Average NZ Salaries by Age 2023 - Where Do You Stand?

Discover where you stand financially with our guide to average NZ salaries and net worth by age. While various factors can influence earnings and net worth, understanding where you stand can help you set goals and make informed financial decisions.

Updated 24 December 2023

Summary:

Our guide covers:

Disclosure:

Related Guides:

- Comparison is the thief of joy. However, many Kiwis are occasionally keen to find out how they stack up financially against other New Zealanders.

- Finding the relevant data to benchmark variables like income and net worth by age can be difficult, causing confusion and uncertainty.

- Additionally, your earning potential and net worth can be influenced by various factors, including your education, skills, work experience, and the industry in which you work.

- For these reasons, it's arguable (to a certain degree) that understanding what you should earn and your net worth at each stage of life can help you set goals and make informed financial decisions.

- To increase your income and net worth, consider investing in your education and skills, negotiating your salary, pursuing promotions and new opportunities, starting a side hustle, and seeking out high-paying industries.

- Ways to increase your net worth include paying off debt, saving and investing, increasing your income, spending wisely, and buying assets that appreciate.

Our guide covers:

- How Much 'Should' I be Earning at Each Stage of Life or Age? (Holistically)

- How Much Should I be Earning at Each Stage of Life or Age? (per Statistics NZ)

- How Does the Wealth of New Zealanders Compare with Wealth from Other Countries?

- Tips to Increase Income, Earnings Power and Net Worth

- Resources Covering Personal Finance and Helping to Growing Income and Net Worth

- Earnings and Net Worth Must-Know Facts

- Frequently Asked Questions

Disclosure:

- The main source we’ve used to draw down on and populate this guide has come from Statistics New Zealand (Stats NZ). Where possible, we've tried to include as much unbiased data as possible.

- However, some of the data points below may be made through a survey or anecdotal format rather than hard, granular data. While our focus is always on quantifiable data, this research needs to rely on such sources, given the nature of the topics.

- Additionally, we’ve focused on median figures, rather than average figures (despite titling the study 'Average NZ Salary'), as median statistics are more representative of the “typical” New Zealander. By doing so, we eliminate the risk of excessive incomes and net worths that skew the data and believe we have a more accurate 'average'.

Related Guides:

Know This First: What is Net Worth? How Do I Calculate Net Worth?

Net worth is a measure of your financial health. It's calculated by subtracting your liabilities (debts and other financial obligations) from your assets (property, investments, and other valuable possessions). A positive net worth indicates that you have more assets than liabilities, while a negative net worth indicates more liabilities than assets.

To calculate your net worth, you'll need to add up the value of all your assets and subtract any outstanding debts or other liabilities. For example, if you own a house worth $500,000 and have a mortgage of $300,000, your net worth would be $200,000 ($500,000 - $300,000).

If you're looking for an easy way to work out your net worth, our net worth calculator will crunch the numbers and work this out for you in minutes.

To calculate your net worth, you'll need to add up the value of all your assets and subtract any outstanding debts or other liabilities. For example, if you own a house worth $500,000 and have a mortgage of $300,000, your net worth would be $200,000 ($500,000 - $300,000).

If you're looking for an easy way to work out your net worth, our net worth calculator will crunch the numbers and work this out for you in minutes.

How Much 'Should' I be Earning at Each Stage of Life or Age? (Holistically)

It's difficult to determine a specific amount you should earn at each stage of life, as this can vary based on your job, education, skills, experience, and industry.

We've focused on medians - for example, if you're a lawyer, accountant or in a medical field, the salaries below will be lower than you and your professional peers. However, this guide focuses on age, not profession, and offers some general guidelines that can help you understand what you should be earning based on your age and career level in New Zealand:

Know This: The above data range is anecdotal evidence to help describe the relative levels and stage Kiwis might be at; we describe hard data below. The numbers above are just general guidelines, and your earning potential may be higher or lower depending on your circumstances.

