Saving for a House Deposit as a Young Professional in New Zealand

Our guide explains why saving for a house deposit is challenging, the reality of choices and sacrifices, must-know facts and frequently asked questions.

Updated 24 January 2024

Summary:

Our guide covers:

Know This First: Homeownership in similar ways, but the common theme to being able to save a sufficient deposit is being financially secure:

Summary:

- With relatively high inflation in recent years, coupled with higher interest and mortgage rates and a tightening of lending policy from banks (largely driven by the RBNZ's push to implement Debt to Income Restrictions), it has never been more challenging to try and save up for a house deposit.

- This culmination of factors has put pressure on all New Zealanders (those with houses, mortgages, and renting). However, younger New Zealanders such as Generation Z (Gen Z) that have just entered the workforce (the oldest cohort aged 26) have probably been impacted the most given that they've had limited time in the workplace to earn and save and are likely to be in a far worse financial position than their parents.

Our guide covers:

- 10 Reasons Why Saving For a House Deposit as a Young New Zealander is Challenging

- Saving For a House Deposit - Money, Choices, Sacrifices and Reality

- Is Buying a House Right for You and Your Long-Term Needs? Understanding the Realities of Homeownership

- Must-Know Facts about Young Professionals Saving for a House Deposit

- Frequently Asked Questions

Know This First: Homeownership in similar ways, but the common theme to being able to save a sufficient deposit is being financially secure:

- This means having little or no credit card and personal debt, a KiwiSaver balance to draw on, living at home while saving, working overtime to make more money, spending carefully, working overseas, relocating to the regions and/or accepting family help.

- Investing can also help, given that capital gains for NZX-listed shares and most ASX-listed shares are tax-free. However, it can also go wrong and reduce money for a deposit. Finally, limiting social activities and delaying other major life events to prioritise saving for a home.

MoneyHub Founder Christopher Walsh Explains Why We've Published this Guide:

|

"New Zealand is undoubtedly one of the best places to live, but it has financial hurdles. Getting into a position to buy a house has become increasingly difficult, with low incomes being dwarfed by high house prices. This has led to an owners vs renters situation in New Zealand, which no government seems interested in addressing the inequality that arises from a lifetime of being unable to own a home.

There's no shortcut to a house deposit. I moved from Otago to Auckland in 2007 and rented a room in a giant house close to Ponsonby Road for $70/week (back then, everyone else I knew lived at home or was paying $200+ a week). I made it work and benefited from low overheads, but those days are long over. Graduate salaries have remained flat, rents have gone up (my cheap flat is now a boutique hotel with rooms from $500+ a night), and living costs in New Zealand haven't come down. I can't emphasise enough how important it is to get control of your money and familiarise yourself with your spending habits. Unless you're getting an entire house paid for by the bank of Mum and Dad, a lot of your earnings will likely go to housing costs. Having enough money to have choices is essential to being happy and minimising stress. Money is scarce, and every dollar saved can contribute to a house deposit. We live in an era where credit cards, automated payments, subscriptions, and impulse online purchases are the norm. I posted this guide on Reddit in December 2023, and the top comment suggested to track your net worth every month. I agree with this - it will motivate you to keep growing. This guide does not suggest anyone lives like a monk for ten years while they save up. Instead, we explain ways to get connected with your money. Please make analysing your expenses so familiar that you know where every dollar goes. This will give you the confidence to make smart decisions. I suggest considering a budgeting app (or something like the budget app meets high-interest paying Savvy account) which are designed to get you to spend wisely, live happily and maximise your earnings to give you options and freedom. For most New Zealanders, owning a home can be achieved - we don't want you to miss your window when establishing good habits will give you more and last a lifetime". |

Christopher Walsh

MoneyHub Founder |

10 Reasons Why Saving For a House Deposit as a Young New Zealander is Challenging

There are many reasons why it’s more difficult for young New Zealander professionals to save up for a house deposit:

|

Burdened with debt (student loans, credit cards, car payments)With the Fees Free government incentive that provides the first year of university or trade school free after New Zealanders finish college, coupled with the cultural norm of doing further study/training, it's never been more common for young New Zealanders to take out student loans and complete a degree. This often means that young graduates starting in the working world frequently come out with student loan debt.

