What is the OCR? The Official Cash Rate Explained

Understand the Official Cash Rate (OCR) with our comprehensive guide and how it impacts personal finances such as loans, mortgages, and investments, and its broader effects on the economy. With insights into how OCR changes influence different sectors and practical strategies to navigate these changes, this guide is a must-read for informed financial decision-making in New Zealand.

Updated 21 June 2023

Summary

This guide aims to provide every New Zealander with a comprehensive understanding of the OCR, its determination, and its role in the New Zealand economy. By gaining insights into the OCR, better-informed decisions about personal finances can be made, given movements in the OCR affect everything from how much you can earn on a term deposit to how much a mortgage, personal loan, car loan and credit card will cost. We cover:

Know This First: Different sectors of the economy can react differently to OCR changes.

Summary

- The Official Cash Rate (OCR) is essential to New Zealand's monetary policy framework. It plays a pivotal role in influencing New Zealand's short-term interest rates, affecting the cost of borrowing and deposit rates for consumers and businesses.

- Understanding the OCR is crucial for making informed decisions about personal finances, such as loans, mortgages, and investments.

- For consumers, the OCR impacts the interest rates on loans, mortgages, and savings accounts. For example, borrowing costs typically rise when the OCR increases, and savings rates improve.

- In contrast, decreasing the OCR generally leads to lower borrowing costs and less favourable savings rates.

- Changes in the OCR can influence consumer spending, saving, and investment behaviour, ultimately affecting the broader economy.

This guide aims to provide every New Zealander with a comprehensive understanding of the OCR, its determination, and its role in the New Zealand economy. By gaining insights into the OCR, better-informed decisions about personal finances can be made, given movements in the OCR affect everything from how much you can earn on a term deposit to how much a mortgage, personal loan, car loan and credit card will cost. We cover:

- Understanding the Official Cash Rate (OCR)

- How OCR Changes Impact Consumers

- Simple Strategies for New Zealanders to Navigate OCR Changes

- Understanding the Historical Context of the OCR and Our Helpful Glossary

- Frequently Asked Questions

Know This First: Different sectors of the economy can react differently to OCR changes.

- Retail Sector: A lower OCR typically means lower interest rates, increasing consumer spending power. This increase can stimulate retail sales.

- Manufacturing Sector: Lower interest rates can stimulate investment in capital goods, boosting the manufacturing sector. Conversely, high-interest rates might deter such investment.

- Housing Market: OCR influences mortgage rates. A low OCR often leads to lower mortgage rates, stimulating housing demand and potentially raising house prices. Conversely, a high OCR can lead to higher mortgage rates, potentially.

MoneyHub Founder Christopher Walsh explains his views on the OCR and how it affects every New Zealander:"Any movement in the OCR creates winners and losers. For example, mortgage-free retirees with cash savings will benefit from an OCR rise, given interest payments will increase. This increases their disposable income and makes retirement more enjoyable. However, anyone with a mortgage, such as working families, will face higher repayment costs in one way or another, therefore reducing how much disposable income and making keeping up with costs a little harder.

This guide is published to help New Zealanders understand OCR changes and how they affect everyone at different moments in their life. While 0.25% OCR rates are a thing of the past and probably won't be repeated, given their effects on inflation and housing affordability, every move in the OCR is relevant and important to understand. If you have questions, please contact our research team, as our focus is making sure we explain the OCR as clearly and comprehensively as possible". |

Christopher Walsh

MoneyHub Founder |

Understanding the Official Cash Rate (OCR)

The Official Cash Rate (OCR) is the interest rate set by the Reserve Bank of New Zealand (RBNZ), which serves as a benchmark for short-term interest rates in New Zealand. The OCR is the rate at which commercial banks (e.g. Westpac, BNZ, Kiwibank) can borrow from or deposit funds with the RBNZ. In turn, the OCR influences the interest rates commercial banks charge their customers for loans and pay on deposits.

How is the OCR determined?

The OCR is determined by the RBNZ's Monetary Policy Committee (MPC), which meets approximately every six weeks to review and set the OCR. The MPC considers various factors when making its decision, including domestic and global economic conditions, inflation forecasts, and the overall health of the financial system.

The primary objective of the RBNZ's monetary policy is to maintain price stability, which means minimising inflation. While the cost of living is at an all-time high, New Zealand has traditionally been low inflation and has kept the annual increase in the Consumers Price Index (CPI) within a target range of 1-3%. However, this has not been the case since the global pandemic.

What is the role of the Reserve Bank of New Zealand (RBNZ) in the OCR?

