoneyHub’s opinion only and is not a substitute for financial advice. There’s no “right answer” for which fund you should be in, but based on the analysis below, we’ve lightly recommended what might make sense given the conclusions that MJW has drawn.

- Where possible, MoneyHub has attempted to show all sources.

- All dollar figures are in New Zealand Dollars unless stated otherwise.

MoneyHub Founder Christopher Walsh discusses the importance of aligning KiwiSaver fund aggressiveness with personal financial goals:

|

"In my conversations with KiwiSaver members, a common theme surfaces: the challenge of choosing a fund that makes sense. It's not merely about age, being conservative, or being aggressive; it's about aligning with your life's financial needs and demands.

An aggressive KiwiSaver fund isn't a one-way ticket to prosperity, nor is a conservative fund the universal path to security. Throughout 2023, we've seen significant shifts in the economy, impacting how Kiwis save for retirement. This will continue, hence my desire to publish this guide. As the founder of MoneyHub, my goal is to demystify these options. We distil the latest data, like the insights from the MJW report, into actionable knowledge. It's about informed choices – understanding your investment's potential highs and lows and how it fits within your unique financial landscape. The conversation around KiwiSaver fund aggressiveness is more relevant than ever. Economic headwinds have prompted many to question their current strategies, particularly given the declining balances and high-interest term deposits. Our guide is designed to bring clarity to these decisions. Remember, reviewing your KiwiSaver fund is not an admission of past mistakes; it's a proactive step towards future financial well-being. It's crucial to reassess periodically, ensuring your retirement savings work as hard as you do." |

Christopher Walsh

MoneyHub Founder |

What Are the Main Types of Kiwisaver Funds?

KiwiSaver funds are typically designed with four main risk/reward tolerances: conservative, moderate, balanced and growth:

- Conservative Fund: These funds primarily invest in fixed-interest assets, like bonds, with a smaller portion in shares. They aim for steady, moderate returns and are less vulnerable to market fluctuations. Conservative funds are ideal for those who prefer stability and are nearing retirement.

- Moderate Funds: A step up from conservative funds, these allocate a more significant portion to shares and property while maintaining a substantial portion in fixed-interest assets. They balance risk and return, making them suitable for individuals looking for moderate growth without excessive risk.

- Balanced Funds: Here, the investments are almost evenly distributed between growth assets (like shares and property) and income assets (like bonds and bank deposits). With moderate to high returns, balanced funds cater to individuals who are comfortable with medium levels of risk.

- Growth Funds: These funds primarily focus on growth assets, offering the potential for higher returns. However, they also come with higher volatility, making them suitable for those with a long-term investment horizon and a higher risk tolerance.

What is the MJW Study? What approach did MJW take in doing this study?

The Retirement Commissioner commissioned Melville Jessup Weaver (MJW) to gather comprehensive demographic data on the KiwiSaver program. MJW contacted various KiwiSaver providers to obtain consolidated data that reflects their scheme members' profiles.

These providers were requested to compile a straightforward spreadsheet outlining member account balances across different age and gender segments by fund type. The data collection occurred early in 2023 and reflects the status as of December 31, 2022.

While this is the first detailed analysis MJW has done, it follows two previous publications that reported on membership distribution by age and gender, using data snapshots from 2021 and 2022:

Limitations related to the MJW Study:

How was the MJW Detailed Demographic Study Set Up?

In MJW’s detailed demographic analysis, their main purpose was to explore the correlation between an individual’s age and the degree of investment risk they assume. To yield reliable and coherent findings, MJW has categorised ages and levels of investment risk into specific ranges. The criteria for these categorisations are outlined in subsequent sections.

To gauge the level of investment risk, MJW assessed the proportion of growth assets within a fund and then grouped funds with similar levels into defined ranges. MJW exercised their judgement to identify and segment these ranges, encompassing three additional categories beyond those recommended by the FMA’s guidelines for fund name classifications.

MJW Study Age Terminology:

These providers were requested to compile a straightforward spreadsheet outlining member account balances across different age and gender segments by fund type. The data collection occurred early in 2023 and reflects the status as of December 31, 2022.

While this is the first detailed analysis MJW has done, it follows two previous publications that reported on membership distribution by age and gender, using data snapshots from 2021 and 2022:

Limitations related to the MJW Study:

- The Inland Revenue Department (IRD) indicated there were a total of 3,249,512 KiwiSaver participants as of December 2022, suggesting the MJW 2023 study encompasses roughly two-thirds of the entire KiwiSaver membership. Although this constitutes a substantial sample, there is a potential for bias in the findings, and as such, caution is advised when interpreting these results.

- There were instances where gender data was not specified. Consequently, while the total figures presented in the MJW study account for members with unspecified or non-binary gender statuses, any gender-specific analyses exclude such data. For more information, see the MJW study methodology.

How was the MJW Detailed Demographic Study Set Up?

In MJW’s detailed demographic analysis, their main purpose was to explore the correlation between an individual’s age and the degree of investment risk they assume. To yield reliable and coherent findings, MJW has categorised ages and levels of investment risk into specific ranges. The criteria for these categorisations are outlined in subsequent sections.

To gauge the level of investment risk, MJW assessed the proportion of growth assets within a fund and then grouped funds with similar levels into defined ranges. MJW exercised their judgement to identify and segment these ranges, encompassing three additional categories beyond those recommended by the FMA’s guidelines for fund name classifications.

MJW Study Age Terminology:

Age Demographic |

Age Demographic Age Range |

Youth |

Between 0 and 30 years old. |

Middle Age |

Between 31 and 50 years old. |

Nearing Retirement |

Between 51 and 64 years old. |

Retired |

Sixty-five years old and above. |

Note: The terms selected by MJW were for descriptive purposes within the study only and are not intended to make assumptions about the individual circumstances of members within each group.

What Type of Fund is the Typical New Zealander Invested In?