A few insights from the Victoria University of Wellington 2022 Study:

Once New Zealanders with student loan balances start working, they must mandatorily pay 12% of each dollar earned above the repayment threshold (the annual repayment threshold is $22,828 for the 2024 tax year). Additionally, if young New Zealanders have moved to a new city that's not their home town, it's increasingly common to turn to credit cards or car financing to make the move work. Bringing all this together, a young grad’s take-home salary gets reduced to around 70% of their gross pay. While this sounds impressive, student loan repayments, credit card instalments, car financing payments, rent, food, and other discretionary spending (which we discuss below) make it difficult to save significant sums in the early years of working life. |

|

High mortgage ratesThe typical mortgage rate now sits between 7 - 8% p.a. depending on the duration (with variable rates 8.50% and above). This risks causing rental increases, as landlords need to cover their interest costs, taking away money that could be saved for a deposit.

However, it's likely that dual-income households that are decades into their careers earning six-figure incomes would struggle to get approved on a million-dollar mortgage at 8% mortgage rates. If these types of applicants are struggling, it's near impossible for younger New Zealanders (especially those on single incomes) to be able to afford mortgages. |

|

Low graduate salariesGenerally, there's a strong correlation between salary and years of experience. When young graduates enter the workforce, they have nearly zero working experience, so their graduate salaries will typically be at the lowest point in their careers.

Additionally, employers know that there are far more hungry graduates looking for jobs than there are jobs available, meaning employers can low-ball salaries with the comfort that if you don't take the job, there are 100+ other applicants who would kill for your role (at that lower salary level). |

|

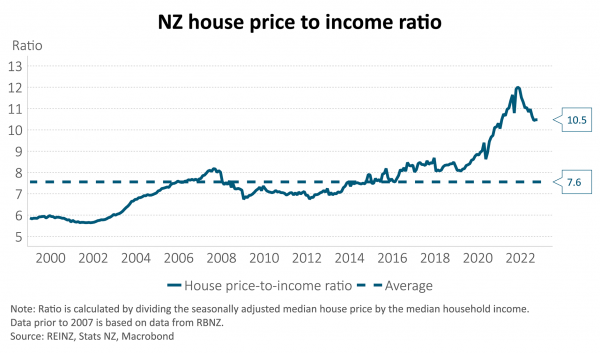

Skyrocketing house prices (relative to incomes)Compared to when parents of young New Zealanders purchased their first homes, the relative house price to income ratio has almost doubled since 2000 (and the comparison is likely worse if your parents purchased their homes in the 80s or 90s).

There are likely two reasons why the NZ house price-to-income ratio has blown out so much:

Exhibit: NZ House Price to Income Ratio since 1999 (source: Harbour Asset Management)

