Lifetime Retirement Income

Updated 24 July 2023

Important: MoneyHub has been notified the Lifetime Retirement Income scheme has been relaunched. The review below relates to the legacy offering. For the latest news, visit the Lifetime website.

Our guide to Retirement Income Products covers the new version of Lifetime.

Our guide to Retirement Income Products covers the new version of Lifetime.

Summary of Lifetime Retirement Income

- Lifetime Asset Management Limited (known as Lifetime) offers the opportunity to invest into a fund that, with the use of an insurance policy, guarantees fixed cash payment every year until you die.

- Such retirement schemes are known as a variable ‘annuity’, and on paper, it sounds attractive to anyone first hearing about it. But there are many things you’ll need to understand about variable annuities before investing.

- Variable annuities are not without their risks and may not be a suitable product for your retirement needs. In many cases, you can pay tens of thousands of dollars in fees during your retirement.

In this guide we breakdown what Lifetime is offering, how it works, what it costs, the advantages, disadvantages, alternatives and essential facts to make you aware before you go any further. We cover:

- What exactly is the Lifetime Retirement Income fund and how does it work?

- Where is my money invested, and is it safe?

- Management, Insurance and Joining Fees

- Lifetime Income Payments vs Bank Deposits

- Inflation, and why it matters for Lifetime

- Advantages and Disadvantages

- 10 Must-Know facts about Lifetime

- Lifetime FAQs

Know this first:

Be Aware: New Zealand Retirement Schemes have a chequered history - guaranteed annual payments attract attention

Warning: Do NOT invest in Lifetime (or any other annuity) if you do not fully understand how it works, the costs and the risks. It's essential that you know what you are getting into before you give over any amount of money as there are long-term implications of this investment.

- The concept of annuities and guaranteed income are both relatively new to New Zealand, and don’t worry if you find them complicated – they are!

- As more providers either introduce, or look to offer such products, we anticipate more media attention on them and higher awareness of how they work in the public domain.

- If you want the certainty of a fixed income every year for the rest of your life, an annuity can provide this. However, there are costs involved, including insurance and management fees, insurance premiums and the possibility of negative returns on your assets. In saying this, the product offers a fixed guaranteed income for life, irrespective of the investment performance.

- Be aware, the insurance and management fees are deducted from your initial investment, meaning you and/or your estate are probably going to be left with much less than you invested, or in some cases, nothing, depending on what age you die. Lifetime is about income in retirement that’s insured for life, not accumulating wealth for the future.

- It is often easier, and significantly cheaper, to manage your money yourself depending on your financial background. We include a comprehensive comparison with putting money in Lifetime vs in a bank.

Be Aware: New Zealand Retirement Schemes have a chequered history - guaranteed annual payments attract attention

- The retirement industry in New Zealand has suffered its fair share of problems, from failed finance companies, property development funds, bankrupt NZX-listed companies, Ponzi schemes and dodgy ‘too good to be true’ investment scams.

- Because the only thing that is certain in the future is death, the offer of having a guaranteed income stream for the rest of your life can appear to be very attractive.

- However, there are many things to know before making any decision to take out a variable annuity.

Warning: Do NOT invest in Lifetime (or any other annuity) if you do not fully understand how it works, the costs and the risks. It's essential that you know what you are getting into before you give over any amount of money as there are long-term implications of this investment.

What exactly is Lifetime Retirement Income and how does it work?

- By definition, a variable annuity is a "fixed sum of money paid to an individual or couple fortnightly or monthly typically for the rest of their life". In its simplest form, it is an insurance policy.

- You pay a sum of money to an insurance company who in return guarantees you will always be paid a fixed amount of money until you die.

- The sum of money you pay to the insurance company will be invested on your behalf in a fund.

- The guaranteed payment you receive will be made up from your original capital investment and the returns the fund makes.

- If the fund doesn't earn enough money to cover the payments and fees over time, and all of your money has been paid out to you, the variable annuity guarantees you will continue to be paid. This is how the insurance policy components works. You are protected no matter what happens to your money and for the rest of your life.

How does this relate to Lifetime?