Historically, many KiwiSaver members have been invested in conservative funds. Many members, especially those auto-enrolled when the programme first started, found themselves in default conservative funds.

However, as awareness about the KiwiSaver scheme grew, and people became more financially literate, there has been a gradual shift. Many New Zealanders now understand that moving to a fund better aligned with their age and risk appetite can offer better returns over the long term. Consequently, there's been a noticeable uptrend in investments in balanced and growth funds, especially among the younger demographic.

MJW Study Fund Allocation Methodology

For the study, MJW has classified funds into eight distinct types according to their target allocation towards growth assets, with designations as follows:

However, as awareness about the KiwiSaver scheme grew, and people became more financially literate, there has been a gradual shift. Many New Zealanders now understand that moving to a fund better aligned with their age and risk appetite can offer better returns over the long term. Consequently, there's been a noticeable uptrend in investments in balanced and growth funds, especially among the younger demographic.

MJW Study Fund Allocation Methodology

For the study, MJW has classified funds into eight distinct types according to their target allocation towards growth assets, with designations as follows:

Fund Type |

What % of the portfolio is in “growth assets”? |

Example age range recommendation from MJW |

Shares |

100% |

Youth |

Aggressive |

90 - 100% |

Youth |

Growth |

63 - 90% |

Youth |

Balanced |

50 - 63% |

Middle Age |

Moderate |

35 - 50% |

Middle Age |

Conservative |

10 - 35% |

Nearing retirement |

Defensive |

0 - 10% |

Nearing retirement |

Fixed Interest |

0% |

Retired |

Note 1: The above are approximations based on anecdotal recommendations, and MJW's categorisation reflects the funds' target asset allocation, which can sometimes differ significantly from their actual allocation at any given point.

Note 2: The ranges for each category are defined with a non-inclusive lower bound and an inclusive upper bound, except for the Aggressive category. For instance, a fund aiming for precisely 50% investment in growth assets falls under the Moderate category.

What are the top key points from the MJW Study?

However, this distinction doesn't necessarily indicate varying risk preferences. It might be influenced by the size of the KiwiSaver balance, with individuals holding smaller balances possibly opting for lower-risk funds.

Sources:

Note 2: The ranges for each category are defined with a non-inclusive lower bound and an inclusive upper bound, except for the Aggressive category. For instance, a fund aiming for precisely 50% investment in growth assets falls under the Moderate category.

What are the top key points from the MJW Study?

- Over a third (38%) of all managed funds are directed towards growth funds

For individuals below 50, around 50% of their investment balances are in growth funds. This ratio drops to 30% for those between 50 and 65 years of age and falls below 20% for those over 65. - Male KiwiSaver portfolios are more tilted to growth funds compared to females.

Women tend to invest more in conservative portfolios, whereas men lean more towards growth portfolios. The disparity is minor among the younger demographic but becomes more evident as they age.

However, this distinction doesn't necessarily indicate varying risk preferences. It might be influenced by the size of the KiwiSaver balance, with individuals holding smaller balances possibly opting for lower-risk funds.

Sources:

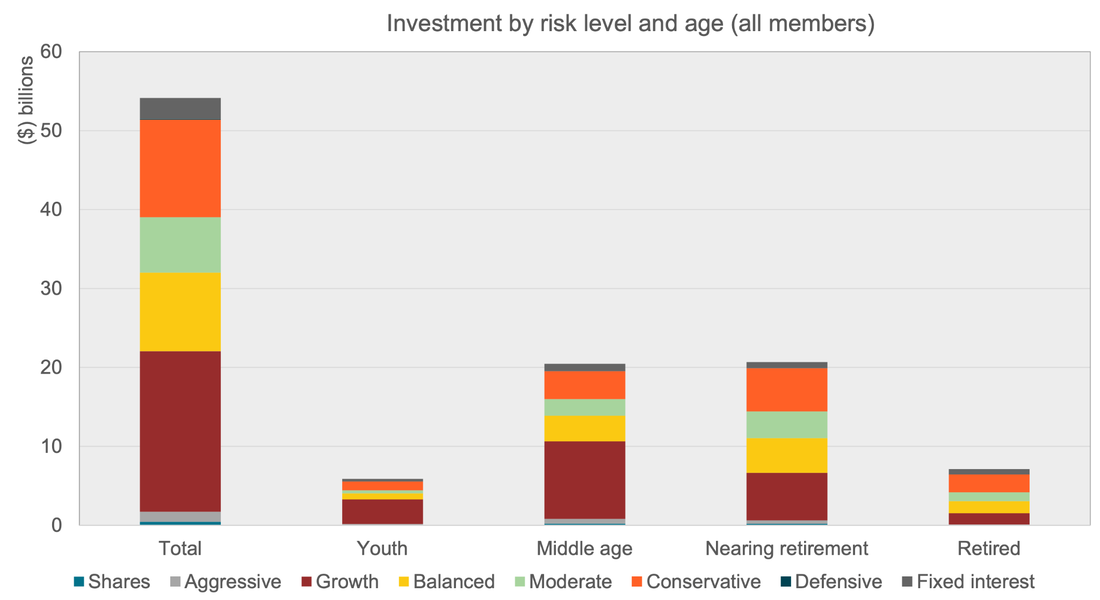

What’s the Total Amount of Money Invested for Each Age Cohort (Segmented by Fund Type)?

Source: MJW Detailed Demographic Study 2023 (Page 5)

Key Insights on Asset Distribution (e.g. who has all the KiwiSaver money?)

Regarding which type of KiwiSaver fund is most popular?

Notably, middle-aged members have the highest investments in these growth funds.

Key Insights on Asset Distribution (e.g. who has all the KiwiSaver money?)