|

|

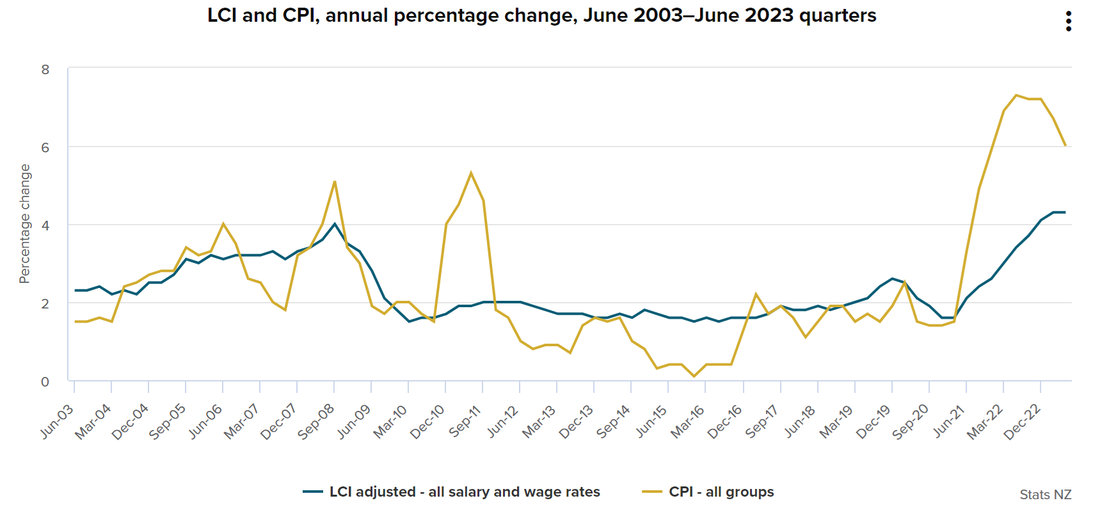

High cost of livingInflation has been hammering New Zealanders post-COVID (particularly those in megacities like Auckland and Wellington). New Zealanders have a few options to battle rising inflation:

Additionally, while COVID had the benefit of normalising the ability to work remotely, many young graduates are now forced to come into the office. Because these graduates are also very early on in their careers, they may not have the negotiating power or "pull" they need to ask for fully remote work. As such, many young graduates that start in the workplace must relocate, often to high-cost-of-living cities like Auckland or Wellington, which can put significant pressure on their ability to save.

Exhibit: Wage growth relative to inflation, suggesting near-zero real wage growth (Source: Stats NZ)

|

|

More stringent banking regulations lead to higher stress testsCompared to the near-zero interest rate in the 2020 and 2021 COVID era, many banks in New Zealand started to raise the bar on the quality and amount of lending they were comfortable with as interest rates started to rise. Additionally, with the Reserve Bank of New Zealand noting the potential financial risks associated with higher interest rates, they moved to implement a Debt to Income framework that financial institutions in New Zealand must comply with.

All of the above leads to the conclusion that financing home purchases has become significantly more difficult, especially for young New Zealanders (who may have lower deposits and a shorter working/earnings history). |

