Tax on Investments and Savings in a Nutshell

Our definitive guide explains tax in a simple way for KiwiSaver members, investors, savers and property owners to make better financial decisions.

Updated 15 July 2024

Please note: This is general tax information, not tax advice in any form. MoneyHub does not give tax advice, nor does the IRD - that is a job for tax agents and accountants.

Summary of Tax and Investments (Covering KiwiSaver, PIE Funds, Shares, Cash Savings and Property)

Background to our guide:

Our guide covers:

Further information: We suggest reading our capital gains tax and bright-line rules for property guides.

Please note: This is general tax information, not tax advice in any form. MoneyHub does not give tax advice, nor does the IRD - that is a job for tax agents and accountants.

Summary of Tax and Investments (Covering KiwiSaver, PIE Funds, Shares, Cash Savings and Property)

- Tax on KiwiSaver, Managed Funds, Index Funds and PIE Funds: Income generated (i.e. dividends and interest payments on cash invested) from KiwiSaver funds are taxed at the PIE rate (10.50%, 17.50% and 28%), depending on what the investor's annual income is. No tax is charged on capital gains your fund makes.

- Tax on Shares: There is no tax on the gains from investing in New Zealand and most Australian shares. For example, Sydney Airport, which is a stapled security share, is included in the FIF rules. However, tax on foreign shares (e.g. US or UK based) over $50,000 is calculated under the FIF rules which includes consideration of any capital gains.

- There are two methods of calculating tax under the FIF rules being either FDR or CV and the method that produces the lowest tax is chosen. This can be complicated, so we suggest reading an expert guide to help you understand your obligations if you own non-New Zealand or Australian shares.

- However if you invest in overseas shares through a managed funds or KiwiSaver provider the fund manager will calculate and pay any FIF taxes through the fund. For NZ and most Australian shares you pay taxes only on the income generated by shares (i.e. dividends) at the applicable RWT rate (currently up to 39%).

- Tax on Bonds, Term Deposits and Savings: Interest payments generated from cash deposits are also taxed at an applicable RWT rate of up to 39%.

- Tax on Property: Gains in property values are not taxed for the family home (first primary residence). This means if you buy a house for $800,000 and sell it for $1,000,000, the gain is tax-free. However, investment properties are subject to the Brightline Test as outlined by the IRD.

- Important: There are no capital gains on New Zealand and most Australian shares, unless you are classed by the IRD as a "trader" and buy/sell with the intent of immediate profit, but the IRD will assess 'trading' on a case by case basis.

Background to our guide:

- Tax is a topic that can quickly get complex and confusing, especially in the context of investing. Tax season is typically a stressful time for many investors (both retail and institutional).

- To help make everything clearer, our guide outlines the basics of investment taxes to help ensure you’re aware of what payments you need to make when payments are due or what refunds you’re potentially owed.

- This guide aims to be a simple way for investors to understand the different types of tax in New Zealand (RWT, PIR, PAYE rates etc.), the tax treatment given for each asset class (Shares, Bonds, Property, Managed Funds, KiwiSaver) while answering Frequently Asked Questions.

Our guide covers:

- Understanding Resident Withholding Tax (RWT)

- Tax on asset classes:

- Tax on KiwiSaver, Managed Funds, Index Funds and PIE Funds

- Tax on Shares

- Tax on Bonds, Term Deposits and Savings

- Tax on Property

- Tax on Crypto

Further information: We suggest reading our capital gains tax and bright-line rules for property guides.

Understanding Resident Withholding Tax (RWT)

- Your RWT rate is self-chosen and based on your estimated total income in the current financial year (1 April to 31 March).

- During the financial year, it’s best to pick an RWT rate that is in line with how much income you’re most likely to make (income, in this case, includes things like wages, interest from term deposits or dividends from shares).

- Keep in mind that RWT only considers the income you’ve received – not capital gains. There is no capital gains tax owing unless you are classified as a trader (or have invested more than NZ$50,000 overseas – which is enforced as a quasi-capital gains tax. For more information, see FIF taxes on the IRD website).