- The Lifetime product is a variable annuity, and allows you to buy an insurance policy. You pay Lifetime a sum of money, it invests it on your behalf, and you receive the same amount of money every month or fortnight until you or your spouse dies (if you choose the spouse benefit).

- There is provision to withdraw lump sums from your fund. On your death, your estate receives any balance in the fund.

Important - Lifetime's product is 'variable' and different from the historical concept of an annuity. In a good way.

- Every investor has access to their capital, (less income payments and net investment returns) at any time. This is an improvement from older products which were 'purchased' meaning the capital was lost. In summary, if you want your money later on, you can withdraw it.

- Older annuities generally offered returns that were linked to similar duration fixed-interest investments which meant low returns. The Lifetime product invests in a balanced fund with an expected gross return over 20 years of 6.5% p.a.

- Older life annuities were held as a balance sheet asset of the Insurer and the fund returns were taxed at the same rate as the insurer. But Lifetimes' funds are a PIE and not held on its balance sheet; tax is deducted at the individual’s tax rate, rather than Lifetime's.

Know this:

- The guaranteed income you receive every year is not a return on your investment - your money decreases year after year as fees are charged, the fund makes its returns and your guaranteed income is paid out.

- If you are told by anyone selling variable annuities that your guaranteed income is a return on your investment, this is not true (and also fraudulently misrepresents the product).

How does Lifetime's policy work in practice?

The ins and outs of the policy are best explained using an example:

- Max and Claire are both 64 and want to retire at 65.

- They have $100,000 set aside and want to buy Lifetime's policy to give them a guaranteed income for life. The $100,000 becomes what is known as their 'Protected Income Base'.

- Lifetime's 'Withdrawal Benefit Payment Rate' for anyone retiring at 65 years of age is 5.00%.

- What this means is that the policyholder(s) will receive 5.00% per year, every year, on the money they set aside for the variable annuity.

- For Max and Claire, this means they are guaranteed to receive $5,000 (5.00% of $100,000) each year for the rest of their lives.

- To kick things off, they transfer $100,000 to Lifetime and their money is invested in a fund which aims to make a return above 6.50% per year.

- As the future performance of global markets can never be predicted, the fund's return may be less than 6.50% per year Lifetime states it expects. If there is any shortfall in returns, Max and Claire still receive their $5,000, but the shortfall will come from the original $100,000 they paid to Lifetime originally.

- If Max and Claire live long enough, the funds they set aside may have all been eaten up in guaranteed income payments and Lifetime's ongoing fees. If this is the case, the policy guarantees them that they will continue to receive their $5,000 every year even if there is nothing left. This is the risk that Lifetime takes.

- Conversely, Max and/or Claire may pass away - at this point, whatever is left from their original payment to Lifetime will become the property of the estate.

- Max and Claire have the option, for an extra fee, to have the income continued to be paid to the surviving partner on death of either Max or Claire.

Table 1 - Lifetime's benefit payment rate (guaranteed for life from the age you agree first to receive your payments)

- Lifetime lets you start receiving your Lifetime Withdrawal Benefit at any time if you are between the ages of 60 and 90.

- The age you choose to start receiving your Lifetime Withdrawal Benefit determines your Payment Rate, and the amount you'll receive fortnightly or monthly. For example, if you decide to start at 70, you will receive 5.50% of your protected income base every year, paid fortnightly or monthly.

- Once you've chosen to start your Lifetime Withdrawal Benefit your Payment Rate won't change. In the example above, the 5.50% will be paid every year until the policy holder dies.