The RBNZ is New Zealand's central bank, responsible for formulating and implementing monetary policy to maintain price stability and support maximum sustainable employment. As part of its mandate, the RBNZ sets the OCR to influence short-term interest rates, manage inflation, and foster a stable financial system. By adjusting the OCR, the RBNZ can either stimulate or dampen economic activity, depending on the current economic conditions and the desired policy outcomes.

How is the OCR determined?

The OCR is determined by the RBNZ's Monetary Policy Committee (MPC), which meets approximately every six weeks to review and set the OCR. The MPC considers various factors when making its decision, including domestic and global economic conditions, inflation forecasts, and the overall health of the financial system.

The primary objective of the RBNZ's monetary policy is to maintain price stability, which means minimising inflation. While the cost of living is at an all-time high, New Zealand has traditionally been low inflation and has kept the annual increase in the Consumers Price Index (CPI) within a target range of 1-3%. However, this has not been the case since the global pandemic.

What is the role of the Reserve Bank of New Zealand (RBNZ) in the OCR?

The RBNZ is New Zealand's central bank, responsible for formulating and implementing monetary policy to maintain price stability and support maximum sustainable employment. As part of its mandate, the RBNZ sets the OCR to influence short-term interest rates, manage inflation, and foster a stable financial system. By adjusting the OCR, the RBNZ can either stimulate or dampen economic activity, depending on the current economic conditions and the desired policy outcomes.

Factors Influencing the Official Cash Rate (OCR):

Before deciding, the Reserve Bank looks at various factors to help decide whether the OCR should increase, stay the same or decrease. These factors include:

- Inflation targeting: The OCR is one of the tools that the Reserve Bank of New Zealand (RBNZ) uses to manage inflation. The goal is to keep inflation within a target range, typically 1-3%. If inflation is rising too quickly, the RBNZ might increase the OCR to cool down the economy. Conversely, if inflation is too low or the economy is sluggish, the RBNZ might lower the OCR to stimulate growth.

- Economic growth: The RBNZ uses the OCR to help manage the country's economic growth. When the economy is booming, the RBNZ may increase the OCR to prevent overheating, while during economic downturns, the RBNZ can lower the OCR to stimulate spending and investment.

- Employment levels: The level of employment is another key consideration. High unemployment can lead to lower OCR to stimulate job growth, while low unemployment might prompt a higher OCR to prevent the economy from overheating.

- Global economic conditions: The OCR can be influenced by global economic trends and crises. If overseas economies are struggling, the RBNZ may lower the OCR to protect NZ's economy.

- Fiscal and monetary policies: The government's fiscal policy and the RBNZ's monetary policy also play a role. The OCR can be adjusted to complement these policies to achieve economic stability and growth.

How OCR Changes Impact Consumers

The OCR is always in the news now because increases significantly affect household costs, given mortgage rates increase. However, OCR movements go up and down and affect the following:

- Borrowing costs: A lower OCR usually means lower interest rates on loans, making it cheaper to borrow for a house, car, or other major purchases. Conversely, a higher OCR can mean higher borrowing costs.

- Savings and investment returns: OCR increases typically lead to higher interest rates on savings accounts and other interest-bearing investments, benefiting savers. Conversely, OCR decreases often mean lower returns for savers.

- Consumer spending and confidence: Lower interest rates can encourage more spending as borrowing is cheaper, boosting the economy. However, higher interest rates may make consumers more cautious about spending.

- Housing market and affordability: Lower OCR can lead to lower mortgage rates, potentially boosting the housing market. But, it could also lead to increased housing prices. Conversely, higher OCR can have the opposite effect.

- Exchange rates and imported goods prices: A higher OCR can attract foreign investors, potentially increasing the value of the NZ dollar. This can make imported goods cheaper but can make exports more expensive for foreign buyers, however it's not always the case - the inflation level and economic outlook will also affect the strength of the NZD.

Case Studies: Impact of OCR Changes

To further explain how the OCR affects personal financial decisions, let's consider a couple of hypothetical scenarios:

Know This: These case studies underline how crucial it is to understand the implications of the OCR on individual financial circumstances.

- Case Study 1: Jane, a homeowner with a floating mortgage rate, experiences how an increase in the OCR results in a hike in her mortgage payments. This change impacts her monthly budget, prompting her to cut down on other expenses.

- Case Study 2: Peter, a retiree, has a term deposit. When the OCR decreases, the interest on his deposit reduces, affecting his income from savings. As a result, Peter has to reassess his retirement strategy and consider other investment options to maintain his lifestyle.

- Case Study 3: Sarah and Rangi, first-time home buyers, are approved for a home loan. They are keeping a keen eye on OCR trends. Noticing a predicted rise in the OCR, they decide to lock in their mortgage at a fixed rate now to avoid paying higher interest in the future.