- We outline PAYE tax rates here.

What is the RWT scale?

- Typically, the largest source of income for a person is the annual salary or weekly wages they get from working in a primary job.

- This can be calculated by your employer or can be worked out yourself.

- The RWT bands range from 10.5% on the lower end to 39% at the upper end. This scale is progressive.

- The Inland Revenue (IRD) will also tell you if you have underpaid or overpaid according to the information they have and the payments they’ve received to date.

- If in doubt, you might consider putting a slightly higher rate (e.g. if you think you might make close to $75,000 – it can pay to put 33% as your RWT rate at the start of the financial year to ensure you won’t incur a tax bill at the end of the year).

When do I need to file my tax return? Will I pay tax?

- Income tax returns are typically due a few months after financial year-end (e.g. for the year ending 31 March, your income tax return is due before 7 July).

- Most investing and brokerage platforms will keep a record of how much tax needs to be paid for each investor. If you are a wage worker with no other taxable income, it's likely you won't need to file a tax return.

- After the financial tax year ends, platforms typically notify investors of their tax balance and provide some time for investors to deposit money and pay any outstanding tax amounts owing.

- The alternative process is to file a tax return directly with the IRD.

Tax on KiwiSaver, Managed Funds, Index Funds and PIE Funds

Every KiwiSaver fund is classed as a PIE Fund, meaning the interest and dividend earnings are taxed at a maximum rate of 28% (vs the highest income tax rate of 39%). We explain the need to make sure you've confirmed the correct tax rate to maximise your investment returns and minimise any unfavourable tax bill.

What is a PIE fund? What rate do I get taxed at for a PIE entity if I participate in one?

The PIE tax rules were created to cap the effective tax rate you pay on your investments (currently set at a maximum of 28%). The amount of taxable income or loss allocated to an individual is calculated daily and attributed (i.e. deducted from the investment) at the end of each quarter.

Which is a PIR?

A prescribed investor rate (PIR) is the rate used to calculate how much tax you'll pay on your portfolio investment entity (PIE) taxable income. Depending on your circumstances, individual investors could choose a PIR of: 10.5% 17.5% 28%. It’s important to select the correct PIR. This is by understanding a combination of:

The individual PIR is determined based on whichever year has the lower combined income amount. If your actual PIR is lower than the PIR you set, you may be able to obtain a refund on the tax paid. If you select a PIR tax rate that is too low, you may have to file a tax return and pay tax at your marginal tax rate.

Know This: You can easily change your PIR at any time by completing a ‘Notice to Change PIE Details’ form, typically through the investment platform you use to invest.

In relation to dividends, imputation credits represent a payment to you for the tax that was paid by businesses on profits generated in New Zealand. Imputation credits were implemented to prevent double taxation, where a company has paid company tax already. This is to ensure individual investors don’t pay tax twice. Imputation credits are explained clearly here.

- The total taxable income (including worldwide income);

- The last two income tax years of PIE income (an income year is from 1 April to 31 March).

The individual PIR is determined based on whichever year has the lower combined income amount. If your actual PIR is lower than the PIR you set, you may be able to obtain a refund on the tax paid. If you select a PIR tax rate that is too low, you may have to file a tax return and pay tax at your marginal tax rate.

Know This: You can easily change your PIR at any time by completing a ‘Notice to Change PIE Details’ form, typically through the investment platform you use to invest.

In relation to dividends, imputation credits represent a payment to you for the tax that was paid by businesses on profits generated in New Zealand. Imputation credits were implemented to prevent double taxation, where a company has paid company tax already. This is to ensure individual investors don’t pay tax twice. Imputation credits are explained clearly here.

How is KiwiSaver taxed?

As a KiwiSaver is a PIE, it will be taxed differently depending on what your income levels are. The rate of tax you pay on KiwiSaver follows the PIR rates (see Table 1 below), which is largely determined by how much you earn. The Inland Revenue can directly notify KiwiSaver providers to show that the investor is on the wrong PIR. You will then be notified by the investment platform you use if this is the case.