- Of the total $55 billion of KiwiSaver assets under management by the managers who responded to MJW’s survey request, the majority of the funds in the KiwiSaver system belong to New Zealanders in their middle age (representing around $20 billion) and those approaching retirement (also representing $20 billion). Growth funds dominate total assets managed, surpassing $20 billion (38% of this study's total).

- This spread seems reasonable, given that these age groups represent most KiwiSaver members. Taking into account that KiwiSaver started around 14 - 16 years ago, it also makes sense that the New Zealanders who were young (who are now middle age) or the New Zealanders that were middle age (who are now nearing retirement age) have had the most exposure (and have likely been the ones who've consistently invested in KiwiSaver for the longest period compared to other age groups).

- Those who are retired and in their youth likely couldn't contribute for 14-16 years since the KiwiSaver programme was set up.

Regarding which type of KiwiSaver fund is most popular?

Notably, middle-aged members have the highest investments in these growth funds.

- Youth: With the smallest overall balance compared to the other age cohorts (around 5-7 billion compared to 20 billion for middle-aged and 20 billion for those close to retirement), it's unsurprising that most youth demographic is in growth funds. You would expect that with long-term investment runways of around 40 years, you would expect to see more young New Zealanders in growth funds.

- Middle age: Growth investments make up the bulk of middle-aged KiwiSaver members (which is completely reasonable given the long investment horizon). Interestingly, there are a significant number of middle-aged KiwiSaver investors who've invested in conservative funds (which predominantly hold cash and bonds). This may be a short-term market timing approach, but it also shadows a more worrisome thought that some middle-aged New Zealanders might be sitting in cash for over 20 years.

- Near Retirement: As you would expect, when individuals approach retirement age, investments in growth funds diminish, and conservative funds levels become more popular (but still only about a 1:1 ratio). Yet, even for those close to retirement, growth funds represent a significant portion of their balances. In other words, people still invest in more aggressive funds when they're "close to retirement". However, note that the "near retirement" bucket is a huge range from 1 to 15 years away from retiring. As such, someone who's 51 is still likely better off investing in more aggressive growth-type funds than more defensive, conservative funds.

- Retirees: The distribution across various fund types is most balanced among retirees. The conservative funds are the most popular among retirees, but there are still reasonable allocations to growth and moderate funds.

