Should I Stop Contributing to KiwiSaver?

Looking to stop contributing to KiwiSaver due to financial pressures? Our guide covers the pros and cons of this decision, the consequences in the long term and how to take a savings break to help you make an informed decision about your financial future.

Source: Bloomberg and The Inland Revenue (IRD).

Updated 16 March 2023

Summary:

Know This First: An Example

Our guide covers:

Summary:

- Almost all New Zealanders will know of KiwiSaver and the benefits of saving money for the future. However, with a cost of living crisis, many are considering stopping their contributions to KiwiSaver due to financial pressures.

- While it's widely known that stopping your KiwiSaver contributions has long-term ramifications for your financial future, the specifics are rarely articulated and the consequences are rarely appreciated.

- While the high living costs make it completely understandable to consider all the options to make ends meet, including pushing away retirement savings, stopping contributions to KiwiSaver can have serious consequences for an individual's financial security in the long term. These can lead to unintended consequences such as difficulties in old age and missed investment opportunities.

- If you stop contributing to KiwiSaver, the 3% (or whatever percentage you contribute) you previously contributed will be added to your regular salary or wages. However, it is important to note that this additional amount will be subject to income tax, just as it would have been if it remained part of your KiwiSaver contribution.

- KiwiSaver contributions and income tax are calculated based on your gross pay, so your tax rate remains the same regardless of whether the funds are sent to your KiwiSaver fund or received as part of your regular income. You also lose out on the employer's 3% gross contribution, as well as the government tax credits.

Know This First: An Example

- If you earn $60,000 a year and stop your 3% KiwiSaver contributions, you would have an additional $1,800 (3% of $60,000) added back to your annual income.

- A $60,000 salary puts you in the 30% income tax bracket for income between $48,001 and $70,000. Therefore, the additional $1,800 you receive will be taxed at 30%.

- Stopping your KiwiSaver contributions would give you an additional $1,260 in your annual income after tax.

Our guide covers:

Know The Difference - Opting out vs Stopping your Contributions

- Opting out is available for a specific timeframe (day 14 to day 56) when a new employee who is not already in KiwiSaver has been auto-enrolled by an employer, as per their obligation.

- Opting out closes an account (which has only ever been provisional), meaning no funds have been passed to the provider.

- The employee is refunded their deductions, the employer is refunded theirs, and the account is never active.

- Many people think they can ‘opt out’ of any employer at a later date to stop deductions. However, this is not the case - you can only choose a savings suspension. Opt-outs sent to Inland Revenue are declined, and a savings suspension is automatically issued for 12 months.

- Many New Zealanders do not understand the difference, but we publish this section to make it clear. This guide focuses on savings suspensions which allows you to stop contributing and retain more of your after-tax income.

Know This First: Understanding KiwiSaver and How to Stop Contributing

- As a background, KiwiSaver is a voluntary retirement savings scheme designed to help Kiwis save for retirement. It's an important financial tool that can provide financial security in old age and help prevent future financial difficulties. The scheme is designed to help Kiwis save for their retirement by making it easy to set aside a portion of their income each pay period.

- When you enrol in a KiwiSaver scheme, you'll choose a savings plan that suits your needs and risk tolerance. Your employer will then automatically deduct a set amount from your pay each pay period, which will be deposited into your KiwiSaver account.

- For those that enrol in the KiwiSaver scheme, the minimum amount set by legislation is 3% of your pay (which is matched by your employer). However, some government and private companies can offer more to incentivise increased retirement savings and improve employee compensation packages.

- In addition to your contributions, the government also makes contributions to your account through member tax credits. These credits are paid annually based on the amount you've contributed to your account during the previous year. More information on the government's member contributions can be found on the IRD's website.

- You can choose to stop contributing any time you want; it's called a savings suspension and you'll lose your employer's contribution (e.g. 3%). All employees who have contributed and been a member for 12 months or more can have a savings suspension for 3 months to 1 year. You do not need to give a reason and you can have as many savings suspensions as you want. You'll need to access MyIR and follow the steps outlined here.

- Generally, you'll only be able to withdraw your KiwiSaver after you turn 65. However, some situations allow you to withdraw your KiwiSaver, such as when you're purchasing your first home, when you're going through financial hardship or when you're leaving New Zealand permanently. You cannot opt-out once you're enrolled unless you leave New Zealand (or were enrolled without your knowledge and exit before a set time), but you can have as many savings suspensions as you want.

More Details on KiwiSaver:

Why are Kiwis Stopping their KiwiSaver Contributions?

There are two primary reasons why Kiwis are considering stopping contributions to KiwiSaver:

1. Financial Pressure

New Zealand is experiencing a strain on household budgets due to high inflation and rising prices for necessities like rent, groceries, and child care. The high cost of living can make it difficult for individuals to afford to contribute to KiwiSaver, especially if they're struggling to meet their current expenses. While a 3% contribution doesn't seem significant, many households are struggling and financial pressure may mean current expenses are prioritised over saving for the future. Having $20 or $30 extra per week on an average by dropping KiwiSaver wage is significant.

2. Decreased Net Worth and Portfolio Values

Another reason why Kiwis are considering halting contributions to KiwiSaver is the market downturn and negative financial performance of funds. If individuals see their KiwiSaver accounts decreasing in value due to market fluctuations, they may be discouraged from continuing their contributions. This behaviour can be especially true for inexperienced or uncertain investors in the financial markets.

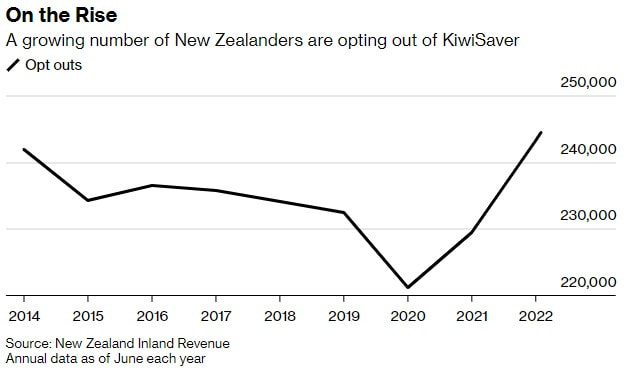

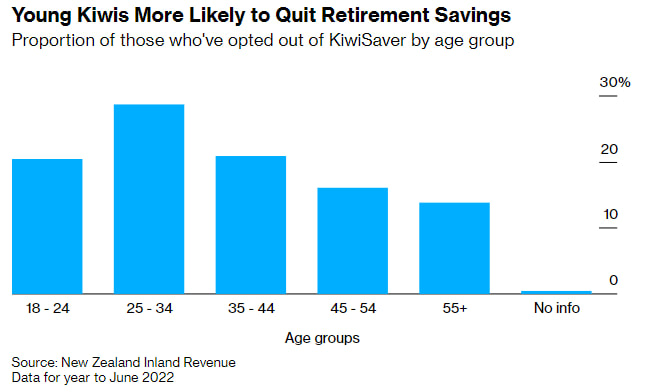

What Does the Data Say about Young New Zealanders who have Opted Out of KiwiSaver?

You're automatically enrolled in KiwiSaver when you start a new job in New Zealand. However, from 2022, young Kiwi workers are actively and increasingly choosing to opt out of KiwiSaver. The IRD has datasets to show that there's been a 6% increase in people opting out of the program between July 2021 and June 2022, the highest increase since data collection began in 2012. Most of those opting out are young, with 28% being in the 25-34 age group and 70% below the age of 45.

More young Kiwis opting out of KiwiSaver could be a warning sign of long-term consequences caused by an upcoming recession and rising interest rates. However, it’s not surprising to see an increase in opt-outs given the market volatility, inflation, and the rising cost of living.

More young Kiwis opting out of KiwiSaver could be a warning sign of long-term consequences caused by an upcoming recession and rising interest rates. However, it’s not surprising to see an increase in opt-outs given the market volatility, inflation, and the rising cost of living.

Source: Bloomberg and The Inland Revenue (IRD).

How Can I Take a KiwiSaver Savings Break?

One of the features of the KiwiSaver scheme is the ability to take a savings break (also known as a KiwiSaver Savings Suspension, which allows you to stop making contributions to your account temporarily.

A savings break can be taken for various reasons, such as experiencing financial hardship, purchasing your first home, or taking time off work to raise children. To take a savings break, you'll need to lodge the request via MyIR.

Know This:

A savings break can be taken for various reasons, such as experiencing financial hardship, purchasing your first home, or taking time off work to raise children. To take a savings break, you'll need to lodge the request via MyIR.

Know This:

- While you're on a savings break, your contributions will stop, but your KiwiSaver fund will remain open, and your balance will continue to earn interest (if in a cash fund) or returns (as the sharemarket moves). However, during a savings break, your employer won't be required to make any contributions to your account, and you won't be eligible to receive any government contributions.

- It's worth noting that taking a savings break can impact your retirement savings and your eligibility for the KiwiSaver first-home withdrawal. It’s important to weigh the benefits of a savings break against the potential impact on your savings before making a decision. Check out our definitive guide for a more detailed breakdown of taking a KiwiSaver savings break.

What are the Pros & Cons of Stopping Contributions to KiwiSaver?

Pros:

There are several reasons why Kiwis may choose to stop contributing to KiwiSaver:

There are several reasons why Kiwis may choose to stop contributing to KiwiSaver:

1. Increased disposable income

- Stopping contributions to KiwiSaver is becoming a more popular choice for people looking to increase their disposable incomes.

- By suspending their payments, someone would theoretically get the amount they would usually put into KiwiSaver as disposable income (which could be anywhere from 3% to over 10%) that could be used to cover expenses.

- In addition, by halting contributions, individuals may have more money available to cover necessities such as rent, groceries, and child care.

- Halting contributions can be especially beneficial for those facing financial pressures and struggling to meet their current expenses - giving up a 3% contribution on a $50,000 salary will direct around $125 (before tax) per month into someone's pocket.

2. Increased flexibility

- Another benefit of stopping contributions to KiwiSaver is that individuals may have more flexibility with their finances. By not contributing to KiwiSaver, individuals will likely have more control over how they allocate their money and may be able to use it for other financial goals, such as paying off debt or saving for a home.

- While the ~3% increase in cash flow might not seem like much, it can make all the difference for Kiwis paying 7%+ interest on mortgages and can add a buffer in case short-term/emergency expenses arise.

- Additionally, for those contributing more than the 3% minimum, stopping contributions to KiwiSaver could mean you increase your cash flow by up to 10% (before tax) depending on your contribution rate.

Cons:

There are several drawbacks to stopping contributions to KiwiSaver:

There are several drawbacks to stopping contributions to KiwiSaver:

1. Slower wealth accumulation and lower retirement savings

- Individuals miss out on the opportunity to grow their savings through investments. KiwiSaver funds are invested in various financial products, such as shares, bonds, and cash, and the value of these investments is designed to increase over time.

- By halting contributions, individuals may miss out on the potential growth of their savings and may have less financial security in their retirement.

2. Missing out on employer match and yearly government contributions

- By law, your employer is obligated to contribute a minimum of 3% to your KiwiSaver account if you're also contributing that amount. Therefore, stopping contributions may mean missing out on this additional investment if your employer provides a matching contribution above and beyond the 3% to your KiwiSaver account.

- Additionally, if you don't reach the minimum contribution amount (which, as of 2023, is $1,042.86) as set by IRD, you'll miss out on the $521.43 the government normally would put into your KiwiSaver account each year. This is, effectively, free money and forfeited if you stop contributing and don't meet the minimum.

There are are also long-term impacts of stopping KiwiSaver contributions as there are some serious consequences for individuals that don't contribute to retirement savings in the long term:

3. Shortfall of funds when you reach retirement age

- The potential financial difficulties that arise in the golden years of many New Zealanders cannot be understated. Without sufficient retirement savings, individuals may have to cut down on their usual spending or substantially adjust their retirement plans to ensure they can still support themselves without relying on their family members or the New Zealand government.

- However, relying on New Zealand Superannuation or family members may still be insufficient to meet their needs and could lead to financial difficulties.

- KiwiSaver savings are designed to help retirees live beyond the basic level provided for by superannuation payments. However, many New Zealanders retire without sufficient savings and face hardship in their golden years. The consequence of stopping contributions today may be a difficult retirement.

4. Over-reliance on New Zealand Superannuation

- As outlined above, without sufficient retirement savings, individuals may rely solely on New Zealand Superannuation for financial support in their old age. This sole reliance on New Zealand Superannuation may become an issue as New Zealand Superannuation alone may not meet their needs and could lead to financial difficulties.

- This trend could have negative consequences for both individual Kiwis and the New Zealand government, as those who stop contributing altogether, especially if their employer provides a matching contribution, may face a difficult retirement.

- For a further breakdown of New Zealand Superannuation, visit our guide.

5. Implications for the New Zealand pension system.

- Another drawback of stopping contributions to KiwiSaver is that it may negatively affect the New Zealand economy and society. As the population ages and more people retire, there may be a strain on government pension schemes if individuals don't have sufficient private savings to support themselves.

- This overreliance on the New Zealand pension system could lead to a crisis in the pension system and potentially cause financial difficulties for the government and the economy. How significant this becomes is yet to be seen - this Stuff.co.nz article from 2017 suggests the risks are significant

Know This: Cancelling your KiwiSaver contributions is unlikely to make a significant difference.

The reality is budgets need to be balanced which requires careful budgeting, self-restraint and financial planning. By doing so, you can ensure a secure financial future and your family whilst still making ends meet in the here and now.