Age at first Lifetime Withdrawal Benefit Payment |

Lifetime Withdrawal Benefit Payment Rate (percentage of Protected Income Base) |

60 |

4.50% p.a. |

61 |

4.60% p.a. |

62 |

4.70% p.a. |

63 |

4.80% p.a. |

64 |

4.90% p.a. |

65 |

5.00% p.a. |

66 |

5.10% p.a. |

67 |

5.20% p.a. |

68 |

5.30% p.a. |

69 |

5.40% p.a. |

70 |

5.50% p.a. |

71 |

5.60% p.a. |

72 |

5.70% p.a. |

73 |

5.80% p.a. |

74 |

5.90% p.a. |

75 |

6.00% p.a. |

76 |

6.10% p.a. |

77 |

6.20% p.a. |

78 |

6.30% p.a. |

79 |

6.40% p.a. |

80 |

6.50% p.a. |

81 |

6.60% p.a. |

82 |

6.70% p.a. |

83 |

6.80% p.a. |

84 |

6.90% p.a. |

85 |

7.00% p.a. |

86 |

7.10% p.a. |

87 |

7.20% p.a. |

88 |

7.30% p.a. |

89 |

7.40% p.a. |

90 |

7.50% p.a. |

Understand where your money invested, and assess whether it is safe

- Lifetime invests your money in a ‘balanced fund’. This means it invests in global assets, such as bank deposits and bonds, as well as global growth-focused shares. The purpose of a balanced fund is that it is not high in risk, but also should make a better return over time than money in a term deposit given it allocates some of your money to invest in the sharemarket.

- Lifetime invests money in ANZ term deposits, SmartShares, and with fund managers Vanguard and Harbour Asset Management.

- Because Lifetime’s fund value goes up and down every day, there is a risk that if you want to withdraw money, your balance could have fallen if global markets have dropped. But, this won’t affect your guaranteed income payments which are fixed for the rest of your life.

- You invest $100,000 and you are guaranteed to be paid 5% per year net of fees and tax from age 65 onward.

- Every year, you receive $5,000, as per your agreement.

- Some years on, there is a global crash and your investment balance falls to $70,000.

- You will continue to receive the $5,000 per year.

- While your income guarantee is protected, your investment balance can fluctuate. This means if you wanted to withdraw 20% of your fund, you would only receive $14,000 (20% of $70,000) and not the $20,000 as per your original investment.

- Also if, for example, you withdraw $10,000 from a $100,000 protected income base, your ongoing benefit will reduce by the same proportion. So if you received $5,000 per year, after the withdrawal you would receive $4,500.

- Lifetime aims to make sure the underlying funds are invested in relatively ‘safe’ assets that are not volatile to market shocks.

Important - the most important thing is that your annual income is GUARANTEED

No matter what happens to your investment, even if it goes to $0, your annual income is protected. You cannot outlive the benefits – even if you receive more each year than your fund is worth, you will continue to receive the money year after year until you die. We analyse the payments below.

No matter what happens to your investment, even if it goes to $0, your annual income is protected. You cannot outlive the benefits – even if you receive more each year than your fund is worth, you will continue to receive the money year after year until you die. We analyse the payments below.

Lifetime charges fees - and they do add up

Understanding Lifetime's ongoing fees is essential in your decision marking, and we put the different fees in context below with common examples:

Joining and Withdrawing fund fees:

- Insurance fees: You will pay 1.35% per year of your original payment to Lifetime for insuring you to you receive your guaranteed income. If your initial payment was $100,000, you would pay $27,000 in insurance fees in the first twenty years.

- Management fees: You will also be charged a fee for having your fund managed, and you pay 1% every year on the remaining balance of your fund. Over 20 years, that adds up to $15,000 (based on the assumption your fund grows 6.50% per year, before deductions for tax, the 5% payments to you and the insurance fees). Add this to your insurance fees, and it’s $42,000 over 20 years, or $2,000 a year in fees you will pay on the original $100,000 investment.

- Be aware, the insurance and management fees are deducted from your initial investment, meaning you and/or your estate are probably going to be left with much less than you invested, or in some cases, nothing if you live beyond 90 years of age.

Joining and Withdrawing fund fees:

- Joining fee - You have to pay to join the fund (0.125% of the value). So if you invest $100,000, $125 is deducted, so your available money is $99,875.

- Withdrawal fee - You can withdraw multiple lump sums, and you’ll pay a fee on the amount you take out (0.125% of the value). For example, if you take out $10,000, you’ll be charged a $12.50 fee.