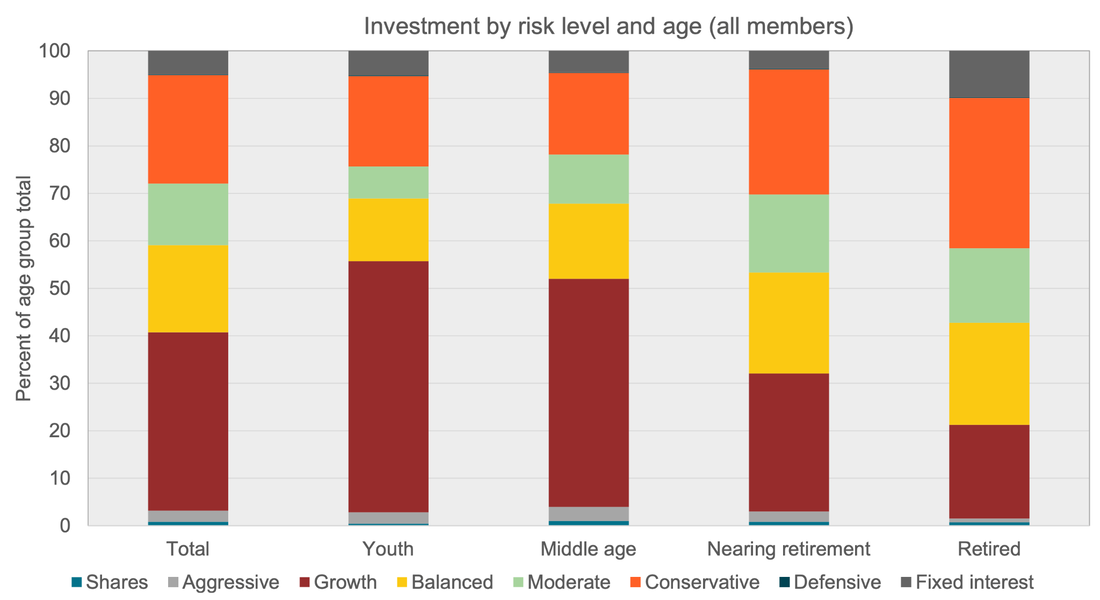

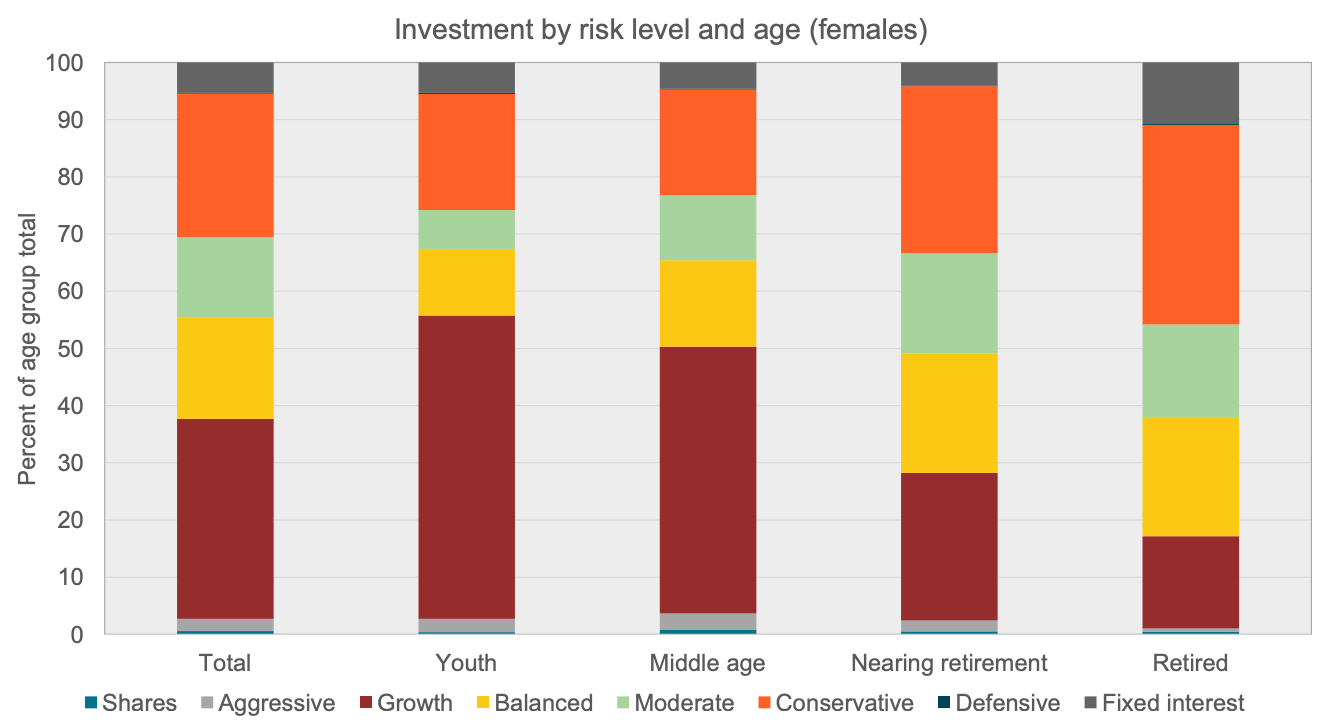

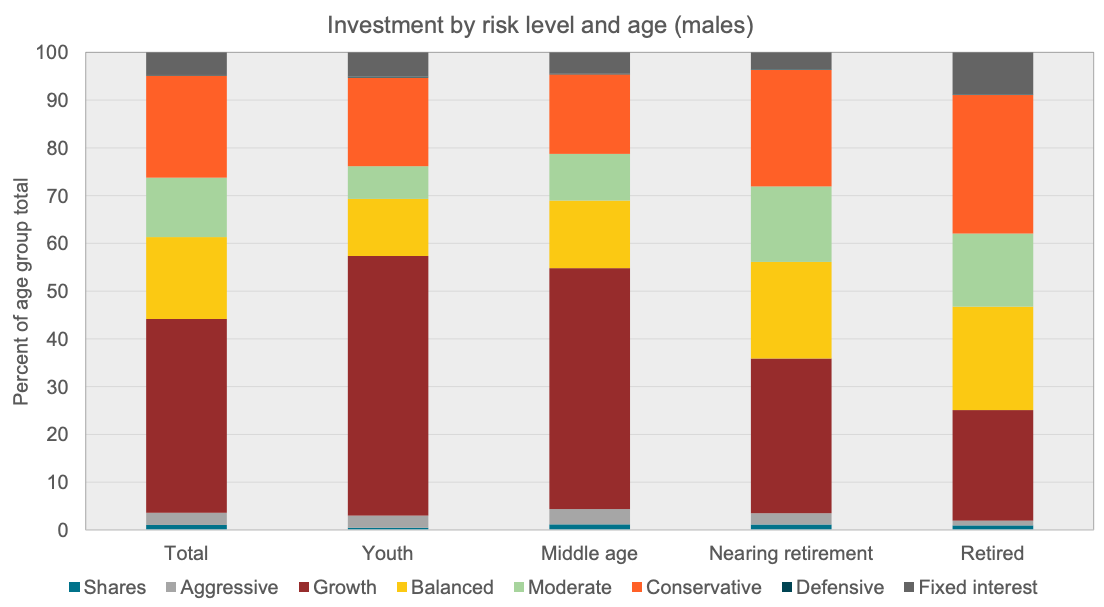

What’s the Split Between Different Fund Types for Each Age Cohort in New Zealand?

Source: MJW Detailed Demographic Study 2023 (Page 6).

A few interesting insights can be observed from the above graph:

A few interesting insights can be observed from the above graph:

- In line with predictions, the investment in growth assets tends to reduce as individuals age. This reflects the trend of "lifestyle", which is the gradual shift from equities to bonds as individuals near the retirement phase.

- Over 50% of the investment balances for younger and middle-aged members are in growth funds.

- The conservative fund type is the most popular fund type for those New Zealanders nearing retirement age or who are in active retirement.