|

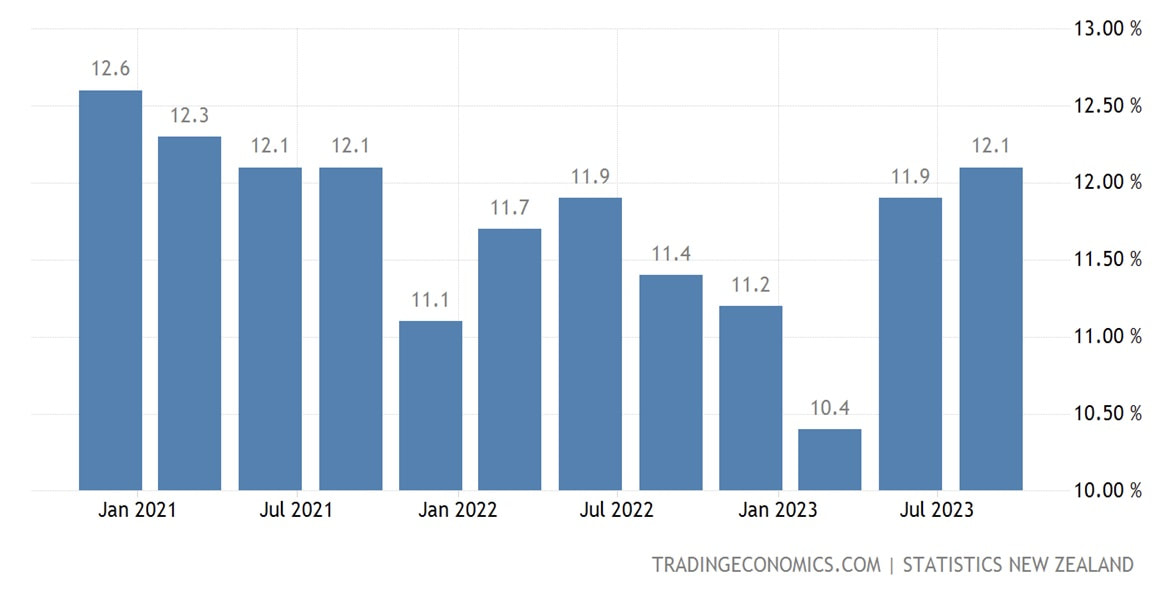

The risk of not being able to find a job post-graduationWhile it can be an easy decision to go to university and get a degree, there's a chance that you won't be able to secure a job post-graduation. If this is the case, your ability to save for a deposit is severely haemorrhaged. Often, it's not up to you either, as many New Zealanders who graduated into the Great Financial Crisis (GFC) in 2008 / 2009 also experienced.

With youth unemployment rates sitting above 10%, there are a substantial number of young New Zealanders who aren't able to make headway on saving for a deposit.

Exhibit: Youth Unemployment Rate as of December 2023 (Source: Stats NZ and Trading Economics)

|

|

Naturally, there is higher discretionary spending on experiences and travelYou’re only young and in your 20s once. Many Gen Z New Zealanders who’ve spent their prime years at uni or in the first few years of the working world locked down at home have the burning desire to go out and see the world, whether that’s the gap year they never took, the South East Asia trip with their mates they couldn’t take or the working holiday to Europe to go to music festivals.

Whatever the experience, young New Zealanders are more likely to spend their youth travelling and having fun - and this comes with its high costs (at a time when they may not have much savings or cash sitting around). |

|

Young New Zealanders may not be in a relationship (and would need to apply for a mortgage as a single-income household)Young New Zealanders are at a time in their lives where they're still figuring out who they are, what they want, where they want to live and who share the core values they want to spend their lives with.

Many young New Zealanders who've spent time travelling or prioritising personal development may not have yet found a life partner they're ready to commit to (and are willing to get into a binding mortgage agreement with). It's not recommended to jump into buying a property with a partner you've known for less than a few years and might be unsure about the long-term. However, the facts are clear as day - if you're applying for a mortgage, you're in a far stronger position applying as a couple than a single person. Assuming both New Zealanders are working, you've likely got double the income to service the mortgage (so you can take out a larger mortgage), and you'll likely be able to share costs (e.g. sharing a room). |

|

Young New Zealanders often face the challenge of limited financial literacy and understand investment opportunitiesMany young adults enter the workforce without a comprehensive understanding of personal finance, investment strategies, and mortgage and real estate nuances. While the government plans to address this, there is a general lack of knowledge. This holds people back - young and old alike.

MoneyHub aims to make investing information available to everyone, but we are realistic and know that many don't and won't get the chance to learn and take action. This means it's harder to save and get ahead and more problematic to get into a house. |

Saving For a House Deposit - Money, Choices, Sacrifices and Reality

Generally, to get the best mortgage rates possible, it's recommended to target 20% of the purchase price as a deposit. However, a 20% deposit is a significant ask for many young New Zealanders (who don't have a few hundred thousand lying around). As such, many programmes require much lower deposits (such as the Kainga Ora first home loan programme, which only requires a 5% deposit down). Alternatively, banks will have a low deposit scheme (which normally drops the deposit requirement to 5 - 10%).

Many of the above programmes and incentives will have stringent eligibility criteria (such as income caps, specific geographies you can buy in, the types of property and minimum sizes, etc.) Additionally, many banks only allow a certain percentage of their loan book towards low-deposit (low equity) mortgages. As such, eligibility for a bank's low deposit programmes may vary depending on how much of that lending they've already done. Our guide to low-deposit loans has more details.

Many of the above programmes and incentives will have stringent eligibility criteria (such as income caps, specific geographies you can buy in, the types of property and minimum sizes, etc.) Additionally, many banks only allow a certain percentage of their loan book towards low-deposit (low equity) mortgages. As such, eligibility for a bank's low deposit programmes may vary depending on how much of that lending they've already done. Our guide to low-deposit loans has more details.

How can I increase my savings and save enough for a deposit?