Lifetime Income Payments vs Bank Deposits

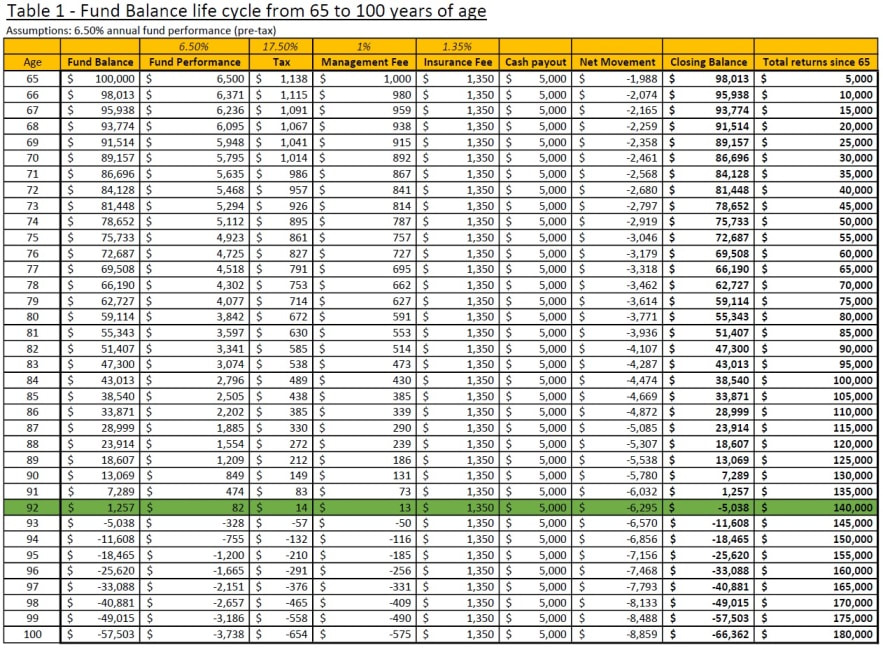

To understand how Lifetime works, we've presented a simple table below that charts the cash movements from age 65 to age 100. You can download both the tables as a PDF (Table 1 and Table 2).

In Table 1, we have used an example of an original Fund Balance of $100,000.

Conclusion

Based on our calculation, we believe that Lifetime only has some value if the policyholder lives significantly beyond 92 years of age. We have compared the alternative option of investing the original $100,000 in the bank (see Table 2 below).

In Table 1, we have used an example of an original Fund Balance of $100,000.

- Every year, we assume the Fund Performance will be 6.50% (which is consistent with what Lifetime says they expect).

- The return is added to the fund balance, then Tax is deducted. We have used a Prescribed Investor Rate of 17.50% but your tax rate may be higher if you earn more.

- The Management Fee (1% on your closing fund balance) and Insurance Fee (1.35% on your original payment to Lifetime) are also deducted.

- Finally, a Cash payout is made (i.e. the guaranteed income you receive fortnightly or monthly).

- The Net Movement is how much your fund has increased or decreased in the year. Unless the average Fund Performance is above 9.00%, it is likely the Fund Balance will decrease year after year.

- In this example, we see that at age 92, the Fund Balance is $1,257 and the total returns have been $140,000. If the policyholder lives beyond 92, the Fund Balance becomes negative, but due to the insurance policy, they will continue to receive their $5,000 guaranteed income every year until they pass away.

- As a point of interest, the total Management and Insurance fees paid by age 92 total close to $55,000.

Conclusion

Based on our calculation, we believe that Lifetime only has some value if the policyholder lives significantly beyond 92 years of age. We have compared the alternative option of investing the original $100,000 in the bank (see Table 2 below).

Note: We understand that payments to policyholders are made more frequently than once a year, and that fund performances fluctuate year over year - this example is a simple walk-through of a typical variable annuity.