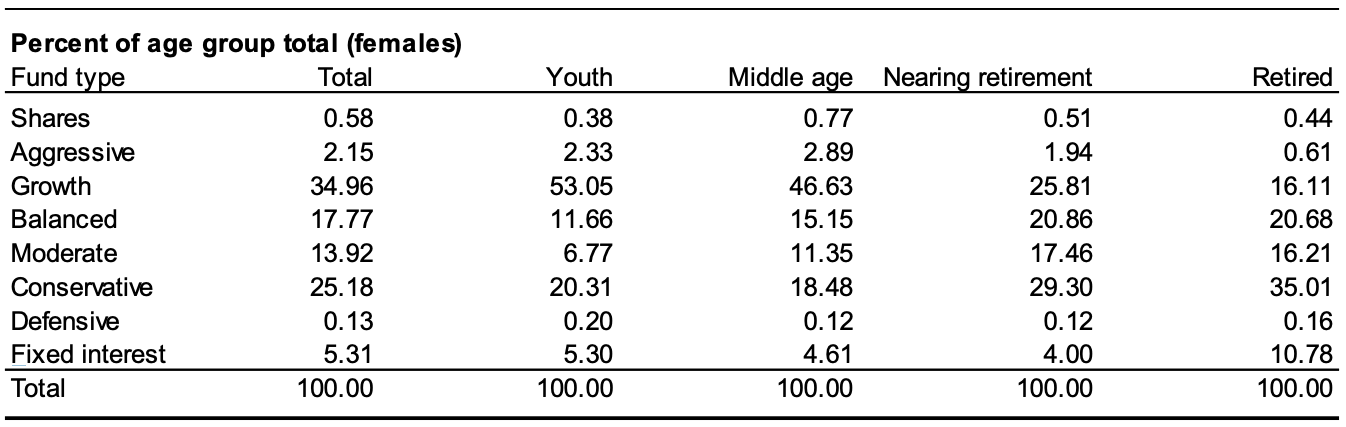

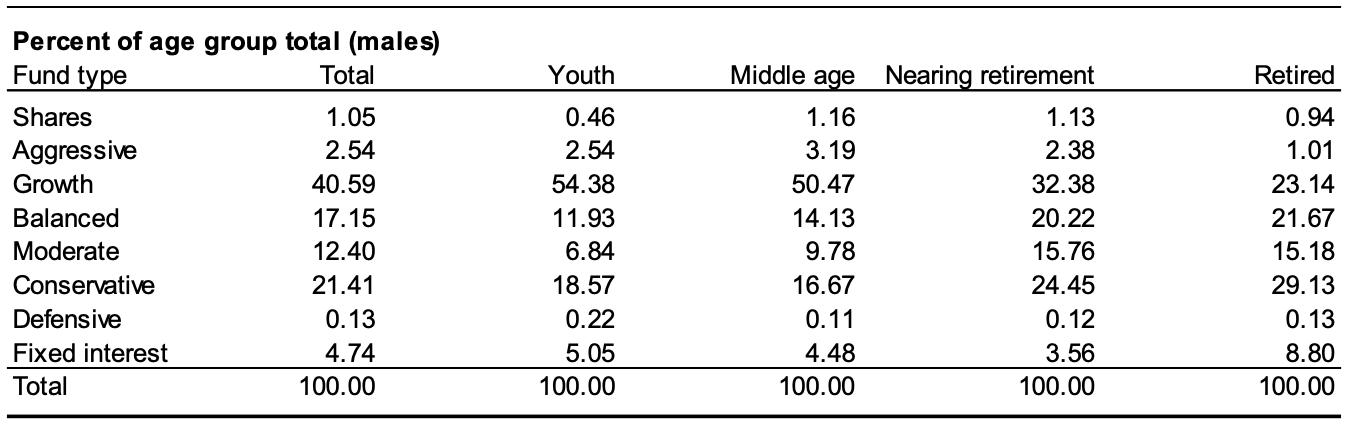

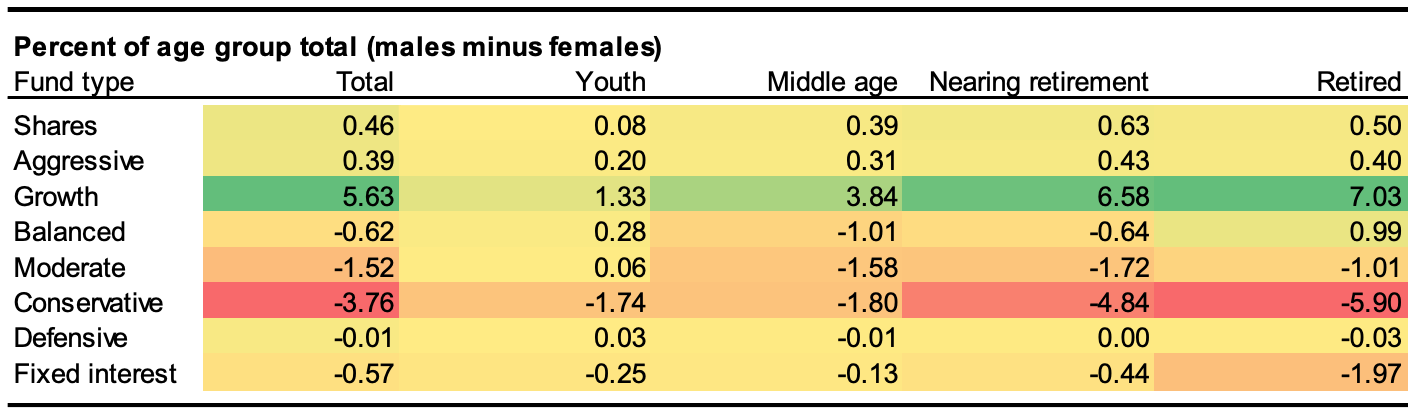

What is the Fund type split by age group and gender?

Source: MJW Detailed Demographic Study 2023 (Page 9).

How do I interpret the table above?

What are some of the key insights from the table above?

How do I interpret the table above?

- This section's analysis displays the disparities in proportions (males compared to females) across different age groups. A positive value (indicated with green) suggests a higher percentage of males in a specific cohort, while a negative value (shown in orange/red) indicates a higher percentage of females.

- As a practical example, the total % of male KiwiSaver member balances into growth funds is 40.59%, compared to female KiwiSaver member balances of 34.96% (source: MJW Study). The percentage difference between the male versus female proportion in growth is 5.63% (shown in bright green in the table above). This 5.63% is the gap in the proportion of male and female member balances within growth funds.

- As another example, male KiwiSaver member balances in conservative funds stand at 21.36% compared to female KiwiSaver balances at 25.12%. This -3.76% difference is displayed in the table's first column in bright red.

What are some of the key insights from the table above?

- Generally, there is a preference for more aggressive investment funds among males. A higher percentage of male balances is found in Shares, Aggressive, and Growth funds than females. In the youngest cohort, labelled "youth", the differences are minimal but seem to increase progressively with age.

- The most pronounced gender differences are observed in the older age brackets, where a larger proportion of investments by males stays in growth-oriented funds into their later years, in contrast to females who move their balances to more conservative funds. Numerically, there’s a >7% differential in the proportion of males investing in growth funds versus females investing in growth funds.