We've focused on medians - for example, if you're a lawyer, accountant or in a medical field, the salaries below will be lower than you and your professional peers. However, this guide focuses on age, not profession, and offers some general guidelines that can help you understand what you should be earning based on your age and career level in New Zealand:

- Age 15 - 19 (teenagers): Most teenagers with assets at this stage will have been generated through gifts or small odd jobs. Salaries in this age range will likely be <$20,000 per year. For example, working ten hours a week during school and some 40+ hour weeks during summer could earn around $15,000.

- Age 20 - 24: You'll usually either be finishing up university or have just become qualified as a tradesperson. You will likely take an entry-level position at a private company or public organisation. Generally, private companies pay more than public organisations (as many private roles come with short-term incentive plans, bonuses or employee share plans). As an example, entry-level positions in New Zealand typically pay around $40,000 to $50,000 per year.

- Age 25 - 34: As you gain more experience and skills, you’ll likely be able to negotiate higher pay and move between firms or competitors. Salaries in this age range can range from $50,000 to $80,000 per year.

- Age 35 - 44: As you reach your mid-career, you'll likely become extremely proficient or experienced in certain aspects of your role. Additionally, you'll likely take on additional organisational responsibilities, such as leadership, strategy and supporting the younger graduates. All this responsibility means you'll likely be far more valuable in the market and can command a higher salary. The average salary in this age range is from $80,000 to $100,000 per year.

- Age 45 - 54: Many people in this age range are at the peak of their careers and will be earning the highest salary compared to all other age brackets. By this point in your career, you should have had the opportunity to accumulate a significant amount of assets, and your net worth will likely reflect this. Kiwis in this age bracket will likely earn salaries in the $100,000 to $150,000 per year range.

- Age 55+: While salaries may start to decrease slightly as you approach retirement, many people in this age range still earn significant salaries, with the average salary ranging from $80,000 to $100,000 per year.

Know This: The above data range is anecdotal evidence to help describe the relative levels and stage Kiwis might be at; we describe hard data below. The numbers above are just general guidelines, and your earning potential may be higher or lower depending on your circumstances.

How Much Should I be Earning at Each Stage of Life or Age? (per Statistics NZ)

The analysis below has been sourced from Stats NZ. Our research team has undertaken the analysis/calculations and created the graphs:

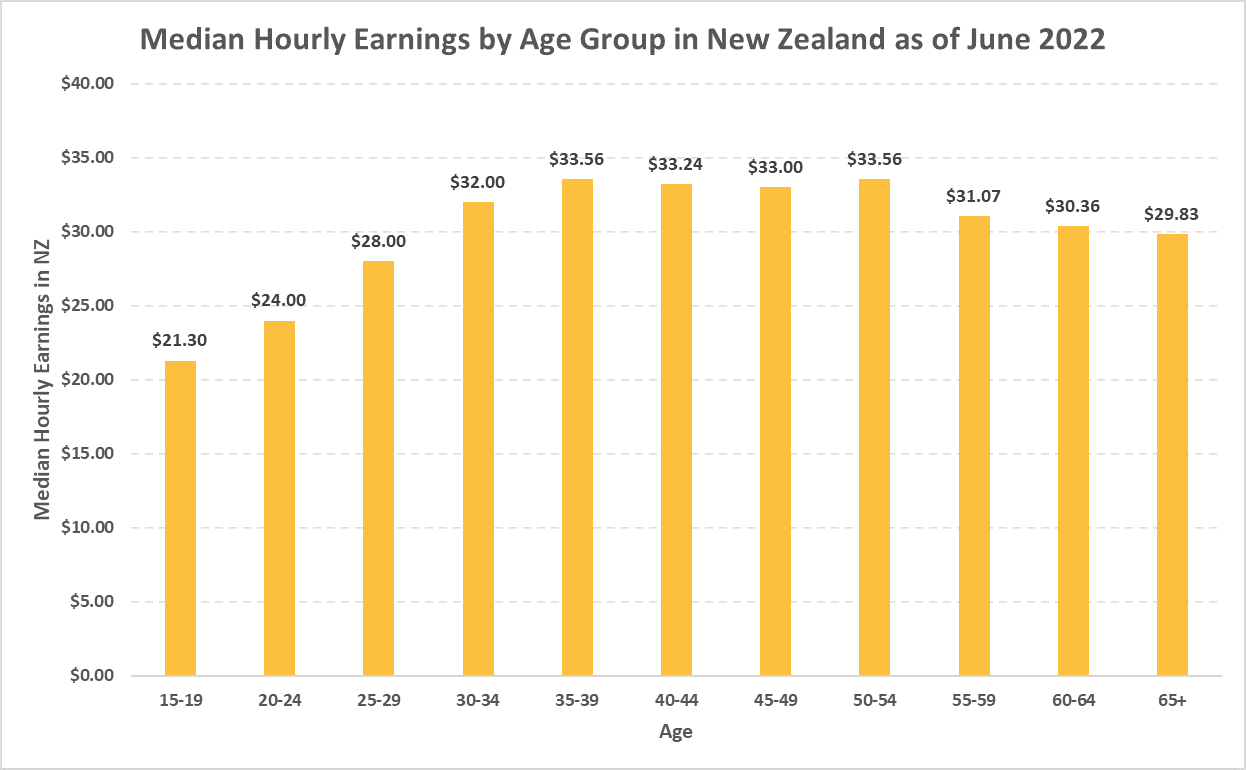

Hourly Earnings in New Zealand

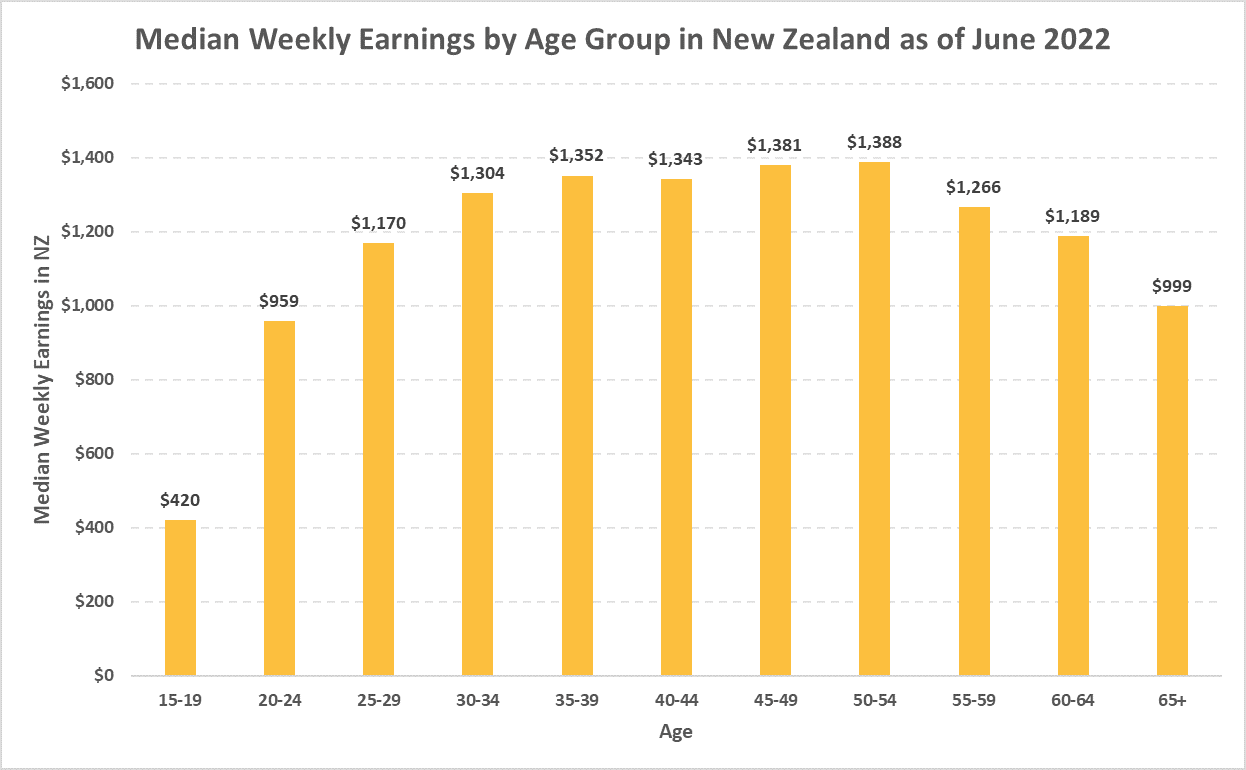

Weekly Income in New Zealand

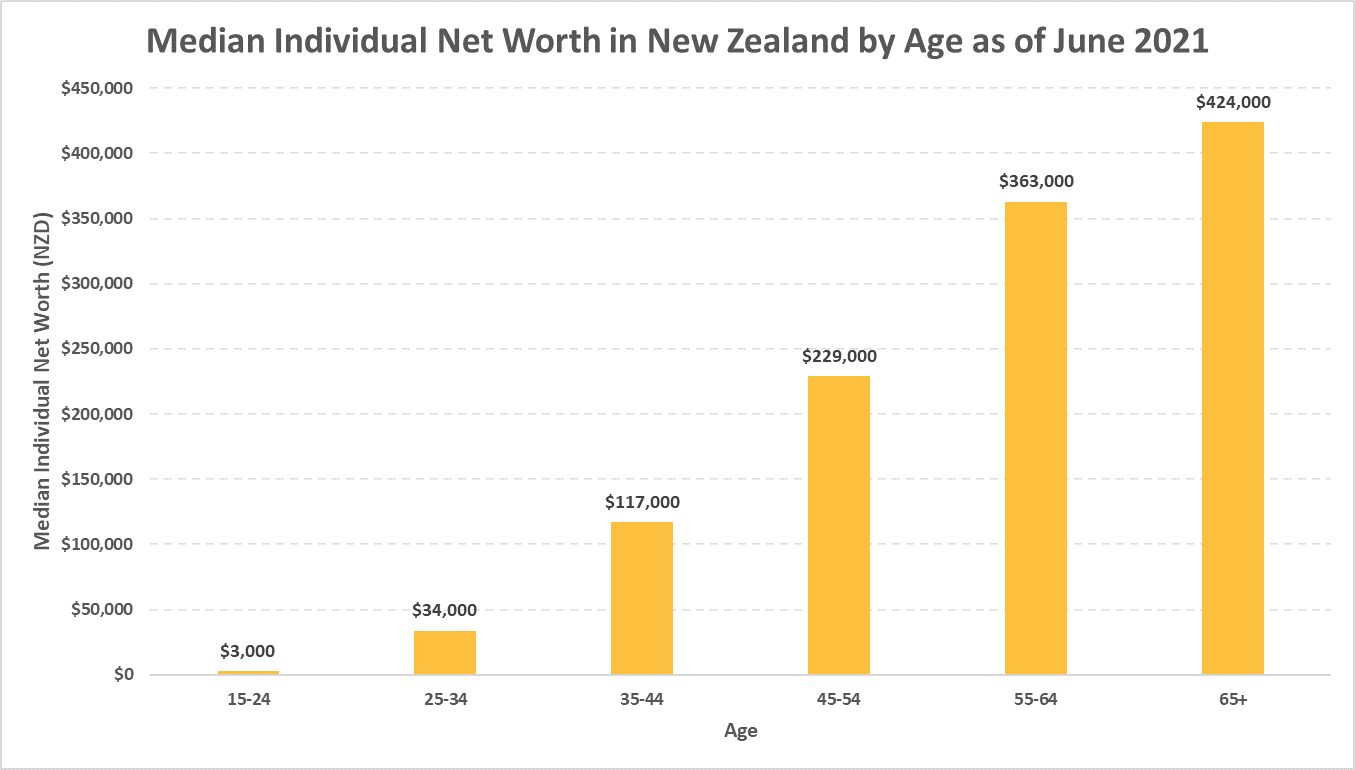

Net Worth (NZD) in New Zealand

Sources: Stats NZ Labour Market Statistics June 2021 and 2022

A few insights can be gained from looking at the tables above - all amounts are presented in New Zealand dollars.

A few insights can be gained from looking at the tables above - all amounts are presented in New Zealand dollars.

Teenagers (15-19)

- As of June 2022, teenagers aged 15 to 19 in New Zealand earned a median hourly rate of $21.30. As of June 2022, teenagers aged 15 to 19 in New Zealand earned a weekly median income of $420.