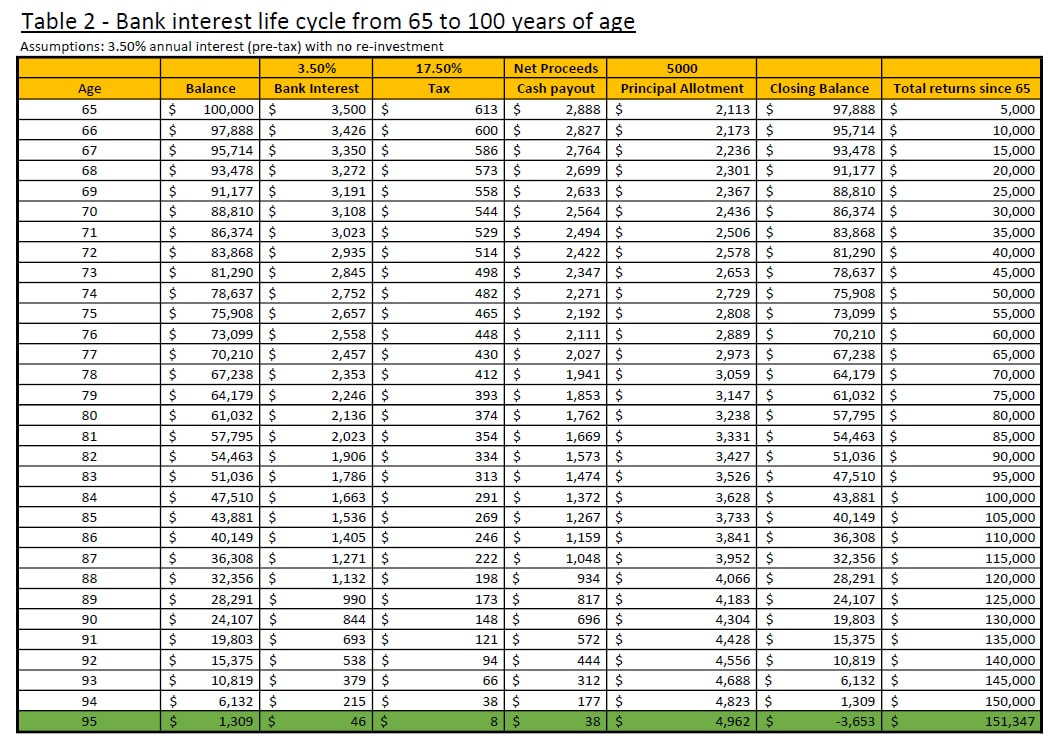

In Table 2, we have also used an example of an original Fund Balance of $100,000.

- Every year, we assume the Bank Interest rates will be 3.50% (which is consistent with 2018/19 term investment interest rates).

- The return is subject to Tax which is deducted - we have used a Prescribed Investor Rate of 17.50% but your tax rate may be higher if you earn more.

- The Net Proceeds is the Bank Interest less Tax. In this case the amount is $2,888 per year, this is paid in cash to the investor.

- The term deposit's assumed interest rate (3.50%) is not enough to earn $5,000 per year, so we have calculated that the remaining portion of the $5,000 will be funded by your original investment. As time goes on, the interest you earn (in dollar terms) drops as more and more of your original investment is paid out every year as part of the $5,000 you receive (Lifetime works the same way).

- By the age of 95, your investment is worth $1,309, and you have received $150,000 of payments over 30 years.

- Lifetime, by comparison in Table 1, shows your fund running out at 92 years of age based on a 6.50% annual return. After 92, you will receive $5,000 for the rest of your life as per the insurance policy. With a bank deposit, you will receive $0 after 95 years of age.

Assumptions we have made, and limitations in the comparison between a variable annuity and a term deposit

Conclusion

- We have assumed there are no break fees if you want to withdraw your term deposit early and access your capital - in practice there are usually interest rate adjustments if you take your money out early.

- Term deposits, unlike the Lifetime product, do not offer longevity (i.e. a fixed interest rate/return beyond five years) nor do they offer any market protection for the retiree.

- We assume a long-term interest rate of 3.50%.

- Unlike Lifetime's product which guarantees income for life, if the retiree uses up their investment before they die, there will be no further payouts.

- Term deposits do not make fortnightly or monthly cash payments, where as Lifetime does. Retirees need to re-invest their term deposit when it matures, withdrawing the interest for their day to day needs.

Conclusion

- Even though a variable annuity and a term deposit are not the same products, we wanted to see the costs involved in generating a $5,000 return per year.

- We conclude that unless you live beyond 95 years of age after retiring at 65, a bank deposit does provide better value for money than Lifetime's offering in dollar terms. However, Lifetime offers certainty of income for the rest of your life - a term deposit does not.