Important: Ensure you’re on the right tax rate

All KiwiSaver providers will have to show which specific tax bracket you are classed under. Sometimes this is asked before setting up your KiwiSaver, or the platform will make an assumption for you. It’s important to check this is right as early as possible. In the instance you are on a lower rate than you should be on, you will end up with a large tax bill at financial year-end.

To avoid any tax issues, as a rule of thumb for PIR rates:

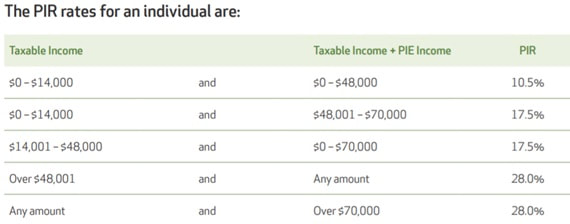

Table 1 - KiwiSaver PIR rates (source: KiwiSaver Form)

To avoid any tax issues, as a rule of thumb for PIR rates:

- With an annual income above $48,000, you’ll pay tax on KiwiSaver at the rate of 28%.

- With an annual income between $14,000 and $48,000, and you’ll pay tax on KiwiSaver at the rate of 17.5%.

- With an annual income of $14,000 or less, you pay tax on KiwiSaver at 10.5%.

Table 1 - KiwiSaver PIR rates (source: KiwiSaver Form)

Important: The tax you pay doesn’t come out of your salary. Instead, it's deducted from the investment balance, so this effectively reduces the overall return you make on your investments.

How are managed funds and index funds taxed?

As stated previously, managed funds are taxed at a PIR level. Just as with KiwiSaver, you’re able to set your PIR rate on the brokerage platform you use to make investments. Tax is normally applied to the investment income received by the managed fund itself. Tax is also calculated when you sell any units at the end of the tax year.

Know This: You don't need to keep tabs on the tax incurred - investment platforms and your fund manager(s) will keep a record of how much tax that needs to be paid (or is owed) and typically connect their data to The IRD. This means tax gets deducted (or paid into your account) after 31 March automatically.

Know This: You don't need to keep tabs on the tax incurred - investment platforms and your fund manager(s) will keep a record of how much tax that needs to be paid (or is owed) and typically connect their data to The IRD. This means tax gets deducted (or paid into your account) after 31 March automatically.

Tax on Shares

Typically, New Zealand shares are not subject to capital gains tax when they're sold or go up in value. Only the income derived from holding these shares will be subject to tax (e.g. dividend tax). We explore the tax obligations for shares (and their related components) below:

1. Company dividends

The dividends from shares will count as income and are taxable. This is likely a mixture of RWT and imputation credits (whether imputation credits are attached and paid for by the company will change depending on the type of dividend paid).

When you receive a dividend from holding shares, the tax will already have been deducted from the amount you receive. Most brokerage platforms make sure the RWT and dividend imputation credits are organised appropriately. Some brokerage platforms will pay the owed tax from dividends to The Inland Revenue directly on your behalf.

2. ETF dividends

Dividends received from investing in ETFs is taxable. This rate is typically at 28%, given New Zealand ETFs are classed as listed PIEs, which means the tax rate is fixed at 28%). The tax owing is typically managed and deducted by the fund provider (e.g. Smartshares or Vanguard).

3. International shares

To understand whether international shares get taxed, there are important considerations to be aware of:

a) Location of shares

New Zealand investors in New Zealand companies are not subject to the same taxes that overseas investments are. This means that a foreign investment typically needs to earn over 1% extra each year just to cover the additional tax owing.