With inflation putting significant pressure on Young New Zealander's finances, saving up enough for a deposit has never been harder. However, there are a few things that crafty young New Zealanders can do that older New Zealanders may not be able to take advantage of:

1. Automate your savings

2. Position your savings in higher risk/reward investments

3. Watch your expenses through budgeting and expense management.

1. Automate your savings

- Set up automatic transfers to a savings account specifically for your house deposit. Treat it as a non-negotiable expense. The more seamless you can make putting money aside for your deposit and the easier it is to track your progress against it every month or quarter, the more likely you'll feel motivated to continue saving.

- Many banks (such as ASB or Westpac) have built-in app functionality that helps visually show your milestones when saving for things like a home deposit.

2. Position your savings in higher risk/reward investments

- Young New Zealanders are in a unique position that many others don't in that they have an extremely long time horizon to continue growing and investing their wealth (usually multiple decades). This can mean young New Zealanders will be more able to take on higher risk/reward investments to achieve their financial goals (like saving for a deposit).

- If you're a young New Zealander, ensure you're invested in the RIGHT instruments for your age. For example, investing in a heavily skewed shares or ETF portfolio as a 20-year-old New Zealander probably makes more sense than a 100% cash or term deposit portfolio.

3. Watch your expenses through budgeting and expense management.

- You can't control what you don't measure. Young New Zealanders starting to build their financial habits over time might not be aware of how much money they're spending, especially if they have multiple credit cards and accounts with varying bank providers. Unless you track your finances in a big spreadsheet or through an app(such as Booster Savvy, a budgeting app or on a spreadsheet, it can be really easy to overspend or just have no idea how much you spend weekly or monthly.

How Can I Cut Costs?

As a young professional, saving up for a house deposit can be a challenging but achievable goal. We walk you through the steps and strategies necessary to accumulate a substantial deposit for your first home despite high living costs and rent pressures:

1. Consider strategic living arrangements

2. Make lifestyle adjustments

3. Accept that there will be trade-offs.

Related Guides:

1. Consider strategic living arrangements

- As a young New Zealander professional, unless you live with your parents, a significant portion of your income will likely go towards rent, which can slow down savings for a house deposit.

- While it might be seen as "uncool", consider moving back home with your parents if you have the option. This can significantly reduce living expenses, allowing you to save more. While it might not seem worth the $20,000 - $40,000 a year you would save by not paying rent (given the stigma, anxiety and stress that can arise sometimes when living with parents), the ability to accelerate your timeline to get the minimum deposit amount cannot be understated. Additionally, in many cultures (particularly Asian cultures), it's common to continue to live with parents in their 20s, especially before you've met a partner.

- If moving in with your parents is not feasible, getting flatmates and sharing rent and utility costs can also help greatly reduce expenses. If you're currently living alone or in a studio apartment, you're paying a steep premium for the peace of not having flatmates.

- A key question you’ll need to ask is how important getting on the property ladder is to you - if it’s a big priority for you, it might be worth taking on the additional stress and lack of privacy to get to that minimum deposit amount faster.

- Moving in with your partner can significantly reduce costs if you're in a relationship. However, it's crucial to approach this option cautiously, as relationships come with complexities and risks.

2. Make lifestyle adjustments

- Young New Zealanders are in a unique position where they might not have had the time to accumulate lots of "stuff", meaning they can live a relatively minimalist lifestyle. By adopting a more minimalist lifestyle that includes buying less, reusing what you have, and valuing experiences over material possessions, you're likely to be able to reduce your costs significantly. As New Zealanders age, this minimalistic lifestyle likely gets much harder when considering other factors like kids or pets.

3. Accept that there will be trade-offs.

- You must make sacrifices if you're serious about saving up for a deposit. You might not be able to go on that holiday to Europe or go skiing for two months in Queenstown. All these fun things that young New Zealanders love to do have significant costs attached to them, which will slow down the time to save the minimum deposit (and ultimately extend how long you need to keep saving before you can buy a property).