Inflation is Lifetime's Biggest Enemy

The rate of inflation is really important - if New Zealand sees a return to the 5%+ levels of annual inflation of the 1980s and 1990s, the benefits of the offering are significantly reduced. Specifically:

- The standard Lifetime product is NOT inflation adjusted. This means what you get paid in today’s money will be worth a lot less in the future. To protect against this, Lifetime offer indexed options at lower guaranteed rates to help manage the impact inflation has on the value of income payments.

- For example, if you retired at 60 in 1970 with a $25,000 investment (which back then was enough to buy a house in Auckland) and a 5% guaranteed income every year, you would receive $1,250 per year.

- The problem is that inflation can seriously affect the value of this income. While $1,250 per year in 1970 was a lot, it was a lot less valuable by 1990, and it is not that much in 2019-20.

- There is a serious risk that if inflation was to take off again in New Zealand, your 4.50% to 7.50% guaranteed income wouldn’t keep up with the increasing cost of everyday items. As a point of reference, inflation is currently running at around 2%.

Advantages of Lifetime:

Disadvantages of Lifetime:

- Guaranteed income for life and a Protected income base - once you start receiving your guaranteed income for life, no matter what happens to the fund you are invested in, you will always receive your ongoing payments, even if your payments and fund performance reduce your fund to $0.

- Withdrawals are possible - you can withdraw any or all of your investment at any time, and there is no limit on how many withdrawals you can make. You will pay a 0.125% fee on any sum you take out - so if you withdraw $10,000, you'll pay a $12.50 fee and receive $9,987.50. The percentage you withdrawal also affects your ongoing guaranteed monthly income. For example, if you withdraw $10,000 from a $100,000 protected income base, your ongoing benefit will reduce by the same proportion. So if you received $5,000 per year, after the withdrawal you would receive $4,500.

- Joint investment benefits - Lifetime can accept couples where the age differential of each partner is ten years or less; for example, a 64 and 57 is covered, but if you are 64 and your partner is 53, you won't be eligible. The benefit is that if one person passes away, the surviving person will continue to receive the Lifetime withdrawal benefit for the rest of their life. There is a higher insurance fee for this - single policyholders pay 1.35% where as couples will pay 1.75% on their protected income base.

- Lifetime's guaranteed income for life payments are regulated and monitored by the Reserve Bank of New Zealand - Lifetime, just like a bank, is required by law to hold sufficient regulatory capital to meet their obligations at all times.

Disadvantages of Lifetime:

- Unless you take out a specific inflation-proof policy, you are not inflation protected – meaning whatever you agree to be paid could, if past inflation is anything to go by, be worth 25-40% LESS by the time you’re 80. Right now, in 2019, we have low inflation. But if it goes higher, as some economists have said it will, the payment you receive may be worth a lot less in real terms, and would not even keep up with rising costs. Such an instance would create a miserable situation as we explain below. Lifetime do offer inflation proofed rates, but this is optional and means a lower guaranteed payment.

- High ongoing fees which eat up your investment year after year - fees can add up, and we discuss fees in detail below.

- Lifetime is an insurer, holds a Managed Investment Scheme (MIS) licence under the FMCA, and has a B- credit rating - Public Trust is the fund supervisor and holds the insurance policy for the benefit of the investors under the FMCA regulations, the solvency capital used to support the guarantees offered to investors is regulated and monitored by the Reserve Bank of New Zealand.

- Entry and Exit fees - when you invest, 0.125% of your money will be charged to join the Lifetime fund. If you decide to withdraw or leave the fund altogether, another 0.125% is charged for each withdrawal.

10 Must-Know Facts About Lifetime Retirement Income’s Fund

|

Lifetime is a variable annuity, which means it’s a contract between you and an insurance company to provide income for lifeYou may think a variable annuity is an investment, but it is not. It is a contract, where the risk involved in committing to pay you every year is held by the insurer. Lifetime’s product locks you and the insurance company into contractual obligations. You pay 1.35% of your initial investment value every year as a fee to the insurance company. In return, the insurance company gives you a fixed net return between 4.50% to 7.50% depending on when you retire.