Stopping contributions to KiwiSaver is not a decision to be taken lightly, as it will likely have long-term consequences on your financial security (and that of your family). So while it's understandable to consider stop contributing to keep up with financial pressures and a high cost of living, being fully aware of all the potential consequences (both short-term and long-term) is critical.

Stopping contributions to KiwiSaver is not a decision to be taken lightly, as it will likely have long-term consequences on your financial security (and that of your family). So while it's understandable to consider stop contributing to keep up with financial pressures and a high cost of living, being fully aware of all the potential consequences (both short-term and long-term) is critical.

Frequently Asked Questions

Can I stop my contributions to KiwiSaver at any time?

Yes, you can stop your contributions to KiwiSaver anytime by using myIR. However, it's important to consider this decision's long-term consequences before making it.

What happens to my KiwiSaver account if I stop my contributions?

If you stop your contributions to KiwiSaver, your account will remain open, and you will still be able to move funds or schemes. You also have access to any contributions you have already made for qualifying withdrawals such as first-home or reach the retirement age. While your contributions are suspended your fund will probably not grow as much as it would if you continued to contribute given the lack of new cash coming in.

Can I access my KiwiSaver savings if I stop my contributions?

Generally, you'll not be able to access your KiwiSaver savings until you reach the age of eligibility, which is currently 65 years old. However, this rule has some exceptions, such as financial hardship or when you're purchasing your first home.

Is it better to contribute to KiwiSaver or invest elsewhere?

Whether to contribute to KiwiSaver or invest in other financial products depends on your financial situation and goals. However, the "other financial products" you'll often invest in (such as ETFs, shares or bonds) might also be accessible through certain KiwiSaver funds.

If you choose to invest elsewhere rather than contributing to KiwiSaver, you'll lose out on the employer and government contributions associated with contributing to KiwiSaver. This makes KiwiSaver attractive as an investment opportunity, especially given the range of funds available.

If you choose to invest elsewhere rather than contributing to KiwiSaver, you'll lose out on the employer and government contributions associated with contributing to KiwiSaver. This makes KiwiSaver attractive as an investment opportunity, especially given the range of funds available.

What are some alternatives to stopping your KiwiSaver contributions?

If your finances are under pressure, and you want to free up some disposable income but don't want to risk your retirement or are anxious about the upcoming market recession, the only option is to reduce your contributions (if they're above 3% already). This contribution reduction can help to lower your expenses while still allowing you to save for retirement. For example, if you're currently contributing 8% of your pay to KiwiSaver, but your employer is only contributing 3%, consider reducing your contribution amount to the employer-match level (3%) rather than outright opting out.

What’s the ideal time to halt KiwiSaver contributions?

Halting current contributions for a few months (or even years) can be one option if you know short-term financial pressures won't get resolved in the medium term (12 months onwards). However, once you realise that your short-term financial problems turn into longer-term structural issues, it might pay to consider the longer-term ramifications of not contributing to KiwiSaver.

Figuring out a realistic solution to your financial pressures will become essential - diverting suspended KiwiSaver contributions into your bank account won't be so significant as to avoid ongoing hardship.

Figuring out a realistic solution to your financial pressures will become essential - diverting suspended KiwiSaver contributions into your bank account won't be so significant as to avoid ongoing hardship.

I’ve stopped contributing to KiwiSaver but am in a better financial position now and want to start contributing. Can I do this?

Yes - you need to visit myIR and restart contributions.

Who should I be stopping KiwiSaver contributions? When does it make sense to do so?

There's no right answer here. Whether you should stop KiwiSaver contributions will depend on your unique financial situation. However, stopping KiwiSaver contributions is completely rational if you struggle to make ends meet. The additional disposable income you get from not contributing to KiwiSaver can make all the difference to your living situation (spending on food, power, petrol or rent).

I've just started contributing to KiwiSaver (less than 12 months) but have had some financial difficulty and want to take a savings break. Can I do that?

Unlike when you’ve been contributing to KiwiSaver for more than 12 months, you'll be required to present evidence of financial hardship beyond your control. If your circumstances have changed due to reasons within your control, your application may not be approved.

Per the IRD's guidance, when you apply, they will need to see evidence of financial hardship for reasons outside your control. If your financial circumstances have changed for reasons within your control, your application may not be accepted.

The IRD states they will work with you to decide the right length of time. The default period for a savings suspension is 3 months. Depending on your circumstances, the IRD may give you up to 1 year.

Per the IRD's guidance, when you apply, they will need to see evidence of financial hardship for reasons outside your control. If your financial circumstances have changed for reasons within your control, your application may not be accepted.

The IRD states they will work with you to decide the right length of time. The default period for a savings suspension is 3 months. Depending on your circumstances, the IRD may give you up to 1 year.