- It's a fine line to walk, and each young New Zealander must weigh what matters most to them. There's no right answer here. Having an absolute blast on budget-friendly holiday options or local entertainment instead of expensive trips or activities is possible. However, you'll need to think and plan for these or risk overspending actively.

Related Guides:

Is Buying a House Right for You and Your Long-Term Needs? Understanding the Realities of Homeownership

In New Zealand, buying a house is often seen as a universally wise financial and lifestyle choice. However, it doesn't always work out - challenging this assumption and understanding both the benefits and the potential downsides is important to ensure you don't rush into the most important decision of your life.

Evaluating the Financial Implications:

1. Long-term Commitment: Homeownership is typically a long-term commitment. Are you ready to stay in one place for a considerable time? Buying a home comes with add-on costs: legal, moving, furnishing, etc., and when you sell a home, you'll be on the hook for around 3% to 4% of the sale price through real estate agent fees. The costs add up, which can make short-term ownership financially unviable.

2. Understanding Costs Beyond the Mortgage: While focusing on mortgage payments is important, don't overlook other expenses such as rates bills, insurance, maintenance, and unexpected repairs. These can significantly impact your overall financial commitment, especially with insurance increasing and more areas becoming difficult to insure.

3. Opportunity Cost: Money tied up in home equity may earn higher returns if invested elsewhere. Housing isn't a sure bet, and there are other investment opportunities.

4. Mortgage Considerations: Most New Zealanders like locking in a fixed-term mortgage, but other options exist, such as floating rates and offset mortgages. What you decide needs consideration.

Lifestyle Considerations

1. Maintenance and Upkeep: Owning a home means you're responsible for all maintenance and repairs - this can be a significant time and financial commitment.

2. Flexibility vs Stability: Renting offers more flexibility to move and less financial burden regarding maintenance and taxes, but it lacks the stability and sense of ownership of buying a house.

Debunking Homeownership Myths

Making an Informed Decision

Evaluating the Financial Implications:

1. Long-term Commitment: Homeownership is typically a long-term commitment. Are you ready to stay in one place for a considerable time? Buying a home comes with add-on costs: legal, moving, furnishing, etc., and when you sell a home, you'll be on the hook for around 3% to 4% of the sale price through real estate agent fees. The costs add up, which can make short-term ownership financially unviable.

2. Understanding Costs Beyond the Mortgage: While focusing on mortgage payments is important, don't overlook other expenses such as rates bills, insurance, maintenance, and unexpected repairs. These can significantly impact your overall financial commitment, especially with insurance increasing and more areas becoming difficult to insure.

3. Opportunity Cost: Money tied up in home equity may earn higher returns if invested elsewhere. Housing isn't a sure bet, and there are other investment opportunities.

4. Mortgage Considerations: Most New Zealanders like locking in a fixed-term mortgage, but other options exist, such as floating rates and offset mortgages. What you decide needs consideration.

Lifestyle Considerations

1. Maintenance and Upkeep: Owning a home means you're responsible for all maintenance and repairs - this can be a significant time and financial commitment.

2. Flexibility vs Stability: Renting offers more flexibility to move and less financial burden regarding maintenance and taxes, but it lacks the stability and sense of ownership of buying a house.

Debunking Homeownership Myths

- It's important to challenge the common myths surrounding homeownership. Despite what the media says, not every scenario guarantees that buying a house is profitable or the best lifestyle choice. Market conditions fluctuate, and personal circumstances can change, affecting the viability of owning a home.

Making an Informed Decision

- Buying a house is possibly the biggest financial decision you will make. It's essential to approach fully understanding all the financial and lifestyle implications. Remember, what's right for others may not be right for you. There is no rush - consider your long-term plans and make an informed decision that aligns with your personal and financial goals.

Must-Know Facts about Young Professionals Saving for a House Deposit

1. Be persistent and keep at it

2. Know you're not behind. You're exactly where you need to be

- Know upfront that saving for a deposit will be a long and arduous road, especially if you've had limited time in a career or have started with student loans/minimal savings. Maintaining focus and resilience in the face of financial challenges is key. Avoiding comparisons and sticking to a personalised saving plan are essential for success.