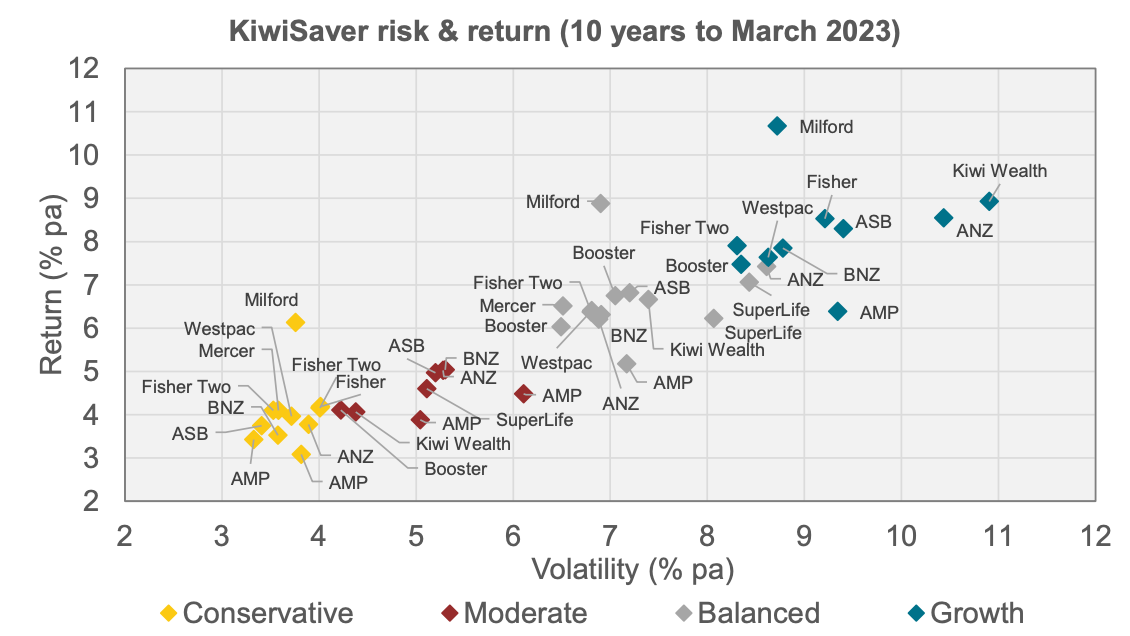

How have the different types of funds performed over the last decade?

Exhibit: Ten-Year Kiwisaver Returns and Volatility by Fund Type (Source: MJW 2023)

From the above graph, as anticipated, it can be seen that there's a direct correlation between risk (in this case, based on the volatility of the fund and underlying investments) and reward (in % return per year). More conservative funds tend to be steadier but yield lesser returns. Conversely, more aggressive funds have higher returns but are significantly more volatile.

It's quite clear from the graph above that for each of the main buckets (Conservative, Balanced and Growth), Milford is separated from the rest of the "pack" and has been able to successfully achieve higher returns with the same or slightly lower volatility compared to its peers over the last ten years. This isn't to say that Milford will continue to outperform relative to the risk it's taking, but just a factual data point from the graph above.

For more insights into Milford, check out our review of Milford’s KiwiSaver Plan.

From the above graph, as anticipated, it can be seen that there's a direct correlation between risk (in this case, based on the volatility of the fund and underlying investments) and reward (in % return per year). More conservative funds tend to be steadier but yield lesser returns. Conversely, more aggressive funds have higher returns but are significantly more volatile.

It's quite clear from the graph above that for each of the main buckets (Conservative, Balanced and Growth), Milford is separated from the rest of the "pack" and has been able to successfully achieve higher returns with the same or slightly lower volatility compared to its peers over the last ten years. This isn't to say that Milford will continue to outperform relative to the risk it's taking, but just a factual data point from the graph above.

For more insights into Milford, check out our review of Milford’s KiwiSaver Plan.

Understanding the Gap Between Men and Women’s KiwiSaver Balances

In the last few years, there has been recent headlines around the gender gap. The data shows that there is an evident widening gap between male and female KiwiSaver accounts, with recent statistics showing a 25% average difference in 2022, up from 20% the previous year (2021). This gap is growing across all age groups, particularly among younger members, suggesting long-term implications for women's retirement savings due to the effects of compound returns and interest.

While a more detailed investigation will need to be done to fully understand the gender gap in retirement savings, our take (based on the MJW studies) suggests there are five main reasons why the gender gap exists:

We explore these below in detail:

While a more detailed investigation will need to be done to fully understand the gender gap in retirement savings, our take (based on the MJW studies) suggests there are five main reasons why the gender gap exists:

- Investment patterns or behaviours (that lead to certain fund types)

- Fund performance (largely driven by fund type)

- Withdrawal behaviours

- Changes in employment status

- Overall economic participation

We explore these below in detail:

|

Investment Patterns by Age and GenderAs discussed above, the MJW study reveals that men are more likely to invest in growth funds, while women prefer conservative funds, with this trend being more pronounced in older age brackets. The smaller average balances held by women may make them more inclined towards conservative investment choices.

|

|

Fund PerformanceExcluding 2022 and 2023, equity markets have largely been low risk and have significantly outperformed other asset classes (like bonds or cash). In practical terms, if one had been invested in growth style funds when they started their KiwiSaver in the 2010 - 2020 period, it’s likely they would have far more investment growth in their KiwiSavers than those in balanced or conservative funds. As we’ve outlined in (1), men are more likely to invest in growth funds. If this is the case, then this may explain why men’s KiwiSaver balances are larger.

|

|

Withdrawals and SuspensionsIn examining the data on withdrawals for significant financial hardship, first-home purchases, and savings suspensions, women slightly outnumbered men in hardship withdrawals but withdrew less money overall.