Know This: The IRD allows imputation credits on tax paid by a New Zealand-based company to the IRD, effectively reducing the personal investor’s tax bill. International shares do not have this ability. For each country, the tax rules are different. This guide will not analyse each country in-depth as it is tailored for beginners. We suggest contacting a tax accountant if your needs are complex.

b) Investing overseas opportunities

Overseas investments can be attractive compared to New Zealand investment for a few reasons:

c) Tax structure

Choosing the wrong tax structure can add unnecessary cost at the end of the financial year. Most retail schemes don't do this, but there have been examples so it pays to be aware. Tax leakage is also a potential issue. Tax leakage occurs, in certain countries, when withholding taxes on an offshore dividend payment cannot be fully claimed as a Foreign Tax Credit (FTCs). FTCs are a proxy for tax payment to the IRD, where you have effectively paid the relevant tax to another government. You can claim them from Australian and USA-listed shares.

d) Cost and Time

Calculating taxes can take up a significant amount of time and effort. Overseas funds add another layer of complexity that you must navigate. You can file a tax return yourself – however, the added cost for calculating this yourself can grow to much more than expected. Utilising an accountant to complete your tax return can actually save more time and money.

Know This: Tax Treatment of Index Funds and ETFs vs Individual Shares

Know This: You don't need to keep tabs on the tax incurred - investment platforms and brokerage companies will keep a record of how much tax that needs to be paid (or is owed) and typically connect their data to The IRD. This means tax gets deducted (or paid into your brokerage account) after 31 March automatically.

1. Company dividends

The dividends from shares will count as income and are taxable. This is likely a mixture of RWT and imputation credits (whether imputation credits are attached and paid for by the company will change depending on the type of dividend paid).

When you receive a dividend from holding shares, the tax will already have been deducted from the amount you receive. Most brokerage platforms make sure the RWT and dividend imputation credits are organised appropriately. Some brokerage platforms will pay the owed tax from dividends to The Inland Revenue directly on your behalf.

2. ETF dividends

Dividends received from investing in ETFs is taxable. This rate is typically at 28%, given New Zealand ETFs are classed as listed PIEs, which means the tax rate is fixed at 28%). The tax owing is typically managed and deducted by the fund provider (e.g. Smartshares or Vanguard).

3. International shares

To understand whether international shares get taxed, there are important considerations to be aware of:

a) Location of shares

New Zealand investors in New Zealand companies are not subject to the same taxes that overseas investments are. This means that a foreign investment typically needs to earn over 1% extra each year just to cover the additional tax owing.

Know This: The IRD allows imputation credits on tax paid by a New Zealand-based company to the IRD, effectively reducing the personal investor’s tax bill. International shares do not have this ability. For each country, the tax rules are different. This guide will not analyse each country in-depth as it is tailored for beginners. We suggest contacting a tax accountant if your needs are complex.

b) Investing overseas opportunities

Overseas investments can be attractive compared to New Zealand investment for a few reasons:

- There is significantly more choice and more thematic focused funds that are not offered in New Zealand (e.g. China, Fintech, Space etc.)

- Investors have a broader range of investment managers to choose from, and the fees are typically much lower than in New Zealand, given there is more competition.

- The highest growth companies are typically listed offshore (even New Zealand’s top companies do this – e.g. Xero, Rocket Lab, Anaplan etc.)

- In general, you will pay much more tax investing in overseas shares than if you invested in New Zealand index funds or companies. This should be considered when investing in offshore ETFs, funds or companies.

c) Tax structure

Choosing the wrong tax structure can add unnecessary cost at the end of the financial year. Most retail schemes don't do this, but there have been examples so it pays to be aware. Tax leakage is also a potential issue. Tax leakage occurs, in certain countries, when withholding taxes on an offshore dividend payment cannot be fully claimed as a Foreign Tax Credit (FTCs). FTCs are a proxy for tax payment to the IRD, where you have effectively paid the relevant tax to another government. You can claim them from Australian and USA-listed shares.

d) Cost and Time

Calculating taxes can take up a significant amount of time and effort. Overseas funds add another layer of complexity that you must navigate. You can file a tax return yourself – however, the added cost for calculating this yourself can grow to much more than expected. Utilising an accountant to complete your tax return can actually save more time and money.