2. Know you're not behind. You're exactly where you need to be

- Many young New Zealanders on social media like TikTok, Instagram, Facebook and Snap might think they're falling behind because everyone else their age they know and follow is seemingly doing it all (travelling, moving abroad, buying property, getting engaged, etc).

- Know that the content you see is usually the very small minority (1%) that are either (1) getting into debt to do all of these things, (2) having a gigantic inheritance, or (3) getting bankrolled by the bank of mum and dad.

- Take a breath. While it can be useful to understand what others are doing to see if you're on the right track, comparing yourself to others can do more harm than good (especially since you won't know what goes on in their financial situation behind the "picturesque photos"). People only share the best of their lives, not the tough stuff.

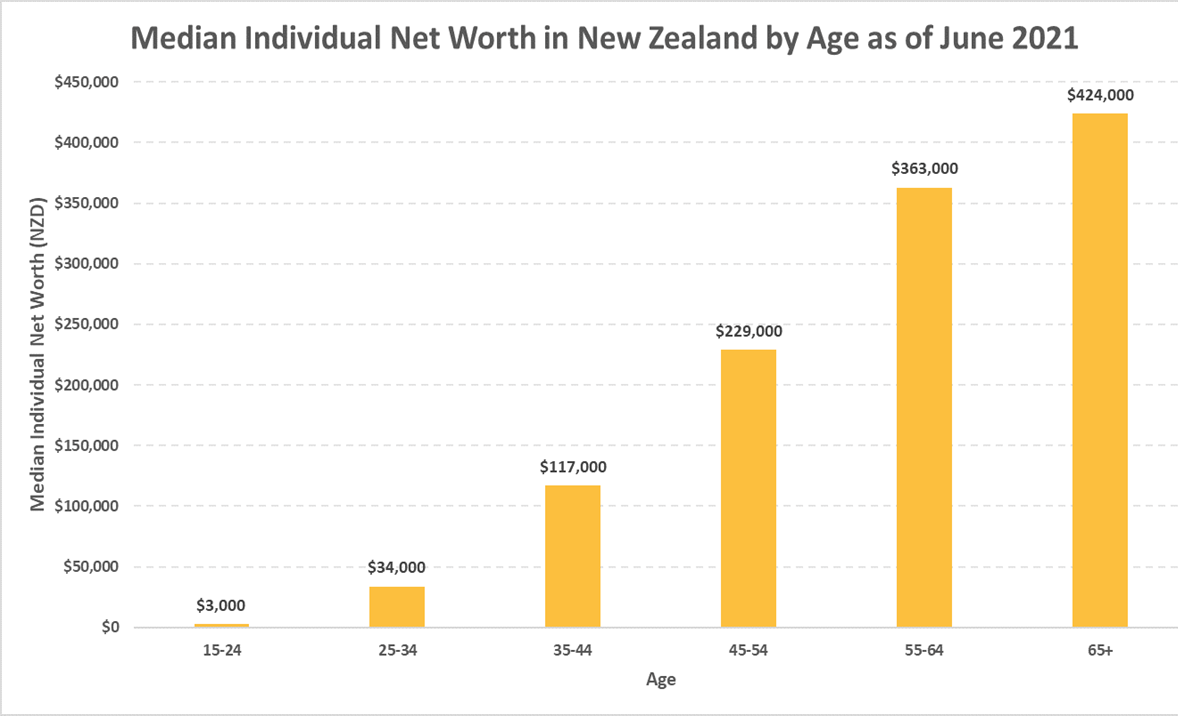

- The data doesn’t lie - our crunched the numbers and guide Average NZ Salaries by Age shows the reality of everyday New Zealand.