More men withdrew for first-home purchases and took out a larger sum. More women had hardship suspensions, but more men had ordinary savings suspensions. Despite these differences, men actually withdrew more funds overall, which contrasts with the fact that women's balances decreased more. |

|

Changes in Employment StatusThe disparity could be influenced by differences in work patterns and labour market participation between women and men in 2022 (e.g. pregnancy and childcare considerations). Note that the MJW study did not get to this level of granularity, but it’s reasonable to expect that men might potentially be in the workplace longer than women, leading to more contributions. The data does not consider individuals who have stopped working and therefore stopped contributing to KiwiSaver if they have not formally taken a savings suspension.

|

|

Economic ParticipationThe MJW study has not undertaken any analysis on labour participation rates (e.g. full time, part time, self-employed, studying etc.) amongst KiwiSaver contributors. This may be another potential avenue for why there is a divergence in KiwiSaver balances between men and women.

|

Sources for the above information:

Must-Know Facts and Considerations about KiwiSaver and Risk

|

Some differences in risk appetite might be due to the varying sizes of KiwiSaver investment balancesResearch conducted by the New Zealand Society of Actuaries’ Retirement Income Interest Group indicated that investment choices are influenced more by the size of the investment balance than by gender.

Since men typically have larger KiwiSaver balances than women (about $31,000 vs. $25,000 as of 31 December 2022), this data doesn't necessarily imply that men have a higher risk tolerance. The generally larger account balances among males might be why they appear to opt for riskier investments on average. |

|

Generally, the more returns/gains you want, the more risk/volatility you’ll have to take on.In investing, there are no shortcuts. The more gains you want on your investment portfolio, the risk you'll likely have to take. Higher risk comes with higher volatility, meaning the value of your KiwiSaver investment balance can fluctuate significantly in the short term. Ensure you're comfortable with the sometimes erratic swings that come with a highly aggressive investment fund.

|

|

If you're younger, try to have a "risk-on" tilt, as you'll likely live longer than New Zealanders historically.New Zealanders live longer than ever before, with current life expectancy in New Zealand at just over 82 years (and young New Zealanders in the Generation Z or Millennial age brackets are likely to live even longer than that). However, it's also likely that the retirement age of 65 will get pushed out when young New Zealanders ultimately hit retirement age.

For instance, some politicians have suggested |

|

Regardless of how distant retirement might seem, it’s extremely important to plan your retirement.The current pressure on many New Zealand households due to rising living costs is not to be overlooked. However, there are a few steps anyone can take to better prepare for their future whilst ensuring stability in the present:

|

|

Keep a long-term mindset.For most Kiwis, you're investing for decades so will need to pick your fund type in light of this long runway. If you're not going to touch your KiwiSaver for multiple decades, you want to keep your KiwiSaver invested in a fund that will give you the best outcome possible (usually, that's going to be the fund with the largest overall return).

As such, aggressive funds are generally best suited for almost everyone (unless you're particularly risk-averse or you're <10 years from retiring and drawing down your KiwiSaver). Over the long term, markets generally trend upwards, and short-term volatility becomes less significant. |

|

Know what kind of person you are and whether you can handle big swings upwards or downwards.Before deciding on aggressiveness, it's essential to assess your risk tolerance. Everyone's financial situation and comfort with market fluctuations differ based on how they react.

|

|

Make sure to adjust your strategy over time.KiwiSaver isn't just a thing you decide once when you're 18 and never look at again for 40 years. As you contribute more money to KiwiSaver during your career and your initial investments compound on each other, it becomes increasingly important to reassess and adjust your strategy over time. The more you learn about investing, the better you'll get at understanding what your risk appetite and investment strategy is.

Also, rebalancing will occur within fund types to ensure they comply with the right asset weightings (e.g. 80% stocks and 20% bonds). Over time, due to market movements, the allocation of your assets can drift from your initial settings. For instance, if shares perform well, the proportion of your share investment may increase compared to bonds. Regular rebalancing, which involves realigning your portfolio back to your preferred asset allocation, ensures that your investment doesn't become more (or less) risky than you'd like. |

|

Not all "growth / conservative/balanced" funds are the same - even if they have the same name.It's essential to remember that even within a specific fund type, like a growth fund, there's variance between each provider. A growth fund doesn't just invest in one stock or industry; it spreads its investments across multiple sectors and regions. Some growth funds might have a more regional focus on the USA, while others focus on emerging markets or Australia. Make sure to do your research and deeply understand what you're investing in when you invest in a specific "fund type", including:

|

|

The Role of Fees in KiwiSaver Aggressiveness.While we often focus on returns, it's equally important to consider the fees associated with different funds. Typically, more aggressive funds, like growth funds, have higher fees than conservative funds. These fees can eat into your returns. Hence, when evaluating the potential benefits of a more aggressive fund, always consider the net return (e.g. returns after deducting all fees the KiwiSaver provider charges).

|

|

Try not to switch KiwiSaver funds too often.While it's essential to ensure your fund aligns with your goals, frequently switching between funds can lead to your KiwiSaver sitting in cash and potentially missing out on market opportunities. Switching too frequently might also incur establishment fees or switching fees (from your current KiwiSaver provider and your new KiwiSaver provider). Make informed decisions and stick with your chosen strategy unless there's a compelling reason to change.

|

MoneyHub Founder Christopher Walsh explains why only you can take action on your KiwiSaver:

|

As the founder of MoneyHub, I've spent countless hours dissecting the nuances of KiwiSaver funds and what they truly mean for New Zealanders. With the tumultuous financial landscape of 2023, I'm often asked, 'How aggressive should my KiwiSaver fund be?' It's a vital question that deserves a nuanced answer.

My philosophy is clear: there's no universal answer, but there is a universal approach - understanding. Whether you're 25 or 55, the aggressiveness of your KiwiSaver fund must reflect not just your age, but your financial goals, your risk appetite, and the realities of the market. In the wake of economic shifts and the lingering effects of global events, many Kiwis scrutinise their retirement strategies. It's a healthy exercise and one I encourage. It's easy to say 'invest aggressively when you're young and conservatively as you age,' but I believe in a more tailored approach. Your KiwiSaver should move with you, grow with you, and be a comfort, not a cause for concern. As you traverse through different life stages, your KiwiSaver fund must adapt, offering stability when you need it and growth where it counts. Let's not forget the power of compounding returns - what may seem like a modest balance today can be the cornerstone of your financial freedom tomorrow. That's why it's critical to nail down the right fund early on and to reassess it periodically. Your future self will thank you for having the foresight. I'm often reminded that the beauty of KiwiSaver is its flexibility. Unhappy with your fund's performance? Let's change that. Concerned about risk as you near retirement? There are options for that. The key is never to stand still - to make your KiwiSaver fund an integral part of your financial journey, alongside your investments and everyday finances. At MoneyHub, we're dedicated to empowering you to make the best choices for your retirement with clarity and confidence, but you need to make the first move and take action". |

Christopher Walsh

MoneyHub Founder |

Frequently Asked Questions Related to KiwiSaver Aggressiveness

Based on all the research and studies above, how aggressive should my KiwiSaver fund be?

While there's no right answer here, generally if you're young, you want to be as aggressive as possible (e.g. you want to have as much of your KiwiSaver in shares that have equity ownership in companies rather than things like bonds and cash, which have a far lower return threshold). What most people forget is that investing in "growth funds" can still mean your portfolio has upwards of 20% allocated to things that AREN'T shares, like bonds and cash.

Age plays a crucial role in determining the aggressiveness of your KiwiSaver fund. For a quick rule of thumb:

Age plays a crucial role in determining the aggressiveness of your KiwiSaver fund. For a quick rule of thumb:

- Under 30 years old: At this age, you have a longer investment horizon, allowing you to ride out the market's volatility. A growth fund, with its higher risk and potential for significant returns, is usually ideal. You’ve got 40+ years of runway left for your investment to compound, so you’ll want to be as aggressive as possible (If you’re very young – for example, around 20 years old, try to pick the funds with the highest % of stocks, as you’ll have the longest runway of all).

- 30 - 40 years old: Generally, a growth fund at this age is still suitable for many. However, some more risk-averse New Zealanders may start to lean towards a balanced fund. You still have 30 years left until you likely retire, so growth is still the go.

- 40 - 50 years old: As retirement nears, a growth or moderate fund is usually appealing. You’ll still have around 20 years left to retire, so you’ll want to be looking to take full advantage of compounding and invest somewhat aggressively.

- 50 - 60 years old: At this stage, safeguarding your savings becomes more vital. A moderate fund approach, leaning more towards income assets, can be more appropriate.

- Sixty and above: As retirement is imminent or a reality, most individuals shift to conservative funds. Stability is paramount, and capital preservation is the main goal (especially if you want to cash it out). However, in some circumstances, you may leave your KiwiSaver invested (as you have other non-KiwiSaver investments or savings to draw down in retirement). In this case, noting you'll still likely live for another 20 years based on the average life expectancy of New Zealanders in the low 80s, it can make sense to still be aggressive in your KiwiSaver allocation.

My KiwiSaver never seems to move and it’s such a low balance. Does fund type even matter?

- While your KiwiSaver may seem small and insignificant right now relative to your income and net worth, don’t underestimate the power of compounding returns.

- Because you’ve likely got a long runway of time for your KiwiSaver to grow (and you’ll hopefully be continuously putting in funds alongside the NZ Government), it can balloon into a significant sum over time.

- However, this will only happen if you invest in the RIGHT fund. if you invest in the WRONG fund, you won’t get the maximum benefits of this. For example, if you started out in a moderate or conservative fund with the majority of your investments in cash, those cash assets won’t grow at the same rate as equities (especially across multiple decades).

- That’s why it’s important to nail the right fund for you and your situation right now, and assess every so often.

How do global events impact the aggressiveness of my fund?

Global events, like economic downturns or geopolitical tensions, can affect market performance. Aggressive funds, with a higher share allocation, can be more sensitive to such events. However, a diversified portfolio can help cushion against some of these impacts.

What if I have a low-risk tolerance but a long time before I retire?

It's essential to invest in a manner that lets you sleep peacefully at night. If a growth fund makes you anxious, consider a balanced or moderate fund. You might sacrifice some potential returns, but you'll have a level of risk you're comfortable with.

Can I have multiple KiwiSaver accounts with different risk profiles?

You can't have multiple KiwiSaver accounts. However, some providers offer 'life stages' or 'age-based' options that automatically adjust your risk profile as you age.

Can I change my KiwiSaver fund if I'm unhappy with its performance?

Yes, you can switch between funds. It's crucial to regularly review your fund choice to ensure it aligns with your investment goals and risk tolerance.

Is it safe to be in a growth fund close to retirement?

While growth funds offer higher returns, they come with increased volatility. If you're nearing retirement, a significant market downturn could impact your savings. However, if you're planning on keeping your KiwiSaver invested after you hit retirement age and think you'll likely live for a long time (e.g. you've got 20+ years of life left), it's okay to still be in a growth fund closer to retirement.

Do all aggressive funds have the same level of risk?

No, the risk levels can vary even among aggressive funds based on their asset allocation and investment strategies.

Related Resources:

- KiwiSaver Providers

- Our Favourite KiwiSaver Funds

- KiwiSaver Guide

- Choosing your KiwiSaver Scheme Provider

- How to Choose a KiwiSaver Fund

- KiwiSaver Essentials

- Withdrawing Your KiwiSaver

- Switching KiwiSaver Funds

- KiwiSaver Hardship Applications and Balance Withdrawals

- Moderate vs Balanced vs Growth Funds - What KiwiSaver is right for me?