Products like Lifetime have been around since Ancient Rome, where Romans would pay a company a lump sum in return for guaranteed annual payments for life. Today, in New Zealand, retirees have the same money worries about their retirement as the Romans. Investments in your KiwiSaver fund, the sharemarket or even a term deposit with a bank don’t provide regular income. For example, shares in Air New Zealand don’t pay you a guaranteed amount for owning them as dividends are only paid twice a year and vary depending on the profitability of the company. As such, Lifetime (and products like it) are becoming more popular as retirees look towards annuities as an option to replace income streams, i.e. wages from their employer. Lifetime’s product offers what no other investment can do – it provides guaranteed income for the rest of your life no matter how long you live. It works similarly to the superannuation payments you receive from the government after you turn 65 with the main difference being that government superannuation is adjusted regularly for inflation. Know this: You will be charged fees, but this will only affect the value of your account balance and not your guaranteed income - our income example demonstrates this. |

|

The younger are when you start receiving your guaranteed income, the lower the percentage payout you will receiveLifetime pays you 4.50% of your investment if you retire at 60, and up to 7.50% if you retire at 90. The younger you are when you receive payments, the longer your life expectancy is and the smaller your payments will be. It’s all based on what the insurer can afford so neither you or the insurer have an advantage.

|

|

You are paid fortnightly, for the rest of your lifeEvery two weeks, Lifetime will make a payment into your bank account. You don’t have the option of weekly or monthly payments, or a lump sum payment either. You’ll need to manage how you spend the payments as they can’t be advanced or deferred once you start receiving your payments.

|

|

Lifetime offers a ‘Protected Income Base’ advantageYou can defer your payment data and take advantage of market movements. Lifetime lets you sign up, invest and defer when the payments begin. This lets you contribute as much as you can to maximize the protected income base and by receiving the guaranteed income later you will receive a higher percentage rate. You only pay insurance fees which you start receiving your guaranteed income.

|

|

The minimum investment is $25,000There is a minimum investment of $25,000, and a maximum of $1 million, and Lifetime recommends investing a maximum of 40% of your savings into their product.

|

|

Your payments are net of tax, so you won’t have any problems from the IRDLifetime pays the IRD tax on your behalf, so the guaranteed income you receive every month is net of tax. You are taxed at your prescribed investor rate (PIR).

|

|

There are no fees if you want to withdraw money, but there is a limit on how much you can take outYou can take out whatever amount you want at any time, and a 0.125% fee applies on every withdrawal.

|

|

Lifetime’s product, and annuities in general, are not growth productsIf you want to invest in something which gives you market growth, Lifetime is probably not the right choice given the fees and balanced fund focus.

|

|

Lifetime makes the most money when clients die just before their account balance runs outThe most lucrative client for Lifetime is one that dies just before the fund balance approaches zero. This because Lifetime will charge the management fee and insurance fee every year until then. If a client dies early, then they have to pay out the fund and Lifetime will not receive any future income in the years to come.

|

|

Lifetime's guaranteed income for life payments are government protected - bank deposits are notLifetime, just like a bank, is required by law to hold sufficient regulatory capital to meet their obligations at all times. New Zealand law protects Lifetime policyholders meaning their guaranteed income will be paid for life even if something happens to Lifetime. Bank term deposits, in comparison, are not guaranteed - although in the history of New Zealand there has never been such financial issues.

|

Lifetime FAQs

Is Lifetime right for you?

MoneyHub is not a financial adviser, and the answer is 'it depends on your circumstances'. If you have a significant level of assets and income streams, and don’t expect to need to depend on your government superannuation payments in retirement, you are less likely to need a guaranteed income product. If you don’t have a lot of savings and would appreciate knowing you will always receive the same amount of money for the rest of your life, Lifetime could be more attractive to you.

Does the money I receive from Lifetime Retirement Income affect my New Zealand superannuation payments?

No – you receive your Lifetime payments in addition to your superannuation fund, which is inflation-adjusted every year by the government. Lifetime simply offers a ‘top up’ to your existing superannuation payments.