Exhibit: 50% of Young New Zealanders (under 35 years of age) Have <$40k Net Worth (Source: Stats NZ)

3. Watch for burnout

4. Job hop often (roughly every two to three years)

5. Watch out for lifestyle inflation

6. Try to balance consumption and savings (you're only young once)

7. Set realistic goals (taking into account your age and situation)

8. Your first home doesn’t have to be your “forever home”

3. Watch for burnout

- Health matters far more than building wealth. While it's great to set ambitious goals and keep yourself motivated, saving for a house deposit is a marathon, not a sprint. Balance is key. Ensure you're not overly sacrificing your current quality of life for your future goals (you are in your 20s, after all).

4. Job hop often (roughly every two to three years)

- Your current employers will often struggle to consistently raise your salaries in line with the market "what you're worth", especially if you joined as a graduate. It can pay to check the going rate for your role every year to ensure you aren't getting underpaid.

- Additionally, your salary doesn't move linearly. The biggest changes in compensation will likely happen when you move jobs. Some New Zealanders see +50% to +100% changes in salary when jumping from one company to another (some of this is down to promotion or changing roles, while other times your current employer is undervaluing you).

- While this is general advice, there may be situations where you're getting paid heaps more than your experience and comparable roles, you love your team culture, and you're constantly learning every day (even after many years). However, this is extremely unlikely.

- It's far more likely that your wage growth will not have doubled in the two or three years you've worked there, your learning curve has plateaued, and you're doing the same things you've been doing before (limiting your learning) and similar things.

5. Watch out for lifestyle inflation

- Young New Zealanders who attended university or trade school probably learned to live like a student. However, once these New Zealanders get into full-time jobs with significant cash flow each month, it can be easy to splurge on nice things while you've got the cash.

- Try to watch that your costs and lifestyle don't change too much as you get further along in your career - lifestyle inflation is silent but financially ruining.

6. Try to balance consumption and savings (you're only young once)

- While it's great to set ambitious goals and try and get onto the property ladder early, you're only young once. There are some experiences that you might want to have that you can't take later (when you've got more obligations or responsibilities). If you want to leverage Working Holiday Visas, realistically, you have to take these before you turn 30. Try to balance having fun when you're young and saving and investing in your future.

7. Set realistic goals (taking into account your age and situation)

- While it's great to try and set a target of saving $1 million by age 30, it may be wildly unachievable and impractical given how many years you need to save for (and how much you can save). Setting achievable savings targets based on personal financial situations and adjusting them as necessary is essential.

- For young New Zealanders, setting a $10k or $20k savings target is a much more reasonable goal than trying to save a huge amount right out of the gate.

8. Your first home doesn’t have to be your “forever home”

- Be open to considering other types of properties. The type and location of the property you aim to purchase can greatly affect the required deposit. Opting for less expensive properties or considering different areas can lower the deposit threshold. This might involve looking at smaller homes, townhouses, or properties in less popular cities or suburbs.

Frequently Asked Questions from Young Professionals Saving for a House Deposit

How Long Does It Take to Save for a House Deposit?

The time required to save for a house deposit varies widely based on income, savings rate, existing savings, and eligibility for lower deposit options. On average, most New Zealanders take five to ten years of serious, focused saving.

Should I Use a Mortgage Broker?

It’s well known that going through mortgage brokers can shave a reasonable amount off your mortgage (anywhere from 10 - 50 basis points - or 0.1% to 0.5%) due to their ability to negotiate on your behalf and potentially get special rates that are below market or standard carded rates. Our guide to mortgage brokers explains more.

How Does KiwiSaver Help with a House Deposit?

KIwiSaver can significantly aid in accumulating a house deposit. After three years of membership, you can withdraw your and your employer's contributions and government contributions for your deposit. Additionally, eligible first-time buyers might receive a Kainga Ora First Home grant, further aiding the purchase. Finally, anyone who contributes the minimum amount each year will receive the government credit, which can be used towards a house deposit.

Why would young New Zealanders want to buy a house right now?

Aside from the cultural norm and "rite of passage" that New Zealanders have to own their property, there are four key reasons why young New Zealanders have their sights on home ownership:

- Not pay rent.

- Build equity (forced savings via mortgage).

- Life milestone (e.g. owning the home to raise kids in).

- Not having to move around every year (which can be seen as a pain, especially with dependants).