Index Funds vs ETFs - The Definitive Guide

Our guide explains the risks and potential profits from both Index Funds and ETFs, and how they can both fit into your investing strategy.

Updated 30 June 2024

Summary of Index Funds vs ETFs:

Know this - fees and charges: Index funds and ETFs both charge annual management fees (expressed as a percentage), this fee comes out of the fund automatically on a daily basis. ETFs are bought on a sharemarket, which means you'll pay brokerage and face bid/offer pricing (the difference between the price available to purchase at and the true value of the units in the fund). Index funds have a number of advantages over ETFs, and we explore these in detail below.

Whatever your investing goals, there are a wide range of index funds and ETFs offering different investment strategies to suit your unique goals. However, despite initial appearances, ETFs and index funds are different in nature and costs. Our guide covers:

Warning - This guide is informational only - MoneyHub does not offer any investment advice, guidance or any opinion on investment options.

- Index Funds and Exchange Traded Funds (ETFs) offer investors opportunities to diversify their investments with one single purchase. However, there are some key differences to be aware of that this guide details.

- Index funds diversify their investments by following a particular index, buying and holding the investments that make up the index.

- An Exchange Traded Fund (ETF) is a fund that the units in that fund are bought and sold on a stock exchange via broker, rather than directly from the fund manager. ETFs can be both index tracking or actively managed.

- Unlike buying individual shares, index funds and ETFs lower risk through diversification – you're never investing in just one company. If one company underperforms, there are dozens or hundreds of other companies that can counteract the fall in the value of one company. This means index funds and ETFs are typically seen as a lower risk investment.

- Index funds, and ETFs that track an index, are growing in popularity because of the diversification benefits, lower fees, and typically consistent outperformance compared to actively managed funds.

Know this - fees and charges: Index funds and ETFs both charge annual management fees (expressed as a percentage), this fee comes out of the fund automatically on a daily basis. ETFs are bought on a sharemarket, which means you'll pay brokerage and face bid/offer pricing (the difference between the price available to purchase at and the true value of the units in the fund). Index funds have a number of advantages over ETFs, and we explore these in detail below.

Whatever your investing goals, there are a wide range of index funds and ETFs offering different investment strategies to suit your unique goals. However, despite initial appearances, ETFs and index funds are different in nature and costs. Our guide covers:

- Index Funds vs ETFs Comparison Table

- Index Funds - Pros, Cons and the Bottom Line

- ETFs - Pros, Cons and the Bottom Line

- Index Funds and ETFs - 5 Must-Know Facts

- Investing in Index Funds and ETFs with the Right Platform

Warning - This guide is informational only - MoneyHub does not offer any investment advice, guidance or any opinion on investment options.

|

|

Your consumer guide to Index Funds is sponsored by our friends at Kernel, a leading New Zealand-based index fund manager and investing platform.

|

Index Funds vs ETFs Comparison Table:

Comparison Facts |

Index Funds |

ETFs |

What are they? |

A portfolio of investments, following an index such as the NZX 20, or S&P500, or an index specific to an industry (i.e. a property sector index) or investing preference (i.e. an ethical investment index). Index funds invest to match the holdings and performance of the index it tracks. |

A portfolio of investments that can be either actively managed or index tracking. Active ETFs are managed by professional fund managers and aim to beat the market; passive ETFs follow a benchmark index. |

Who are they best for? |

Anyone looking for investment diversification, low-fees and are comfortable following a benchmark. |

Anyone looking for investment diversification to spread the risk. Additionally, anyone unwilling to take the time to research individual companies to invest in. |

What are the fees? |

Ongoing fees: Annual management fees, which are expressed in a percentage like 0.35% or 0.65% etc. Membership fees: Some index fund investing platforms, such as Kernel charge a monthly or annual membership fee. Other platforms, such as InvestNow and Simplicity Investment Funds do not. |

One-off fees: Same as Shares' fees (as ETFs need to be bought and sold on a share market). We explore how this works (and what it costs) in the section below. Ongoing fees: Annual management fees, known as "expense ratios". It's expressed in a percentage like 0.60% or 1.25% etc. |

How and where can I buy them? |

New Zealand ETFs: Sharesies InvestNow Smartshares ASB Securities Jarden Direct Any Sharebroker ASX (Australian) ETFs: Sharesies Superhero Tiger Brokers (NZ) ASB Securities Jarden Direct US ETFs: Hatch Stake Sharesies Superhero Tiger Brokers (NZ) |

Understanding Tax and Trading Costs for ETFs and Index Funds

Index funds and ETFs have some key differences when it comes to tax and buying and selling costs, as we outline below:

Tax - New Zealand ETFs are classed as listed PIEs, which means the tax rate is fixed at 28%. If you pay a lower tax rate, you'll have to claim the overpaid tax from the IRD on your tax return at the end of the financial year. This will appear as a credit to offset any other personal tax. If you are investing for a child or charity, where there is no other taxable income to offset the tax credits against, you may be over taxed using an ETF. If you've invested in an overseas ETF, i.e. via Hatch, Stake or Sharesies, you will pay specific US tax as well as NZ tax (via an IR3 form). Index funds are different - tax is deducted at the correct rate and paid directly to the IRD. Unlike ETFs, index funds don't have a tax effect which sees a portion of your investment sitting idle until tax return time.