Know This: Tax Treatment of Index Funds and ETFs vs Individual Shares

- Index funds, ETFs and individual shares will all have different tax treatment. It can be difficult to understand which vehicle is most tax-efficient as it will depend on the combination and number of investments made.

- When investing in index funds, you usually get a better tax treatment if the fund is New Zealand based and has registered with IRD as a PIE. This means the most tax the fund will pay is 28% (whereas the individual top tax rate is 39%). In this sense, an index PIE fund may be more efficient if your personal income levels are in the top two brackets (greater than $70,000).

Know This: You don't need to keep tabs on the tax incurred - investment platforms and brokerage companies will keep a record of how much tax that needs to be paid (or is owed) and typically connect their data to The IRD. This means tax gets deducted (or paid into your brokerage account) after 31 March automatically.

How do I know if I'm flagged as a trader vs an investor? What if some of my portfolio is long-term and some is short-term buy and sell?

Important: The Inland Revenue doesn't 'flag' customers as traders, investors or for that matter long-term holders or short-term buyers and sellers. We asked the IRD to explain the situation of "trader" vs "investor". In providing an answer to the second part of the question, the IRD has interpreted "flagged" to be "treated as".

In relation to share investments, the key considerations with respect to profits or losses on the sale of shares as personal property are whether:

The IRD considers all relevant facts and considers each case on its own facts. It considers what weight should be given to different facts and follows specific guidance from case law and from the Commissioner's public statements about specific aspects, in particular;

In relation to share investments, the key considerations with respect to profits or losses on the sale of shares as personal property are whether:

- The shares which were sold were acquired with the intention of sale.

- The shares were sold as part of a profit-making scheme.

- The shares are sold by a person who also has a business of selling shares.

The IRD considers all relevant facts and considers each case on its own facts. It considers what weight should be given to different facts and follows specific guidance from case law and from the Commissioner's public statements about specific aspects, in particular;

- Short term buying and selling shares is more likely to be considered taxable

- Long term holding may be less likely to be considered taxable

- Regular trading is more likely to be considered taxable

Tax on Bonds, Term Deposits and Savings

How are bonds taxed?

Similar to term deposits and savings accounts, the coupons (or interest) received on bonds is taxable and will count as income (in general). Corporate bonds may have imputation credits attached when the coupons are paid out, but this will depend on the company and the type of bond. You can read more about investing in bonds here.

How is interest on term deposits and savings accounts taxed?

Any interest accrued from term deposits or savings accounts will be taxable under RWT. This is typically included as income (meaning the interest amount will be added to your other sources of income, e.g. primary job).

Tax on Property

Gains in property values are not taxed for the family home (first primary residence). This means if you buy a house for $800,000 and sell it for $1,000,000, the gain is tax-free. However, investment properties are subject to the “Brightline Test”.

Crypto

What do I need to know about tax implications for crypto?

- The Inland Revenue has clarified the position on tax obligations relating to cryptocurrencies in a guideline here and Cryptoassets (ird.govt.nz).

- As crypto-assets continue to evolve, Inland Revenue will progressively update these guidelines to provide people greater certainty on their compliance obligations.

- If you have specific questions or ideas for updates, you can e-mail [email protected] to start a conversation with the Inland Revenue.

- In July 2024 it was reported the IRD is looking into crypto investors and their tax obligations.

Frequently Asked Questions

It's likely you'll have some questions when it comes to tax on investments and savings. To help, we've answered some commonly asked questions below:

Do I get taxed on dividends?

Yes - dividends from any New Zealand companies are considered income and will be subject to income tax. Dividends from listed companies are paid through a share registry (e.g. Computershare and Link Market Services in New Zealand) into your bank account. Dividends are typically taxed before you receive the amount (e.g. dividend imputation credits). You can read more about dividend tax on the IRD's website.

What are the personal income tax rates?

Our PAYE Tax Rates outlines the rates.

