How to choose a KiwiSaver fund

Our guide helps to answer the age-old question of "what KiwiSaver fund should I be in?" We look at fund types, fees, performance and explain why default funds may not be suitable for your needs

Updated 3 August 2023

If you’re already a KiwiSaver member and looking to switch, or thinking about joining, this guide walks you through what’s important when making your decision. The good news is KiwiSaver isn’t complicated, and there are plenty of trusted funds to choose from. Our guide walks you through what's important to help you make the right choice.

Know this first:

To walk you through what you should consider, our guide covers:

If you’re already a KiwiSaver member and looking to switch, or thinking about joining, this guide walks you through what’s important when making your decision. The good news is KiwiSaver isn’t complicated, and there are plenty of trusted funds to choose from. Our guide walks you through what's important to help you make the right choice.

Know this first:

- Our research team believes that the majority of New Zealanders are not currently saving enough to fund a comfortable retirement.

- Right now, based on IRD data, 1 in 3 KiwiSaver members are non-contributing. While this will include a number of people over the age of 65 who are no longer contributing, the statistics are frightening. A lack of retirement money is very much going to be a significant national problem in the not too distant future as our retirement guide explains.

- KiwiSaver isn't complicated, and there's only upside. The process is simple – pick the right fund, contribute the right amount of money, take a long-term view and, if you do all that, you'll have the highest chances of reaching a comfortable retirement.

- But, if you're in the wrong fund for an extended period, it costs you real money every day as your savings will grow at a lesser rate. By the time you get to 65, it’s too late to try and save more - you'll have to live on what you've already saved in addition to your government superannuation payments.

- Once you've chosen what you consider to be the "right" KiwiSaver fund for your needs, you can contribute fully aware that your contributions are going where they should be.

- We believe the "right" KiwiSaver fund depends on your life stage; for example, saving for a first home or powering up a retirement nest egg.

To walk you through what you should consider, our guide covers:

Starting Point: Knowing what you want from KiwiSaver is the BEST way to choose a fund

Know this first: There are a LOT of KiwiSaver funds. Rather than go into painstaking detail comparing fees, past-performance and risk, we think there's a better way:

First, ask yourself what you want from KiwiSaver - the five scenarios describe the majority of New Zealanders:

Second, once you know your plans, you will need to choose a fund type that is designed to deliver what you need. No matter where you are in your life, most KiwiSaver schemes will make you choose a fund 'type' - i.e. growth, balanced or conservative etc. This may be limiting, but it's the most popular approach to KiwiSaver investing.

Now that I need to choose a fund, what fund type is right for me?

Once you know what fund type you're looking for, you can start comparing funds based on their performance and fees, as we outline next.

First, ask yourself what you want from KiwiSaver - the five scenarios describe the majority of New Zealanders:

- Are you young, starting your first full-time job and hoping to buy your first home in 5-10 years (or less) using your KiwiSaver?

- Are you a couple of years away from homeownership and want to use your KiwiSaver fund to help with the deposit?

- Are you in your 30s or 40s and looking to save as much money as possible for your retirement?

- Are you in your late 50s and want to protect your KiwiSaver balance with a low-risk investment so you don’t lose money before you retire?

- Are you retired and looking to keep your KiwiSaver balance safe while you spend it?

Second, once you know your plans, you will need to choose a fund type that is designed to deliver what you need. No matter where you are in your life, most KiwiSaver schemes will make you choose a fund 'type' - i.e. growth, balanced or conservative etc. This may be limiting, but it's the most popular approach to KiwiSaver investing.

Now that I need to choose a fund, what fund type is right for me?

- Guidance from Sorted suggests that if you don't plan to access your KiwiSaver balance for ten years or more and are comfortable with seeing ups and downs in your balance each year, a growth fund is the most appropriate.

- For the five scenarios listed above you can do Sorted's test here to make sure you chose the right fund ‘type'. It's worth triple-checking your answers to make sure you are 100% certain.

Once you know what fund type you're looking for, you can start comparing funds based on their performance and fees, as we outline next.

What to look for in a KiwiSaver fund

When you compare KiwiSaver funds, what matters is the performance and the fees you’ll pay, and you need to balance that against the risk you’re prepared to take.

Step 1: Understand the Investment options

KiwiSaver funds types invest in different assets; the more growth-focused, the higher the proportion of your money that goes into shares, as you can see here:

Some KiwiSaver schemes, such as koura, Superlife and Lifestages, let you mix KiwiSaver funds to suit your investing profile. This means you are not invested 100% into one fund, but you may have 25% in growth, 50% in balances and 25% in conservative funds.

Step 2: Understand the fees

All KiwiSaver funds charge fees; membership fees and management fees, usually in a dollar amount and a percentage of your investment’s value. Either way, the lower the fees, the better off you’ll be in retirement. Fees are calculated and deducted daily; a low-cost fund will charge around $50 a year on a $10,000 KiwiSaver, whereas a high-fee fund could charge as much as $150, or even more. The fund's fee will be displayed on the KiwiSaver scheme's website. You can also fund it in our KiwiSaver reviews.

Step 1: Understand the Investment options

KiwiSaver funds types invest in different assets; the more growth-focused, the higher the proportion of your money that goes into shares, as you can see here:

- Growth funds (the riskiest, as they invest in shares)

- Balanced funds (mixing share investments with less risky term deposits and cash etc.)

- Conservative (even lower risk, with usually around 80% of the money invested in bank deposits and fixed-interest bonds)

- Cash – (lowest risk, as money is deposited into bank accounts)

- Ethical (these funds are unique and usually invest in a particular niche, such as water, sustainable energy or socially responsible companies).

Some KiwiSaver schemes, such as koura, Superlife and Lifestages, let you mix KiwiSaver funds to suit your investing profile. This means you are not invested 100% into one fund, but you may have 25% in growth, 50% in balances and 25% in conservative funds.

Step 2: Understand the fees

All KiwiSaver funds charge fees; membership fees and management fees, usually in a dollar amount and a percentage of your investment’s value. Either way, the lower the fees, the better off you’ll be in retirement. Fees are calculated and deducted daily; a low-cost fund will charge around $50 a year on a $10,000 KiwiSaver, whereas a high-fee fund could charge as much as $150, or even more. The fund's fee will be displayed on the KiwiSaver scheme's website. You can also fund it in our KiwiSaver reviews.

Step 3: Evaluate the Performance

How to read a Morningstar report?

We consider Morningstar to be the most reliable source of comparative KiwiSaver data, and also the only organisation to provide it in such a user-friendly format. As a background, Morningstar is an investment research firm that compiles and analyses funds and general market data. It’s completely independent.

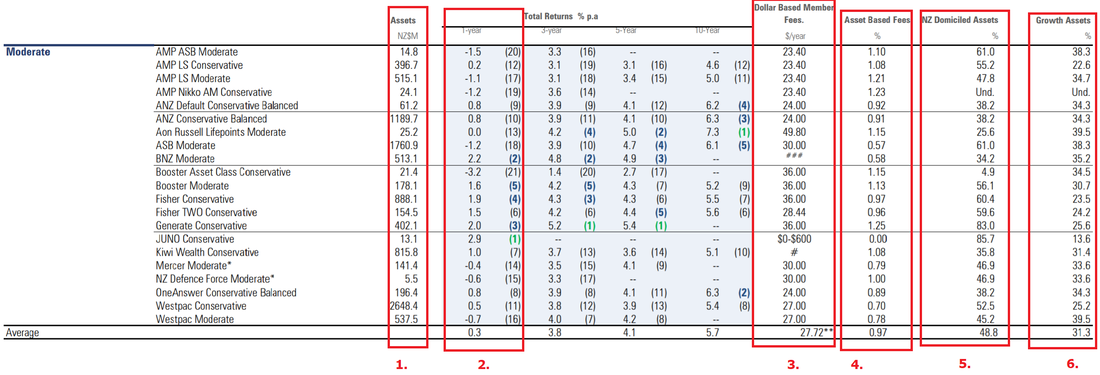

Let’s take an example of 'Moderate' funds for the period ending 31 March 2020:

- You can only compare funds in the same categories; for example, it’s pointless to compare the performance of a growth fund with a conservative fund – they invest in entirely different things.

- To get an idea of the best-performing funds, take a look at the most recent Morningstar data.

How to read a Morningstar report?

We consider Morningstar to be the most reliable source of comparative KiwiSaver data, and also the only organisation to provide it in such a user-friendly format. As a background, Morningstar is an investment research firm that compiles and analyses funds and general market data. It’s completely independent.

Let’s take an example of 'Moderate' funds for the period ending 31 March 2020:

Credit: Morningstar KiwiSaver Reporting. Source: https://cdn.morningstar.com.au/mca/s/documents/KiwiSaver_Survey_Q1_2020.pdf

What the columns mean:

Our video explains how to use Morningstar:

- Assets = total size of the fund. In this example, you can see the Westpac Conservative fund is the largest.

- 1-Year Total Returns = the % return, net of fees, with the performance rank in brackets. In this example, JUNO Conservative was the best performer as it's marked (1). The adjacent columns give 3 year, 5 year and 10 year returns.

- Dollar based member fees = this is the annual membership fee paid by a member of the respective KiwiSaver scheme.

- Asset-Based fees = this is the annual management fee of the fund. In this example, you can see Generate Conservative charged the most (1.25% p.a.)

- NZ Domiciled assets = the percentage of assets the funds holds that are New Zealand based, for example, shares traded on the NZX and local comoany and government bonds.

- Growth assets = the percentage of assets the funds holds that are invested in shares

Our video explains how to use Morningstar:

Tools to Make Comparing KiwiSaver Funds Easy

There is a lot of data available which lets you compare KiwiSaver funds on a number of metrics. Popular and trusted KiwiSaver fund comparison websites include:

Please note: All of the above websites offer information for free and are not affiliated to any KiwiSaver scheme.