- These incomes have increased significantly over the past decade, which may be due in part to minimum wage increases.

- From April 1st 2022 the adult minimum wage increased to $21.20 (gross) per hour, increasing again in April 2023.

Kiwis in their 20’s

- Generally, Kiwis in their 20s earn significantly more than their teenage counterparts, likely due to many Kiwis in their 20s graduating from university or finishing up apprenticeships and shifting to full-time work. As of June 2022:

- Kiwis aged 20 to 24 in New Zealand earned a median hourly rate of $24.

- Kiwis aged 20 to 24 in New Zealand earned a weekly median income of $959.

- Kiwis aged 25 to 29 in New Zealand earned a median hourly rate of $28.

- Kiwis aged 25 to 29 in New Zealand earned a weekly median income of $1,170

Net Worth: Kiwis aged 15 to 24 in New Zealand had an individual net worth of $3,000 (as at June 2021).

Kiwis in their 30’s

- Generally, Kiwis in their 30s are getting promoted and moving jobs, industries and countries as they get more experience, leading to higher salaries. As of June 2022:

- Kiwis aged 30 to 34 in New Zealand earned a median hourly rate of $32.

- Kiwis aged 30 to 34 in New Zealand earned a weekly median income of $1,304.

- Kiwis aged 35 to 39 in New Zealand earned a median hourly rate of $33.56.

- Kiwis aged 35 to 39 in New Zealand earned a weekly median income of $1,352.

Net Worth: Kiwis aged 25 to 34 in New Zealand had an individual net worth of $34,000 New Zealand dollars (as at June 2021).

Kiwis in their 40’s

- Generally, Kiwis tend to reach their highest earning potential in their early 40s as they enter leadership positions and have over 20 years of experience in their industry or roles. As of June 2022:

- Kiwis aged 40 to 44 in New Zealand earned a median hourly rate of $33.24.

- Kiwis aged 40 to 44 in New Zealand earned a weekly median income of $1,343

- Kiwis aged 45 to 49 in New Zealand earned a median hourly rate of $33

- Kiwis aged 45 to 49 in New Zealand earned a weekly median income of $1,381

Net Worth: Kiwis aged 35 to 44 in New Zealand had an individual net worth of $117,000 (as at June 2021).

Kiwis in their 50’s

- Generally, when Kiwis hit their 50s, the amount of time they've spent in the workforce may not necessarily translate to higher earnings.

- This earnings gap exists because most careers and industries have an "earnings cap" or "earnings ceiling" that, once you reach, becomes hard to surpass either due to a lack of open positions above you to get promoted to or the nature of the industry is such that they don't pay any more above a certain level. As of June 2022:

- Kiwis aged 50 to 54 in New Zealand earned a median hourly rate of $33.56

- Kiwis aged 50 to 54 in New Zealand earned a weekly median income of $1,388

- Kiwis aged 55 to 59 in New Zealand earned a median hourly rate of $31.07

- Kiwis aged 55 to 59 in New Zealand earned a weekly median income of $1,266

Net Worth: Kiwis aged 45 to 54 in New Zealand had an individual net worth of $229,000 (as at June 2021).

Kiwis in their 60’s

- Pay tends to decrease significantly when people reach their 60s, which may reflect a switch to fewer hours or early retirement. Additionally, Kiwis in their 60s may find it harder to find the roles they're looking for as easily as they did in their 40s or 50s. As of June 2022:

- Kiwis aged 60 to 64 in New Zealand earned a median hourly rate of $30.36

- Kiwis aged 60 to 64 in New Zealand earned a weekly median income of $1,189

Net Worth: Kiwis aged 55 to 64 in New Zealand had an individual net worth of $363,000 (as at June 2021).

Kiwis at the typical retirement age (65 onwards)

As of June 2022:

Net Worth: As of June 2021, Kiwis aged 65 onwards in New Zealand had an individual net worth of $424,000 (as at June 2021).

- Kiwis aged 65 onwards in New Zealand earned a median hourly rate of $29.83

- Kiwis aged 65 onwards in New Zealand earned a weekly median income of $999

Net Worth: As of June 2021, Kiwis aged 65 onwards in New Zealand had an individual net worth of $424,000 (as at June 2021).