I earned less than NZ$100 in dividends this year total. Am I subject to tax?

Yes, all dividends are subject to tax. Per the IRD, dividends and unit trust distributions are all taxed at a resident withholding tax rate of up to 39%, while portfolio investment entities (PIEs) are taxed at a maximum of 28%. How much tax you pay depends on your total income in the tax year.

Are there capital gains in New Zealand?

There are no taxes paid on capital gains in New Zealand (except the bright-line test, which applies to buying and selling residential property). Income tax is a major source of taxation revenue for the government, which is primarily generated from tax on income from employment, dividends from shares and interest on savings, etc.). Employers, banks and brokerage platforms will typically deduct a proportion of your dividend or interest income as RWT first and pay out the difference to your investment or bank account.

However, Foreign Investment Fund (FIF) tax acts as quasi-capital gains tax (see above), which will affect your investment returns in assets over $50,000 held outside of New Zealand (except for most, but not all, Australian shares).

Further information: We suggest reading our capital gains tax and bright-line rules for property guides.

However, Foreign Investment Fund (FIF) tax acts as quasi-capital gains tax (see above), which will affect your investment returns in assets over $50,000 held outside of New Zealand (except for most, but not all, Australian shares).

Further information: We suggest reading our capital gains tax and bright-line rules for property guides.

Concerning FIF/overseas investments, if my portfolio at the beginning of the financial year is below $50,000, grows to $70,000, but I sell ~$25,000 before the end, how does that get taxed?

Customers can opt into the FIF rules. Where the market value of someone's foreign investments is below or equal to NZ$50,000 on 1 April, that person is not affected by the FIF rules. The foreign shares sold during the income year which has resulted in either a profit or loss may give rise to other tax obligations (including if in the business of buying or selling shares, intention of selling the shares at the time of acquisition, or a dealer in shares).

Am I considered a Day Trader? What tax rates would I be subject to?

If you are trading shares regularly with the intention to profit off share price movements, then you could be classified as a “trader” by The Inland Revenue Department. This guide from Sharesight best explains 'trader' and the intent behind the behaviour. Once you’re considered a “trader”, you’ll be liable to pay tax on any capital gains from the sale of those shares.

However, The IRD does not clarify any hard metrics around what classifies as a trader (e.g. number of trades per year or trade sizes). The IRD focus more on intent as opposed to activity. For this reason, most people participating in the sharemarket buy shares, hold them for a few months (or more), and sell them. Such activity is not considered trading, and therefore there will not be capital gains taxes charged.

However, The IRD does not clarify any hard metrics around what classifies as a trader (e.g. number of trades per year or trade sizes). The IRD focus more on intent as opposed to activity. For this reason, most people participating in the sharemarket buy shares, hold them for a few months (or more), and sell them. Such activity is not considered trading, and therefore there will not be capital gains taxes charged.

I've been told by my employer that IRD based my return on 26 fortnightly payments even though it was a 27 fortnight tax year. Now I owe tax, is there any room to explain this?

The IRD provides information regarding weekly and fortnightly deductions in table format here. The IRD specifically discusses extra pay period write-offs (applies to the 2020 tax year and beyond); they will write off the full amount of tax if the assessed tax to pay is only because of the extra pay period. See this guide for more details.

If you are eligible for the type of write-off described above, IRD will apply the write off at the time they issue your assessment. IRD may request more information regarding this issue, but once this has been confirmed, the IRD will send through an income tax assessment that will show any appropriate automatic write-offs.

You can contact the IRD at any time if you have questions about your tax assessment using the secure message option under 'Correspondence" in your myIR account.

If you are eligible for the type of write-off described above, IRD will apply the write off at the time they issue your assessment. IRD may request more information regarding this issue, but once this has been confirmed, the IRD will send through an income tax assessment that will show any appropriate automatic write-offs.

You can contact the IRD at any time if you have questions about your tax assessment using the secure message option under 'Correspondence" in your myIR account.