Important: We don't suggest selecting a KiwiSaver fund solely because of its most recent performance – past results are no guarantee of future results. To get a better picture of what could be best for you, consult these useful resources:

- Sorted's Smart Investor - an incredibly useful tool which illustrates the fees, returns and investments of every KiwiSaver fund

- MoneyHub’s KiwiSaver scheme reviews – this narrates the basics of each scheme, and discusses the pros and cons of what you can invest in.

- Morningstar - comprehensive quarterly reports which rank the results of each fund.

Please note: All of the above websites offer information for free and are not affiliated to any KiwiSaver scheme.

Important: We don't suggest selecting a KiwiSaver fund solely because of its most recent performance – past results are no guarantee of future results. To get a better picture of what could be best for you, consult these useful resources:

- Our favourite KiwiSaver funds guide can help further decide what’s right for you by challenging you to think about what you need.

- Our KiwiSaver calculator (which links to Sorted's tool) shows you how much KiwiSaver money you will have when you retire, what you plan to spend during your retirement, and whether or not your KiwiSaver money will be enough for what you want to do.

- A KiwiSaver scheme's product disclosure statement (PDS) – each KiwiSaver scheme publishes one; it outlines the investing strategy of each fund, the fees and risks. You can find the PDS published on a KiwiSaver scheme’s website under “documents” or (similar). They are increasingly becoming more user-friendly to read and show each fund side-by-side.

Be Aware: 'Default' funds await those who don't choose a KiwiSaver fund

If you sign up to KiwiSaver but don’t choose a fund, the IRD will pick a fund for you. This is known as a ‘default fund’ and could be one of any default providers here. You don’t have to stay in a default fund. To change to a fund you want simply contact the scheme that managers the fund. For example, if you wanted to join the Fisher Funds Growth fund, you would contact Fisher Funds.

Default funds are, by nature, unlikely to be the best option for your long-term financial needs. Here are some examples of how choosing the right fund makes a big difference:

Default funds are, by nature, unlikely to be the best option for your long-term financial needs. Here are some examples of how choosing the right fund makes a big difference:

Claire chooses lower KiwiSaver fees

- Claire is 35 and earns $80,000 per year working as an accountant. She already has $20,000 in her KiwiSaver fund and was paying 1.00% fees.

- After comparing KiwiSaver funds, she found a fund that offered a similar investment with only 0.50% fees.

- By changing to a fund with lower fees, Claire will have $34,000 more in her KiwiSaver at age 65. Her KiwiSaver account balance will be $419,000 instead of $385,000.

Max chooses a higher-performing KiwiSaver fund

- Max is 30 and earns $60,000 per year working on a farm. He has $10,000 in his KiwiSaver, which is a default fund earning 3.5%.

- After comparing KiwiSaver funds, he finds a growth fund that is focused on making higher returns, and makes the decision to switch. When he reaches 65, his annual after-tax investment return between age 30 to 65 is 4.5%.

- By changing to a fund that is growth-focused (and has lower fees), Max will have $70,000 more in her KiwiSaver at age 65. His KiwiSaver account balance will be $405,000 instead of $335,000.

Important: Expected earnings have been sourced from our KiwiSaver calculator and the Financial Market Authority’s annual after-tax return guidelines - 2.5% (conservative fund), 3.5% (balanced fund) and 4.5% (growth fund). Our calculations include a 2% expected annual pay rise.

Final Thoughts

Important: We don’t think anyone should invest in anything they don’t understand. Before signing up to any KiwiSaver fund, make sure you ask:

Your KiwiSaver is (and will always be) your money. How much you end up with at 65 comes down to how much you contribute and what fund you invest. There are no second chances – making sure you’re in the right KiwiSaver fund is a $100,000+ decision. If you’re in doubt, our favourite KiwiSaver funds guide outlines funds and schemes we like based on different life needs.

- What are the fees, and are they competitive? There are membership fees (around $20-$30 per year) and management fees (anything from 0.31% of your balance to more than 1.50%). High fees don’t mean high returns, and vice versa. Small differences in fees can add up significantly over time which completely changes your retirement money.

- What is the performance of the fund in the last 1-3 years? Past performance is no guarantee of future results, but it does give you an idea of how profitable the fund is compared to its rivals. For example, if you want to invest in a growth fund, Fund 1 reporting a 3-year return of 7% is better than Fund 2 reporting 4.50%. These differences, over time, add up to a lot by the time you reach retirement.

Your KiwiSaver is (and will always be) your money. How much you end up with at 65 comes down to how much you contribute and what fund you invest. There are no second chances – making sure you’re in the right KiwiSaver fund is a $100,000+ decision. If you’re in doubt, our favourite KiwiSaver funds guide outlines funds and schemes we like based on different life needs.