Who is the insurer who provides the ‘guaranteed’ income, and what happens if they go bankrupt?

Lifetime Income Limited is the insurance company, and it is licensed by the Reserve Bank of New Zealand. It has a B- credit rating, which is one level above C+ ("marginal") per its rating agency A.M. If the parent company - the Retirement Income Group goes bankrupt you will have three options:

- The funds trustee, the Public Trust, may place the guarantee with another Insurer or

- You will have your account balance paid back (meaning you can get back whatever is left of your original investment less income received plus net investment returns), and your Lifetime income guarantee value paid out of reserves held in a separate statutory account supervised by the Reserve Bank of New Zealand or

- You will continue to receive your guaranteed income for life (funded by the reserves specifically held for this purpose)

How much can I invest in the Lifetime Retirement Income fund?

Currently, you can invest up to one million New Zealand dollars.

What happens when I die?

Firstly, your guaranteed income stops. Secondly, any balance remaining from your original contribution will be made available to your estate, less a 0.125% withdrawal fee.

Can I withdraw money from the fund?

Yes, up to 20% at a time. A charge of 0.125% applies, meaning if you take out $10,000 you will receive $9,987.50 as Lifetime takes a $12.50 fee. You can withdraw more, but this means you will exit the entire scheme.

What are the tax implications for the fund?

Because you contribute a sum of money upfront, receiving it back as a part of your 'guaranteed income' is tax-free (because Lifetime is paying you your own money). Per Lifetime's terms and conditions, tax is only paid on your investment returns from the balanced fund. This is paid on your behalf by Lifetime before you receive it.

Is the Lifetime Retirement Income better than putting my money in a bank?

As our data indicated above, unless you retire at 65 and live beyond 95 years of age, Lifetime will work out to be more expensive. This is due to the ongoing fees charged, the entry and exit fees. There is also the added risk of inflation eating away guaranteed income, where as term deposit interest rates tend to move in line with inflation rates.

Who is Lifetime not suitable for?

1. If you have proven success in managing your own money.

Lifetime's policy basically serves to manage your retirement funds in exchange for providing you with a fortnightly income. You are charged a fee of 2.35% per year of your savings to do this. If you have a proven track record of looking after your money, Lifetime's policy is unlikely to be of value to your retirement.

2. If you have enough money to meet your needs during your retirement, even if you live to 110 years old.

If you have a lot of assets and believe these will last all of your retirement years, and can sell-down your assets without causing any financial stress, Lifetime's policy is unnecessary.

Lifetime's policy basically serves to manage your retirement funds in exchange for providing you with a fortnightly income. You are charged a fee of 2.35% per year of your savings to do this. If you have a proven track record of looking after your money, Lifetime's policy is unlikely to be of value to your retirement.

2. If you have enough money to meet your needs during your retirement, even if you live to 110 years old.

If you have a lot of assets and believe these will last all of your retirement years, and can sell-down your assets without causing any financial stress, Lifetime's policy is unnecessary.

Our View: Lifetime, and Annuities in general

- In general, we are not fans of annuities, but we understand and support the protection they offer to retirees looking for certainty for the rest of their life. No other retirement product in New Zealand is able to provide what Lifetime offers.

- The fees are high, the guaranteed returns can be eroded by inflation and you don't have control of your money.

- Most importantly, annuities are insurance policies. What you contribute on day 1 is not what you can get out, or what your estate receives when you pass away.

- In the case of Lifetime, you are paying 2.35% per year on the original amount you contributed, but will only receive between 4.50% and 7.50% and any shortfall in your guaranteed income is taken from your original contribution.

- The fees charged up - a $100,000 fund will incur over $40,000 in fees over 20 years.

- Lifetime has a B- credit rating; but if the parent company - the Retirement Income Group goes bankrupt you will have three options:

- The funds trustee, the Public Trust, may place the guarantee with another Insurer or

- You will have your account balance paid back (meaning you can get back whatever is left of your original investment less income received plus net investment returns), and your Lifetime income guarantee value paid out of reserves held in a separate statutory account supervised by the Reserve Bank of New Zealand or

- You will continue to receive your guaranteed income for life (funded by the reserves specifically held for this purpose)