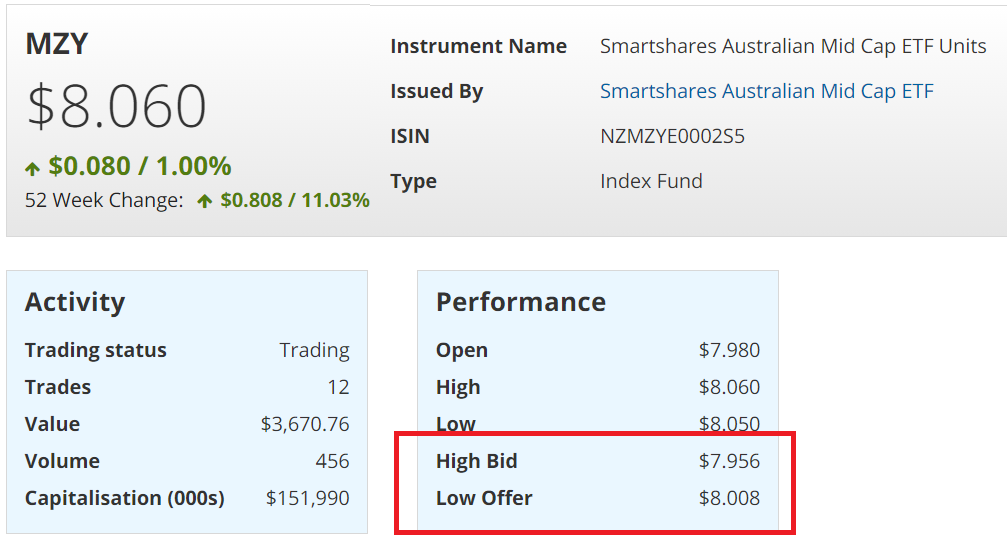

Trading Costs - buying and selling ETFs incurs three costs - brokerage (buying and selling fees), price spread (you can see that the Smartshares MZY as an example) and registry fees (separate fees that are incurred on any trade for using the specific share market). Index funds avoid brokerage, price spreads or registry fees.

Tax - New Zealand ETFs are classed as listed PIEs, which means the tax rate is fixed at 28%. If you pay a lower tax rate, you'll have to claim the overpaid tax from the IRD on your tax return at the end of the financial year. This will appear as a credit to offset any other personal tax. If you are investing for a child or charity, where there is no other taxable income to offset the tax credits against, you may be over taxed using an ETF. If you've invested in an overseas ETF, i.e. via Hatch, Stake or Sharesies, you will pay specific US tax as well as NZ tax (via an IR3 form). Index funds are different - tax is deducted at the correct rate and paid directly to the IRD. Unlike ETFs, index funds don't have a tax effect which sees a portion of your investment sitting idle until tax return time.

Trading Costs - buying and selling ETFs incurs three costs - brokerage (buying and selling fees), price spread (you can see that the Smartshares MZY as an example) and registry fees (separate fees that are incurred on any trade for using the specific share market). Index funds avoid brokerage, price spreads or registry fees.

Bid/Offer differential, typical of any ETF purchase or sale. The buyer offers a lower amount than what the seller wants to accept, meaning the price isn't always clear. The price you pay may also not align to the actual underlying value of the units in the fund. Source: nzx.com/instruments/MZY (please note prices will have changed)

Index Funds - Pros and Cons

Pros:

Cons:

- Index funds make investing easy and remove the need to research individual companies: The index buys and sells shares on your behalf and never deviates from the investing strategy.

- Research backs up the investment: It's well-accepted that investors are, in most instances, better off buying into an index than individual shares, given that markets out-perform the vast majority of individual shares, and actively managed funds, in the long run. The same philosophy generally applies to passively structured ETFs as well.

- The fees are low: Index funds charge as little as 0.03% p.a. in management fees, whereas some ETFs charge more, and have to pay ongoing listing fees which eats into returns.

- Index funds offer diversity: Not only does investing in an index fund give you diversity, there are also a range of index fund strategies available to suit your unique goals.

- Buying at the true value: With an index fund, you are purchasing units directly from the fund manager at the true value of the underlying investments, whereas with an ETF the price you pay for your units may differ to their actual value.

- Low minimum investment: A lot of index funds can now be access through investing platforms, such as Kernel, with as little as $1.

- New Zealand managed index funds are PIEs - If you're buying index funds in New Zealand, all the Kernel index funds are PIEs which means you have flexibility the investment returns are taxed at a top rate of 28% which benefits top-rate taxpayers.

Cons:

- No downside protection: When the market index sinks, the fund's value sinks with it. An actively managed fund may sell off everything to avoid further losses. An index fund rides the ups and downs exactly like the index itself. Although, over time it is proven to be very difficult for active managers to do this accurately and index funds over the long term out-perform the vast majority of actively managed funds.

- No control over holdings: You don't get to pick what shares you invest in.

- Limited exposure to different investing strategies: Index funds simply follow an index, so if a new company lists on the sharemarket, it's unlikely any index fund will include it until it falls within the investment strategy. Also, if a company is performing poorly, the index fund will continue to hold it until it no longer meets the requirements of the fund - for example, the market capitalisation becomes too small. This means losses can be incurred while other investors sell off their poor-performing investments.

ETFs - Pros and Cons

Pros:

Cons:

- Diversification - Just like index funds, ETFs invest into dozens or hundreds of individual companies, so the risk is spread

- Targeted options - ETFs, also like index funds, may focus on a particular investment type, such as companies in the NZX20 shares, energy sector or banking sector.

- Convenience - ETFs don't require the investor to do anything, other than buy and sell their holding when they need to.

- Low minimum investment - ETFs can be purchased using investment platforms like Sharesies, Hatch and Stake for as little as a few dollars.

- New Zealand-listed ETFs are Listed PIEs - If you're buying ETFs in New Zealand assets, all the Smartshares ETFs are Listed PIEs which means the investment returns are taxed at a fixed rate of 28% which benefits top-rate taxpayers.

Cons:

- Annual expense ratios and trading fees - ETFs charge an annual fee, just as a managed fund or KiwiSaver fund does, and you'll also be charged brokerage when you buy and sell. How much you pay depends on the platform. For example, buying Smartshares is free with InvestNow, but you'll pay a fee if you use Sharesies. ETFs listed on US markets can be bought using Hatch or Stake.

- If you buy an ETF in a non-NZD currency, the value of your investment in New Zealand Dollars will change as the exchange rate goes up and down. This means if the NZD gets stronger against, for example, the USD, any ETFs held in USD will reduce in value (in NZD).

- New Zealand-listed ETFs are Listed PIEs. Listed PIEs pay tax at a fixed rate of 28%, this means if you are investing on behalf of a child you may be over taxed, whereas with an index fund it will automatically be taxed at the correct tax rate.

- More research required: As ETFs can be either actively managed or index tracking, investors need to careful research each ETF to ensure they are investing in strategy that they are after.

Investing in Index Funds and ETFs - 5 Must-Know Facts

Whether you decide to invest in index funds, ETFs, or both, there are some smart ways to save money to increase your profits in the short and long-term. We outline the most important facts below.:

|

ETFs and Index Funds charge investors in similar and different waysTo understand how ETFs and Index Funds differ, we explain the fees:

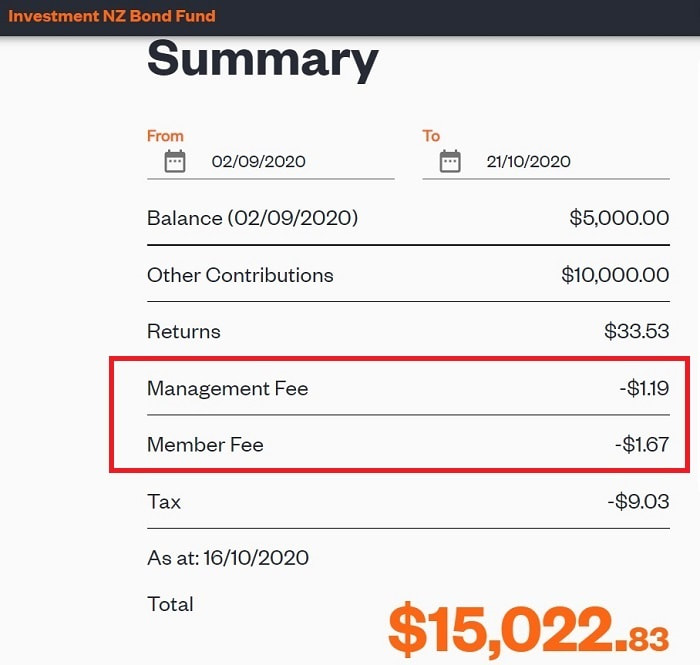

An example of an index fund (the Simplicity NZ Bond Fund) which shows both the management fee and member fee being deducted as a cash expense against the returns

|

|

Index Funds may require a higher minimum investment than ETFs (and charge ongoing membership fees)In many cases, ETFs may have a lower minimum investment than index funds. Most of the time, all it takes to invest in an ETF is the amount needed to buy a single share, and some brokers, such as Hatch, even offer fractional shares..

If you have only a small amount to invest (i.e. less than $500 or $1,000), consider two options: an ETF with a share price you can afford, or an index fund that has no minimum investment amount, such as Kernel which offers index funds for as little as $1. You'll also need to avoid the trap of platform or membership fees - annual charges for being a customer, which some fund managers still charge. To avoid any issues, always understand ALL the one-off and ongoing costs before investing in an ETF and/or index fund. |

|

There are more Index Funds and ETFs available in New Zealand than ever beforeNew entrants to the market such as Simplicity Investment Funds and Kernel Wealth offer more index funds, while Smartshares launched 10+ new ETFs in 2020 which invest locally and overseas. Stake and Hatch, which offer US-based investing, offer hundreds of American-listed ETFs. Generally, the management fees range from 0.10% to 0.70% p.a. In summary, New Zealand has gone from 20+ index funds and ETFs to 1,000+ since the launch of new platforms.

Know this: US-listed ETFs continue to outperform NZX-listed ETFs on fees. A research report by GoodReturns.co.nz stated that some (but far from all) US equity ETFs are very cheap and in some cases offer an expense ratio less than 0.10% - but not always. Before making any decision, compare the fees of the ETF you're looking at with the NZX Smartshares equivalent (if there is one). Do note that while the management fees may be lower on some large international funds, you will likely pay higher tax and transaction fees that will make a NZ based index fund more attractive after all costs are considered. Exchange rate risk: Please remember that if you invest in the US directly with a platform such as Hatch or Stake, your investment will be in US Dollars. This means that that if the NZD strengthens against the USD, your investment will be worth less. And vice versa. Where can I find information about US-listed ETFs? Websites like The Balance publish independent insights into ETFs which can help your investment decision-making process. |

|

Neither Index Funds nor ETFs offer the upside or excitement of picking an undervalued shareSuperstar shares like Xero (50 cents to $100+) and a2 Milk (25 cents to $15+) do exist, but neither index funds or ETFs will give you much exposure. This is because both investment options focus on diversifying risk; going all-in on Xero may seem obvious now, but no investment manager would ever take sure a risk.

For this reason, index funds and ETFs don't offer the huge gains that come from picking a winner. However, on the flip side, they do protect investor money (in the long term) by being thoroughly diversified. Many shares have gone from $5 to 5 cents, destroying investor wealth along with it. Anyone investing in index funds or ETFs has a similar strategy which is usually to let the investment manager do the work. The investor will then plan to cash out in the long term. |

|

Index Funds and ETFs don't just invest in shares - they offer exposure to many different asset typesIndex Funds and ETFs invest in shares, but not always. Many index funds and ETFs invest in bonds, a mix of shares and bonds, currencies, commodities, and more. By doing so, the index funds and ETFs offer investors exposure to non-equity assets, thus diversifying exposure beyond the sharemarket.

What you invest in will depend on what ETF and/or index fund you select. Just because they're not actively managed doesn't mean there are limited growth opportunities - the NZX20 doubled between 2016 and early 2020, meaning investors would have seen their NZX20-following index fund double in value too. |

Conclusion: Investing in Index Funds and ETFs with the Right Platform

Many investors decide to buy into index funds and ETFs, as each has its unique advantages. Both are regarded as long-term investments. To be able to invest in index funds and/or ETFs, you'll need to sign up to an appropriate investment platform or make a direct purchase.

The best approach is to minimise monthly platform fees by choosing an investment platform that offers high quality ETFs and/or index funds that align with your investment objectives. This lets you diversify your investments while reducing fees. Popular options for index funds and ETFs include:

The best approach is to minimise monthly platform fees by choosing an investment platform that offers high quality ETFs and/or index funds that align with your investment objectives. This lets you diversify your investments while reducing fees. Popular options for index funds and ETFs include:

- Kernel (offers index funds which invest in New Zealand and overseas markets)

- Sharesies (offers managed funds, ETFs and individual shares in NZ and US markets)

- InvestNow (offers managed funds, index funds, ETFs and individual shares)

- Smartshares (offers ETFs which invest in New Zealand and overseas markets)

- ASB Securities (offers ETFs and individual shares in New Zealand markets)

- Jarden Direct (offers ETFs and individual shares in New Zealand markets)

- Hatch Invest (offers US-listed shares at ETFs)

- Stake (offers US-listed shares at ETFs)

|

|

Your consumer guide to Index Funds is sponsored by our friends at Kernel, a leading New Zealand-based index fund manager and investing platform.

|