- Case Study 4: Emma, a student, has been saving for her post-graduate studies in a high-interest savings account. As the OCR falls, so does the interest rate on her savings. To ensure her savings don't stagnate, she is considering shifting her savings to other investment types that pay higher interest.

- Case Study 5: Grace, a young professional with a variable-rate car loan, experiences the impact of a rising OCR. As the OCR increases, her monthly loan payments go up. She decides to refinance her car loan to a fixed rate to keep her payments stable.

Know This: These case studies underline how crucial it is to understand the implications of the OCR on individual financial circumstances.

Simple Strategies for New Zealanders to Navigate OCR Changes

Understanding the OCR and its potential changes is one thing, but knowing how to respond to them is another. The OCR plays a significant role in the financial decisions you make. Its variations can have immediate and long-term impacts on your finances, whether you are a borrower, a saver, an investor, or a retiree.

As such, it's essential to have a strategy to navigate these changes effectively. The following strategies are aimed at different financial profiles and can help you make the most of your financial situation, regardless of OCR fluctuations:

As such, it's essential to have a strategy to navigate these changes effectively. The following strategies are aimed at different financial profiles and can help you make the most of your financial situation, regardless of OCR fluctuations:

- Borrowers: Watch the trends in OCR. If it looks like rates will rise, consider locking in your interest rate. You might want to opt for a variable-rate loan if rates are falling.

- Savers and investors: When OCR rises, consider options like term deposits which benefit from higher interest rates. When OCR falls, you might consider a non-cash investment (such as an index fund) to maintain returns.

- Managing household budgets: Changes in OCR can affect household expenses, especially if you have a variable rate mortgage or personal loan which rolls over to an adjusted rate. Keep a close eye on your budget and adjust as needed - higher interest rates on big borrowing holds many New Zealanders back.

- Long-term financial planning: Consider how OCR trends affect your long-term financial goals - you may want to minimise debt and maximise cash investments if the OCR is high, or look to invest in the NZX if the OCR is low and inflation is under control.

Staying Informed about OCR Developments

- Monitor OCR announcements: The RBNZ regularly releases updates on the OCR, as outlined on their website.

- Follow RBNZ statements and reports: The RBNZ provides detailed reports and analysis (as per this May 2023 example) behind their decisions. These can give you a deeper understanding of the economic trends influencing the OCR.

- Keep up with economic news and expert opinions: Interest.co.nz's OCR section is arguably New Zealand's best source - you can follow their stories here.

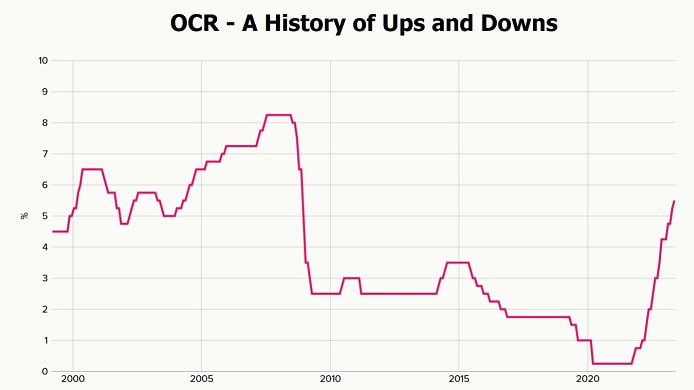

Understanding the Historical Context of the OCR and Our Helpful Glossary

It's helpful to look back at the history of the OCR to gain insights into how this benchmark rate influences the financial market and consumer decisions. In summary:

- Over the past few decades, the OCR has seen both hikes and falls. During periods of economic growth, the OCR has typically increased to prevent inflation from spiralling out of control. Conversely, during economic downturns, like the Global Financial Crisis in 2008 and the COVID-19 pandemic, the OCR was significantly lowered to stimulate economic activity - low borrowing costs usually lead to economic growth.

- Notably, the OCR reached an all-time low during the COVID-19 pandemic to ease the economic shock, which brought about a surge in the housing market due to lower mortgage rates.

- The increases of the OCR from the 2020 record lows had seen the OCR increase over 5.00% from August 2021, when it was held at 0.25% to when it increased to 5.25% (from 4.75%) on 5 April 2023.

Glossary

- Inflation: The rate at which the general level of prices for goods and services is rising, eroding purchasing power.

- Monetary Policy: Policy set by the central bank to control the money supply in the economy and manage inflation and economic growth.

- Consumer Price Index (CPI): An index measuring the average price of consumer goods and services households purchase. It's often used to assess inflation levels.

- Interest Rate: The proportion of a loan charged as interest to the borrower, usually expressed as an annual percentage of the loan outstanding.