How Does the Wealth of New Zealanders Compare with Wealth from Other Countries?

According to data from Credit Suisse Wealth Databook 2022:

Increases in Wealth in New Zealand.

- New Zealanders saw the fastest increase in mean wealth per adult globally between 2020 and 2021. The country's mean wealth per adult increased by US$114,290 (NZD 202,000) to US$472,150, and the median rose to US$231,260, an NZD 57,920.

- The data shows that rising house prices and a strong currency contributed to this increase in wealth for New Zealanders. For example, if you own a house in an Auckland suburb close to the CBD without a mortgage, you could be among the top 1% wealthiest people in the world. If not, you're likely among the top 10% wealthiest people globally.

The number of millionaires in New Zealand.

- In 2021, there were 347,000 millionaires in New Zealand (in US dollars), an increase of 113,000 from the previous year.

- Globally, there were 62.5 million millionaires. New Zealand's growth in millionaires was among the top 10 biggest increases in the world.

- New Zealand has 2.126 million people in the top 10% of wealthy individuals globally and 281,000 in the top 1%. Globally, the top 1% now have 45.6% of the world's wealth, up from 43.9% in 2019.

- To be in the top 10% of wealthiest people in the world, you need to have a net wealth of US$138,346. For the top 1%, the bar is US$1.147 million.

Tips to Increase Income, Earnings Power and Net Worth:

There are several strategies you can use to increase your income:

There are strategies you can use to increase your net worth:

- Education and training: Investing in your education and career development can open up opportunities for higher-paying jobs. Pursue additional certifications, degrees, or training in your field, or consider switching to a field with higher earning potential.

- Add more value: Look for ways to add value to your current employer. For example, offer new ideas, take on additional responsibilities and strive for excellence in your performance. Your employer might see your contribution's value and consider a promotion or raise.

- Networking: Building professional relationships can help you stay informed about job opportunities and can lead to mentoring, career advancement or accelerated promotion.

- Negotiate your salary: Don't be afraid to ask for a raise at your current job or to negotiate your salary when you're offered a new job. But, again, it's important to research and understand what you're worth in the market to negotiate a fair salary.

- Seek out high-paying industries: Some industries tend to pay higher salaries than others. If you want to increase your income, consider exploring careers in technology, finance, and healthcare.

- Look for new job opportunities: Look for new job opportunities on the internet and consider both full-time and part-time jobs. You can use job search websites, recruitment agencies, and your professional networks to search for job openings.

- Start your own business: Consider starting your business as a side hustle or a full-time venture. Starting your own business can be a great way to increase your income, but it does come with more risk and uncertainty. Additionally, as an alternative to full-time employment, freelancing or contracting can provide more flexibility and possibly higher earning potential. It also provides a way to test the waters in a new field or industry.

There are strategies you can use to increase your net worth:

- Increase your income: As mentioned above, increasing your income will almost always help you grow your net worth (assuming lifestyle inflation doesn’t occur).

- Live below your means: One of the most effective ways to increase your net worth is to spend less than you earn. By living below your means, you'll be able to generate more disposable money to save and invest. So review your expenses and look for areas where you can cut back, such as subscription services or dining out.

- Create a budget: Create a budget and track your expenses. Tracking expenses will help you identify areas where you can reduce spending and increase your savings.

- Pay off debt: High-interest debt, such as credit card debt, can eat away your net worth. Make paying off debt a priority and avoid taking on new debt as much as possible.

- Invest: Investing your money is one of the most effective ways to grow your net worth. Consider investing in a diverse range of assets such as stocks, bonds, mutual funds, or real estate.

- Start saving early: The earlier you start saving, the more time your money has to grow. Take advantage of compound interest and take advantage of savings plans.

- Be mindful of tax: Consider the tax implications of your investments and financial decisions. Then, take advantage of any tax breaks or incentives available.

- Be patient and consistent: Building wealth takes time and consistency. Stay committed to your financial goals, and don't get discouraged if you don't see immediate results. Keep in mind that slow and steady progress is still progress.

- Educate yourself: Learn about personal finance and investing as much as possible. Read books, take courses, and seek advice from financial experts. The more you know, the better equipped you will be to make informed decisions about your money. Keep learning and growing. Learning and growing are the keys to financial success. As you learn more, you'll be better equipped to make wise decisions about your money and more likely to achieve your financial goals.

- Be realistic: Try to be realistic about your financial goals, and don't try to keep up with the Joneses. It's important to be content with what you have and not compare yourself to others. Setting realistic financial goals that align with your lifestyle and income will help you create a sustainable plan for achieving them.

- Avoid lifestyle inflation: As you earn more, avoid the trap of lifestyle inflation. Instead of upgrading your lifestyle to match your increased income, continue to live frugally and use the extra money to pay off debt and save for the future.

- Review and re-evaluate your plan: Review and re-evaluate your plan regularly. Reflect on how well you're doing, what changes you need to make, and what you can do better.

- Be diversified: Be diversified in your investments and savings. Diversification reduces risk and increases the chances of getting better investment returns.

Resources Covering Personal Finance and Helping to Growing Income and Net Worth

There are many resources (both global and New Zealand-centric) available to help you learn more about growing your income and net worth. Here are a few suggestions:

MoneyHub (Financial Independence series)

- We have a dedicated section on becoming more financially independent and potentially retiring earlier than the traditional retirement age of 65.

- Our comprehensive guides on boosting income and reducing expenses in the FIRE (Financial Independence Retire Early) series offers easy wins and steps to take to build a strong financial future.

Sorted

- Sorted is a New Zealand government-owned website that provides financial advice and resources to help New Zealanders make the most of their money. The website covers various topics, including budgeting, saving, investing, insurance, and retirement planning.

- One of the key features of the Sorted website is the "Money Planner," which is a tool that helps users create a personalised budget based on their income, expenses, and financial goals. The website also offers a range of financial calculators that can help users determine how much they need to save to reach their goals, such as buying a home or saving for retirement.

- In addition to the financial tools and resources, the Sorted website also offers a range of articles and guides on topics such as debt management, tax planning, and managing your money during economic uncertainty. The website also has a section dedicated to helping young people make the most of their money, with resources and tips for building good financial habits from a young age.

Interest.co.nz

- Interest.co.nz is a news and analysis website focused on personal finance and economic issues in New Zealand.

- The website offers a range of resources and tools, including mortgage calculators, retirement planning tools, and comparisons of different financial products.

- There are several online communities and forums dedicated to personal finance. These communities can be good places to get advice from others who are also working on improving their financial situation.

- The most popular and relevant subreddit for New Zealanders is Personal Finance New Zealand, which has over 60,000 members as of March 2023 and has many great tips and tricks on how Kiwis can increase their income, decrease their expenses and grow their net worth faster.

Earnings and Net Worth Must-Know Facts

1. Most Kiwis will reach peak earnings in their 40’s. Try to take full advantage of this.

Typically, people tend to earn the most in their 40s. In the past, people in their 30s earned virtually the same as those in their 40s. However, the difference between these two age groups has increased, indicating that "peak earnings" tend to occur later in life.

One way to think about it is that your 20s are for learning, while your 30s and 40s are for earning. So this scenario would mean that in your 20s, you choose your field and develop your skills, and then in your 30s and 40s, you focus on extracting the most out of those skills and maximising your earnings.

During your 30s and 40s, you'll likely be able to build wealth the fastest due to your high income and opportunity to leverage up and invest in property (tied to your income affordability). Then, in your 50s and 60s, many people focus on their quality of life and lean into family or relationships rather than work. This pivot means you might ease off and work in a less demanding role or part-time as your goals and ambitions change. However, working less will almost always result in a decrease in weekly earnings.

One way to think about it is that your 20s are for learning, while your 30s and 40s are for earning. So this scenario would mean that in your 20s, you choose your field and develop your skills, and then in your 30s and 40s, you focus on extracting the most out of those skills and maximising your earnings.

During your 30s and 40s, you'll likely be able to build wealth the fastest due to your high income and opportunity to leverage up and invest in property (tied to your income affordability). Then, in your 50s and 60s, many people focus on their quality of life and lean into family or relationships rather than work. This pivot means you might ease off and work in a less demanding role or part-time as your goals and ambitions change. However, working less will almost always result in a decrease in weekly earnings.

2. Don't be disheartened if you're below your age bracket's income and net worth benchmarks.

It's important to know that the numbers and statistics presented in this guide are median figures ONLY. Additionally, there's a significant amount of variability, bias and caveats when breaking down survey data or looking at one specific period.

Just because you're above or below some of the numbers in this guide doesn't mean you're on the wrong track. However, suppose you feel you're not earning as much as you would like or are considering switching careers. In that case, it may be helpful to consider industries currently hiring and offering higher salaries. For a deeper dive into this, check out our definitive guide on how to get promoted at work.

Just because you're above or below some of the numbers in this guide doesn't mean you're on the wrong track. However, suppose you feel you're not earning as much as you would like or are considering switching careers. In that case, it may be helpful to consider industries currently hiring and offering higher salaries. For a deeper dive into this, check out our definitive guide on how to get promoted at work.

3. Choosing the right industry can disproportionately impact your income and net worth.

According to data from Seek, the top three industries with the most significant increases in pay (for specific roles) are the Information and Communication Technology, Manufacturing Transport and Logistics, and Hospitality and Tourism industries.

Generally, picking an average role in a high-growth industry (such as software engineering) will lead to far higher income and net worth than picking a high-growth role in a slow-growth industry. However, if you have the ability or freedom, try to choose industries that align with your skill sets and interests and are also in a high-paying industry.

Generally, picking an average role in a high-growth industry (such as software engineering) will lead to far higher income and net worth than picking a high-growth role in a slow-growth industry. However, if you have the ability or freedom, try to choose industries that align with your skill sets and interests and are also in a high-paying industry.

4. Compare yourself to you yesterday, not to other Kiwis today.

While it can be useful to understand what other Kiwis in similar situations are earning (to ensure you're not getting underpaid), every person will be in a unique financial situation. If comparisons to others are only causing you anxiety and stress, try to focus on comparing yourself to yourself from a few years ago rather than others.

We're all on vastly different journeys, and up to a certain point, it doesn't make sense to compare yourself to other New Zealanders continually.

Try not to get too caught up in comparing yourself to others, and instead, remember that these are just averages and that focusing on your goals and progress will yield more results than constant comparisons.

We're all on vastly different journeys, and up to a certain point, it doesn't make sense to compare yourself to other New Zealanders continually.

Try not to get too caught up in comparing yourself to others, and instead, remember that these are just averages and that focusing on your goals and progress will yield more results than constant comparisons.

Frequently Asked Questions

When do New Zealanders usually reach a positive net worth?

It's difficult to determine a specific age at which New Zealanders reach a positive net worth as this differs heavily based on various factors, including education, skills, work experience, and industry. However, it's common for people to reach a positive net worth in their mid-to late-20s or early 30s as they enter the workforce and accumulate assets.

How long does it usually take New Zealanders to earn more than $100,000 in New Zealand?

It's difficult to determine a specific length of time it takes New Zealanders to earn more than $100,000, as this can vary based on education, skills, work experience, and the industry you work in. However, it's common for people to reach this income level in their mid-to late-30s or early 40s as they gain more experience and skills and progress in their careers.

Where can I find data on what Kiwis are earning? What about data related to Net Worth?

You can find the best data on earnings and net worth statistics in New Zealand from these three government organisations:

Where can I find data on the net worth of other people my age overseas?

The website Financial Samurai has relevant sources about net worth in the United States, for example it has articles about net worth figures of 30-year-olds and above-average people.

Related Guides and Tools:

- PAYE Income Tax Calculator

- Minimum Wage

- Net Worth Calculator

- When Will I Have $1m Calculator

- What to Study

- Apprenticeships

- Average KiwiSaver Balance By Age

- 20 Things to Stop Buying to Have More Money

- 20 Indicators You're Doing Well Financially

- 20 Must-Know Money Lessons (Learned From Experience)

- 20 Money Habits that Keep You Poor