- Official Cash Rate (OCR): The interest rate set by the Reserve Bank of New Zealand (RBNZ), which affects the short-term interest rates banks offer to their customers. The OCR is used as a tool for maintaining price stability within the economy.

- Reserve Bank of New Zealand (RBNZ): New Zealand's central bank, responsible for operating monetary policy to maintain price stability, promoting the maintenance of a sound and efficient financial system, and meeting the currency needs of the public.

- Gross Domestic Product (GDP): The total value of all goods and services produced within a country's borders over a specific period. It serves as a comprehensive measure of a nation's overall economic activity.

- Unemployment Rate: The percentage of the total labour force that is jobless and actively seeking employment.

- Inflation Targeting: A monetary policy strategy the central bank uses where a specific inflation rate is targeted. The RBNZ's goal is to maintain an annual rise in the CPI within a target range, typically 1% to 3%.

- Current Account: The sum of the balance of trade (exports minus imports of goods and services), net income from abroad, and net current transfers. A positive current account balance indicates the nation is a net lender to the rest of the world, while a negative current account balance indicates that it is a net borrower.

- Fiscal Policy: Government policy regarding taxation, government spending, and public debt. Managed by the government rather than the central bank, it is primarily aimed at economic growth and stability.

Frequently Asked Questions

What is the current OCR in New Zealand?

The current OCR is regularly updated on the Reserve Bank of New Zealand's website; you can see this on their website.

How often does the OCR change?

The OCR is typically reviewed seven times a year by the Monetary Policy Committee of the RBNZ, as outlined on their website.

How does the OCR affect inflation?

The OCR influences the cost of borrowing and the return on savings, which can impact spending and investment levels in the economy. These changes in demand can then affect price levels, i.e., inflation.

Does the OCR directly affect the interest rate of my loan or savings account?

While the OCR does not directly determine the interest rates on loans or savings accounts, it influences these rates as banks often pass on OCR changes to their customers. Our guides to the best term deposits, savings accounts and call accounts have more details.

Why does the OCR change?

The OCR changes to help control inflation and stabilise the country's economic activity. For example, if inflation is high, the Reserve Bank may increase the OCR to cool down the economy. Conversely, if economic activity is sluggish, they may lower the OCR to stimulate spending and growth.

How does the OCR affect the average person?

The OCR can affect the interest rates on your mortgage, your savings account, and other loans. When the OCR goes up, interest rates often rise too, which means your mortgage could cost more, but your savings might also earn more interest.

How does the OCR affect businesses?

A change in the OCR can impact the cost of business loans. When the OCR and, consequently, interest rates are low, it's cheaper for businesses to borrow money for expansion or other investments.

What does a low OCR mean for the housing market?

A low OCR often leads to lower mortgage rates, stimulating housing demand and potentially increasing house prices. But it can also lead to more borrowing and higher levels of household debt.

Does the OCR affect the NZX?

While the OCR doesn't directly influence stock prices, changes in the rate can affect the overall economy, which in turn can influence investor sentiment and the stock market.

How does the OCR affect the New Zealand dollar?

A higher OCR can attract foreign investors, potentially increasing the value of the NZ dollar. This can make imported goods cheaper but can make exports more expensive for foreign buyers.

Does the OCR affect all banks the same way?

While all banks in New Zealand are affected by changes in the OCR, how they respond might differ. Some might pass the change to customers immediately, while others might not.

Does the OCR have an impact on unemployment rates?

Indirectly, yes. Changes in the OCR can influence the level of economic activity, which can then affect employment. For example, a lower OCR can stimulate economic growth and potentially lead to more job creation.

What happens if the OCR goes to zero or negative?

If the OCR goes to zero or negative, it could lead to lower interest rates on loans, potentially stimulating borrowing and economic activity. However, it could also lead to lower returns on savings and deposits.

Why does the RBNZ sometimes decide to keep the OCR steady?

The RBNZ might decide to keep the OCR steady if they believe the current rate is consistent with maintaining low and stable inflation and full employment.

Related Guides:

Mortgage Essentials:

Other Mortgage Options:

Alternative Mortgage Options:

Mortgage Management:

Mortgage Essentials:

- Best Home Loans Offers

- Mortgage Calculator

- How Much Can I Borrow?

- Mortgage Repayment Calculator

- Mortgage Options

- Mortgage Cashback

Other Mortgage Options:

- Interest-Only Mortgages

- Interest-Only Mortgage Calculator

- Revolving Credit Mortgages

- Offset Mortgages

- Offset Mortgage Calculator

- Fixed vs Floating Mortgage Rate Calculator

Alternative Mortgage Options:

Mortgage Management: