Lending Crowd Review

- Lending Crowd closed down in mid November 2023 - please visit our guides to personal loans and car finance for more information on alternative lenders.

- The review below explains the Lending Crowd platform historically - will will delete this page in late 2024.

Updated 17 July 2024

(Historical) Summary of Lending Crowd

Borrowers: Borrow up to $200,000 (secured) or $50,000 (unsecured) at between 5.03% and 20.26% per annum for 2 to 5 years.

Borrowers: Borrow up to $200,000 (secured) or $50,000 (unsecured) at between 5.03% and 20.26% per annum for 2 to 5 years.

- Fees of $200 to $1,450 apply per successfully funded loan, depending on the size of the borrowing.

- Early repayment permitted without penalty.

- Lending Crowd helpfully gives interest rate quotes without any commitment, so potential borrowers know exactly what they will pay within two minutes.

Lenders (aka Investors): Earn between 5% and 14% per annum after fees with peer to peer lending.

- The minimum investment is $50

- Loans are personal and commercial and are either secured or unsecured

- Investments are between two and five years.

- Lending Crowd’s historical bad debts between 2016 and to date average is 0.207%. The maximum rate for any risk category is 8.707% (the C3 category).

- No early redemption is allowed, so once you invest, you'll need to wait for the loan to be repaid.

- Lending Crowd charges a fee of 10% to 25% of the interest earned.

Our Guide to Lending Crowd

Know This: We look at Lending Crowd for Lenders and Lending Crowd for Borrowers separately to best understand the pros and cons of this investment and borrowing platform.

- In this guide, we analyse Lending Crowd, a growing peer-to-peer lending (P2P) platform operating in New Zealand.

- Since its debut in 2016, the platform has allowed retail investors (i.e. individuals) to lend money to New Zealand consumers and businesses seeking personal loans.

- In 2020, Lending Crowd lent around $13m to consumers; lenders are enticed by higher returns with lower-than-expected default rates, and borrowers are attracted to the competitive interest rates, with 6.49% p.a. being the introductory rate for applicants with good credit.

- Lending Crowd has lent to over 5,000 borrowers on its platform, providing both secured personal loans and secured business loans.

- Lending Crowd charges fees to both lenders and borrowers, and does not lend any money itself. It acts as the middleman by way of providing a platform.

Know This: We look at Lending Crowd for Lenders and Lending Crowd for Borrowers separately to best understand the pros and cons of this investment and borrowing platform.

Lending Crowd Review: Borrowers

Lending Crowd's borrowers are, historically, individuals wanting to borrow money to buy a car, repay debt, pay for a wedding or help with home renovations.

Lending Crowd has a strict application process - only individuals who meet the following criteria can borrow from the platform:

You will be assigned a credit grade which ultimately decides the interest rate on the loan. The better your credit grade (i.e. A1 or A2 vs C1 or C3), the lower the interest rate. Lending Crowd offers a fixed rate range from 5.03% p.a. to 20.26%. If you accept a loan, you'll be charged fee, added to the loan total per the Amount Borrowed and Platform Fee schedule:

Lending Crowd has a strict application process - only individuals who meet the following criteria can borrow from the platform:

- Be at least 18 years old

- Be able to afford the loan you are applying for

- Provide identity confirmation with either a valid New Zealand Driver’s License or a valid New Zealand Passport.

- Provide bank statements for the last three months (these will be processed and assessed by a loan consultant to see your borrowing ability)

- You’ll need to list all income sources, your assets (e.g. house, investments, savings etc.), liabilities (e.g. credit cards, personal loans etc.) and your mortgage or rent expenses (separately from liabilities)

You will be assigned a credit grade which ultimately decides the interest rate on the loan. The better your credit grade (i.e. A1 or A2 vs C1 or C3), the lower the interest rate. Lending Crowd offers a fixed rate range from 5.03% p.a. to 20.26%. If you accept a loan, you'll be charged fee, added to the loan total per the Amount Borrowed and Platform Fee schedule:

- $2,000 - $5,000: $200

- $5,050 - $50,000: $450

- $50,050 - $100,000: $950

- $100,050 - $200,000: $1,450

How does loan security work?

- Lending Crowd offers secured loans alongside unsecured loans, which means borrowers must have an asset (such as a car or property) which acts as a guarantee of the secured loan. If the borrower later can't repay the loan and defaults, Lending Crowd can get possession of the security, sell it and repay the investors who lent the money.

- Security allowed includes 'any registered motor vehicle or vehicles that are currently registered in the name of a loan applicant, and/or any residential or commercial property or properties registered in the name of a loan applicant' per Lending Crowd's terms and conditions.

- Lending Crowd also makes it clear that if you're purchasing a vehicle with your loan, you can also use the vehicle you're purchasing as security.

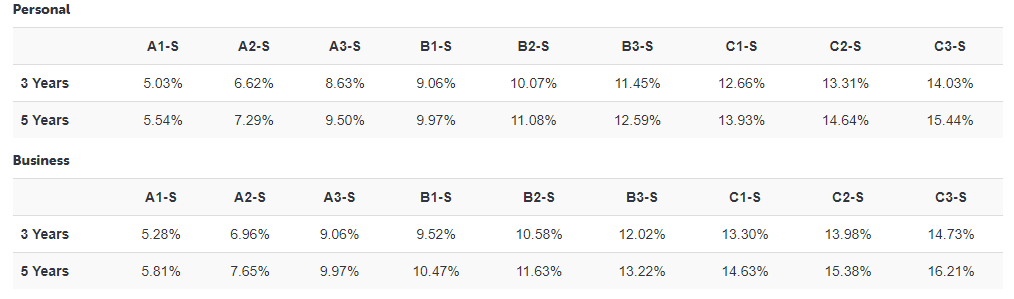

Lending Crowd Interest Rates

When a loan application is approved, it is assigned a "grade" with a corresponding interest rate. Lending Crowd currently offers the following interest rates:

Benefits of Lending Crowd

A major benefit of borrowing through Lending Crowd is that it's 100% managed online without paperwork. Decisions are made quickly, with a personalised interest rate which takes into account your credit history, income and assets.

Another benefit is the zero penalty for paying loans off early. This differs from other personal loan providers, and early repayment is very common on the Lending Crowd platform, with a number of loans being paid off early.

Have the best chance of being funded by being open, honest and descriptive

The speed and success of a loan being funded will depend on how well you write your loan purpose description. A single sentence describing your purpose for the loan will convey distrust. A full paragraph as to the specific purpose of your loan will help to persuade lenders to fund your loan.

Borrowing limits based on credit grade

Lending Crowd does not have any borrowing limits per category, but there is an overall loan limit - minimum $2,000 and a maximum $200,000. In December 2018, the average balance of the loans per credit grade was:

Another benefit is the zero penalty for paying loans off early. This differs from other personal loan providers, and early repayment is very common on the Lending Crowd platform, with a number of loans being paid off early.

Have the best chance of being funded by being open, honest and descriptive

The speed and success of a loan being funded will depend on how well you write your loan purpose description. A single sentence describing your purpose for the loan will convey distrust. A full paragraph as to the specific purpose of your loan will help to persuade lenders to fund your loan.

Borrowing limits based on credit grade

Lending Crowd does not have any borrowing limits per category, but there is an overall loan limit - minimum $2,000 and a maximum $200,000. In December 2018, the average balance of the loans per credit grade was:

- A1: ~$18,000

- A2: ~$20,000

- B1: ~$18,000

- B2: ~$8,000

Borrowers are required to make interest and capital repayments; Lending Crowd also offers a 'Death and terminal illness' insurance option to cover the repayment of the loan. The fee is 4.5% of the amount being financed for individual loans (or 5.95% of the amount being financed for two-person loans) rounded up to the nearest $50, and is a one-off payment added to the loan value.

Lending Crowd: Borrowing Conclusion

- Lending Crowd offers a no-obligation quote for a loan with a specific interest rate, and the process is easy to follow and done online.

- Because of the limited number of loans being offered to lenders, loans more often than not will be funded within the same day or following day.

- Repayments work like any other debt, and there is a credit team to talk to if the borrower falls behind or needs to make a hardship application.

Lending Crowd Fees – How fees are charged to borrowers and lenders

Lending Crowd is not a lender, it is a platform and does not receive interest income from borrowers. Instead, it earns fees from both borrowers and lenders. None of the fees collected are paid to lenders.

Revenue from Borrowers

Revenue from Lenders

Revenue from Borrowers

- Each borrower pays between $200 and $1,450 as a platform fee when the loan is successfully funded

- If you repay your loan on time every month, Lending Crowd charges the borrower no other fees, and there are no fees for early repayment or discharging securities. This means if you take a loan out for three years and repay it all in six months, you will not be charged a penalty.

- A loan default interest rate of 20% is charged on all overdue loans, in addition to the agreed interest rate. This default interest is charged on the amount in arrears only.

- If the loan remains in default after 90 days, Lending Crowd will charge a number of overdue fees.

Revenue from Lenders

- Retail lenders (i.e. individuals or companies investing in Lending Crowd) pay a fee called 'interest flex' – 10% or 25% of the interest repaid on each $50 loan note. This fee is for managing borrower repayments and administering the loan for that lender's benefit. This means if your loans receive $100 per year in interest, Lending Crowd will charge you a fee of either $10 or $25 (being 10% and 25% of the gross interest received).

Lending Crowd Review: Lenders

Lending Crowd offers an alternative to putting money in a term deposit, bond or an investment in the sharemarket. The specs are simple - you lend your money directly to New Zealand individuals and/or businesses looking to borrow, for a 2 to 5 year period.

Loans usually range from $2,000 to up to $25,000 (but borrowers can apply for as much as $200,000), and interest rates charged to the borrower fall between 5.03 % to 20.26% depending on whether the borrower is an individual or a business, the term of the loan, and the level of credit risk. Generally, five-year business loans have higher interest rates (and therefore better returns) and three-year personal loans.

The platform is not without its risks and rewards, which we discuss in detail below.

Loans usually range from $2,000 to up to $25,000 (but borrowers can apply for as much as $200,000), and interest rates charged to the borrower fall between 5.03 % to 20.26% depending on whether the borrower is an individual or a business, the term of the loan, and the level of credit risk. Generally, five-year business loans have higher interest rates (and therefore better returns) and three-year personal loans.

The platform is not without its risks and rewards, which we discuss in detail below.

Lending Crowd's four risk categories and corresponding interest rates a borrower pays

Lending Crowd's 'Standard' vs 'Referred' Loans Fee Explained

Lending Crowd offers a financial incentive to third parties who introduce borrowers to their platform, known as a 'referrer'. For every successfully funded loan, the referrer will be paid 15% of the interest charged. The referrers are used by Lending Crowd to stimulate loan numbers on its platform. Because only secured loans are offered, Lending Crowd receives relatively fewer loan applications than other peer-to-peer lenders. The referral program is designed to boost the number of applicants.

What does this mean for investors?

Investors will see two types of loans that will be reflected on the investor dashboard, distinguished by their percentage interest flex (i.e. commission) displayed:

1. Standard Loans, pushed organically and through more traditional and digital marketing to the platform, where the interest flex will be 10%;

2. Referred Loans, pushed through referral programs to the platform, where the interest flex will be 25%. These loans originate from business-to-business partnerships, such as car dealers, brokers and online affiliates, as well as existing Lending Crowd members who have introduced friends and family to the platform.

Lending Crowd offers a financial incentive to third parties who introduce borrowers to their platform, known as a 'referrer'. For every successfully funded loan, the referrer will be paid 15% of the interest charged. The referrers are used by Lending Crowd to stimulate loan numbers on its platform. Because only secured loans are offered, Lending Crowd receives relatively fewer loan applications than other peer-to-peer lenders. The referral program is designed to boost the number of applicants.

What does this mean for investors?

Investors will see two types of loans that will be reflected on the investor dashboard, distinguished by their percentage interest flex (i.e. commission) displayed:

1. Standard Loans, pushed organically and through more traditional and digital marketing to the platform, where the interest flex will be 10%;

2. Referred Loans, pushed through referral programs to the platform, where the interest flex will be 25%. These loans originate from business-to-business partnerships, such as car dealers, brokers and online affiliates, as well as existing Lending Crowd members who have introduced friends and family to the platform.

Lending Crowd Risk Categories and Returns

Lending Crowd categorises its borrowers into nine grades of risk - A1, A2, A3, B1, B2, B3, C1, C2 and C3. A1 is the best grade, meaning its the least likely to default, but also pays the lowest return because the borrower is charged a lower interest rate. C3 is the riskiest grade and offers the highest return. What your return will be will depend on your willingness to take a risk with your money.

Lending Crowd's data suggests the default rate is very low - mostly 0%; the average default rate is 0.207%, and in the highest risk category (C3), it is 8.707%.

Every Lending Crowd investor manually chooses what loans to invest in, meaning your money won't fund riskier loans unless you say so. Your role becomes a secondary credit analyst, weighing up the risks of an individual loan before deciding to fund the borrower.

Who can you lend to?

Lending Crowd presents investors with only qualified borrowers. Specifically:

Diversification of investment

To protect an individual investor, Lending Crowd makes $50 the minimum investment level. If you want to invest more than $50 in one loan, that is your choice as the platform does not limit this. Remember, diversification underlines a successful investment strategy, so allocating $50 'notes' to as many as loans as possible that meet your requirements is the best way to protect yourself from a borrower defaulting. For example, If you lend $1,000 to Lending Crowd, this can be invested into 20 different loans ($50 X 20 loans = $1,000).

Loan Repayment

To best explain how Lending Crowd works, let's take an example of a loan of $50 lent to a borrower paying 6.89% for 3 years. In this situation, if you have loaned $50, at an interest rate of 6.89% over three years, the borrower will repay $55.44. Each month, this calculates to be a $1.54 repayment, meaning your Lending Crowd account will receive $1.54 each month for three years unless a repayment is missed or the loan defaults. As is the case with the amortisation of every loan, the interest portion you receive is higher at the beginning of the term of the loan repayments and reduces as balance reduces.

Example of loans

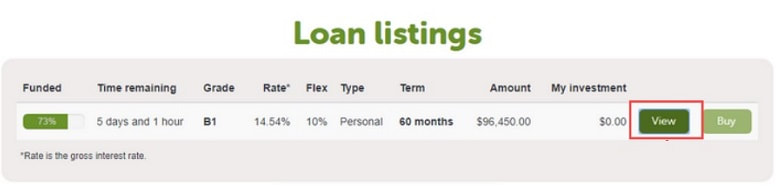

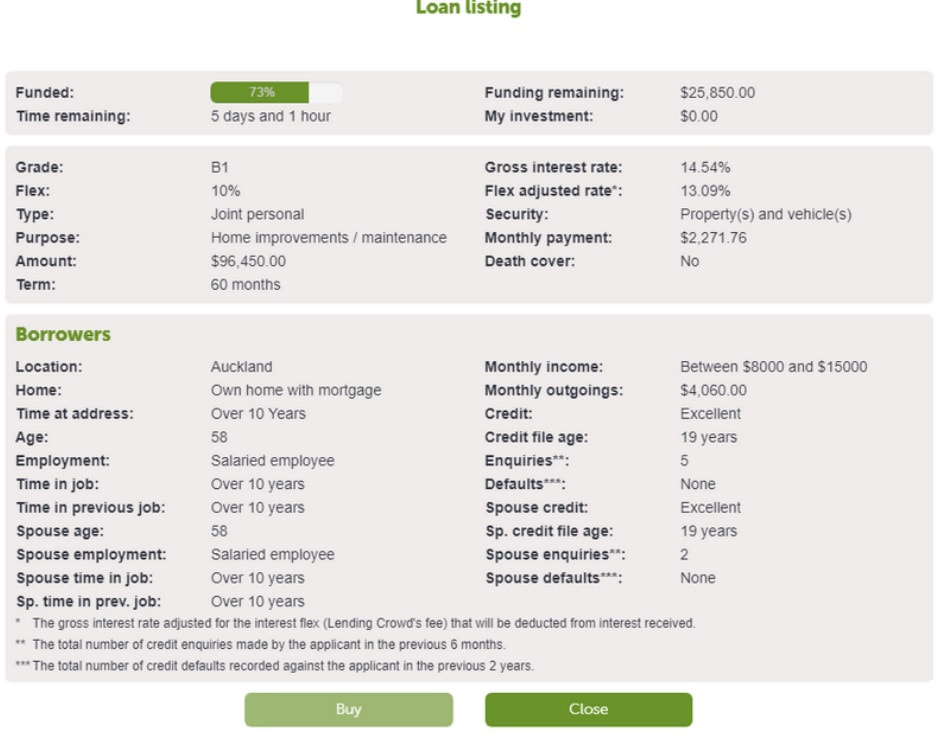

We present a sample of loans from Lending Crowd awaiting funding below; you can see details of the purpose, the Lending Crowd-assessed grade, term (months), loan amount, estimated monthly repayment and the amount funded, as well as details about the loan's purpose, the age of the borrowers, their income and their security. Importantly, the loan details show the 'flex adjusted rate' which is the interest rate you as a lender will receive.

Lending Crowd's data suggests the default rate is very low - mostly 0%; the average default rate is 0.207%, and in the highest risk category (C3), it is 8.707%.

Every Lending Crowd investor manually chooses what loans to invest in, meaning your money won't fund riskier loans unless you say so. Your role becomes a secondary credit analyst, weighing up the risks of an individual loan before deciding to fund the borrower.

Who can you lend to?

Lending Crowd presents investors with only qualified borrowers. Specifically:

- Borrowers must be over 18 years of age, have a good credit history and be a New Zealand resident.

- Every loan is classified within groups A1 to B2, depending on the individual’s income and credit risk.

Diversification of investment

To protect an individual investor, Lending Crowd makes $50 the minimum investment level. If you want to invest more than $50 in one loan, that is your choice as the platform does not limit this. Remember, diversification underlines a successful investment strategy, so allocating $50 'notes' to as many as loans as possible that meet your requirements is the best way to protect yourself from a borrower defaulting. For example, If you lend $1,000 to Lending Crowd, this can be invested into 20 different loans ($50 X 20 loans = $1,000).

Loan Repayment

To best explain how Lending Crowd works, let's take an example of a loan of $50 lent to a borrower paying 6.89% for 3 years. In this situation, if you have loaned $50, at an interest rate of 6.89% over three years, the borrower will repay $55.44. Each month, this calculates to be a $1.54 repayment, meaning your Lending Crowd account will receive $1.54 each month for three years unless a repayment is missed or the loan defaults. As is the case with the amortisation of every loan, the interest portion you receive is higher at the beginning of the term of the loan repayments and reduces as balance reduces.

Example of loans

We present a sample of loans from Lending Crowd awaiting funding below; you can see details of the purpose, the Lending Crowd-assessed grade, term (months), loan amount, estimated monthly repayment and the amount funded, as well as details about the loan's purpose, the age of the borrowers, their income and their security. Importantly, the loan details show the 'flex adjusted rate' which is the interest rate you as a lender will receive.

Average Loans

Unsecured Loans

A1-U |

A2-U |

A3-U |

B1-U |

B2-U |

B3-U |

C1-U |

C2-U |

C3-U |

$12,600 |

$13,900 |

$17,200 |

$11,700 |

$11,400 |

$12,550 |

$8,350 |

$7,000 |

$3,450 |

Secured Loans

A1-S |

A2-S |

A3-S |

B1-S |

B2-S |

B3-S |

C1-S |

C2-S |

C3-S |

$24,800 |

$29,750 |

$24,450 |

$22,650 |

$26,300 |

$24,150 |

$20,850 |

$22,500 |

$20,050 |

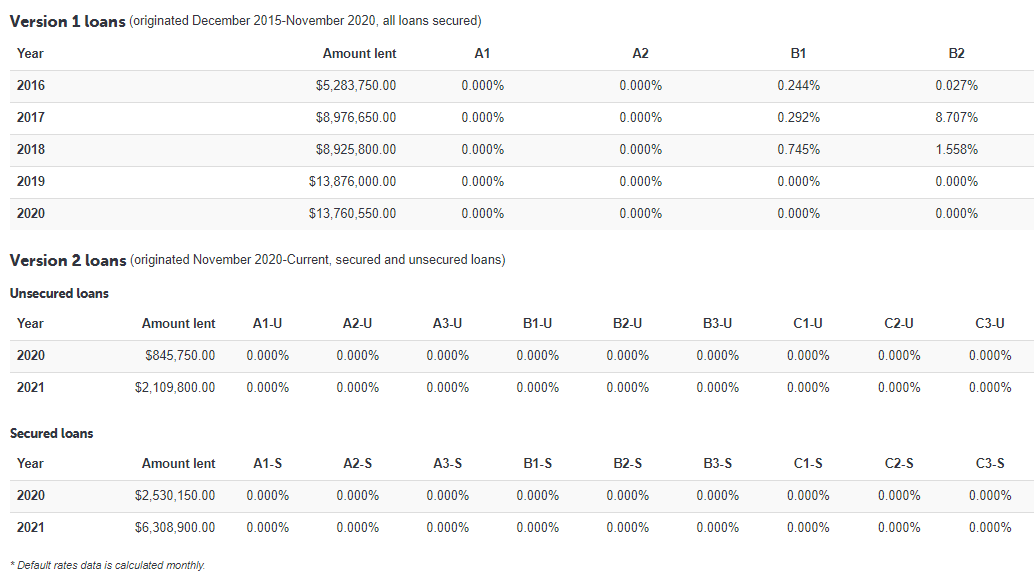

Lending Crowd Default Rates

Lending Crowd launched in December 2015 and is a relatively young platform. However, after 5+ yeara of transactions, the overall default rate sits at less than 0.21% over all loans.

Borrowers are graded A1 to C3, dependent on their risk profile. Within each group are two sub-groups (1 = best, 3 = worst). As of June 2019, loans in sub-grades B1 and B2 have seen minor defaults during 2016, 2017 and 2018 as indicated in the table below from Lending Crowd's website:

Borrowers are graded A1 to C3, dependent on their risk profile. Within each group are two sub-groups (1 = best, 3 = worst). As of June 2019, loans in sub-grades B1 and B2 have seen minor defaults during 2016, 2017 and 2018 as indicated in the table below from Lending Crowd's website:

Lending Crowd Borrowing Volumes

The amount a platform lends is important for two principal reasons:

Cumulatively, Lending Crowd has lent over $65 million since launching in 2016.

- Credit Modelling: The more Lending Crowd lends, the more data it has to build its credit processes and report to investors. 2016-2018 is a short period for credit assessment data collection, and as more loans are issued Lending Crowd gains more experience in evaluating credit risk.

- Higher investment opportunities: The more borrowers, the more funding opportunities for investors. The more the platform lends, the greater the probability of new lenders available to fulfil future loans.

Cumulatively, Lending Crowd has lent over $65 million since launching in 2016.

Lending Crowd Security

The average value of a loan across all risk categories is $16,000. The principal risk to any investment with Lending Crowd is the possibility of borrowers defaulting on their loan commitments, resulting from negative economic conditions in New Zealand and/or poor credit assessment by Lending Crowd.

Lenders are protected by limited exposure and robust credit assessments

Lending Crowd claims lenders are protected in two principal ways:

Our view:

- Fractionalisation – Lending Crowd promotes diversification by splitting up loans. Each loan is divided into packets of $50 called “notes”. Individual lenders lend $50 to each borrower, reducing exposure if one borrower defaults.

- Credit assessment - Lending Crowd's management claims to have the expertise, systems and processes to determine the suitability of a borrower and his or her ability to afford loan repayments

Our view:

- Lending Crowd is in its infancy as a lender but reports an incredibly low default rate among its borrowers, most likely achieved by requiring all loans to be secured.

- With just over 36 months of data as at December 2018, the platform is still learning. In saying this, the mechanics seem near-perfected with relatively less risky borrowers compared to other peer-to-peer platforms such as Harmoney which reports a much higher default rate.

- New loans are notified to lenders via email, and in some instances, a loan can be fully funded within five minutes. If you miss one loan opportunity, you will need to wait for another loan to come onto the platform. Lending Crowd is committed to attracting more borrowers to the market with its referral program.

What if a borrower doesn’t repay a Lending Crowd loan?

If a payment fails, Lending Crowd has a firm process to collect the money owed. For the first 90 days, Lending Crowd charges a 'default interest rate' of 20%. This means that the borrower will pay their agreed interest rate plus a penalty rate of 20% on the amount in arrears.

If payment has not been received, Lending Crowd will charge an arrears management fee ($40.00 per week), issue a repossession warning notice, property law notice and letter of demand (usually within 90 days of the loan payment being overdue). If the loan still remains unpaid, the credit collections team will seek repossession of the security listed on the loan and issue court proceedings.

A lender will be notified when a borrower’s loan goes into arrears and/or is written-off. With the $50 fractionalisation, lenders are diversified against defaults.

If payment has not been received, Lending Crowd will charge an arrears management fee ($40.00 per week), issue a repossession warning notice, property law notice and letter of demand (usually within 90 days of the loan payment being overdue). If the loan still remains unpaid, the credit collections team will seek repossession of the security listed on the loan and issue court proceedings.

A lender will be notified when a borrower’s loan goes into arrears and/or is written-off. With the $50 fractionalisation, lenders are diversified against defaults.

Withdrawing Lending Crowd Funds

Investors (i.e. lenders) can only withdraw money from the Lending Crowd platform when it has been repaid by a borrower. Lenders cannot withdraw funds that are currently invested. This means that once your money funds a loan, you will not have access to it until the borrower has repaid the loan you invested in. This is different from a bank's term deposit, which has a break penalty fee for immediate access.

Lending Crowd: Conclusion

- Lending Crowd offers a unique opportunity for New Zealanders looking for diversity in their investments. No other peer to peer lender currently offers the competitive returns and low default rate, but as always, past performance is no indication of future returns.

- Lending Crowd's 10% to 25% commission on interest income may seem high, but there are no other investor fees and the minimum investment is an affordable $50.

5 Lending Crowd Investor Must-Know Facts

|

Your money is stuck with borrowers until it's repaid, but many repay earlyLending Crowd offers a 'medium-term' investment of either three years or five years. If you're likely to need the money you invested in the short term, i.e. less than three years, Lending Crowd is not for you. Currently, there is no option to sell a loan investment to another lender. However, many borrowers repay early, so there is a good chance that your investment will be repaid to your account and made available to either reinvest or withdraw.

|

|

Fractionalisation and diversification reduce the impact of lossesLending Crowd promotes fractionalisation and loan diversification. Every $50 you invest is converted to one "loan note", but you can invest in as many loan notes as you like for the same loan. This means if you take the view that the borrower will repay, you can invest anything from $50 to the entire value of the loan.

|

|

Repayments can be withdrawn or re-invested, and uninvested funds earn 0% interestAs loan repayments are made monthly by borrowers, a typical lender will usually see a positive balance in their account. You can either re-invest this (if the balance is above $50) or you can withdraw whatever the amount is to your bank account. It's important to know that uninvested funds do not receive interest.

|

|

Lending Crowd doesn't share borrower informationWhen you make a loan, you'll see the borrower's location, age range and loan purpose. You won't know any more details than that. You'll need to make a decision with less data than a bank has, for example, as you're relying on Lending Crowd to have properly credit checked the borrower.

|

|

Your net return depends on many factors, and will likely vary between individual loansPer Lending Crowd, "your returns are directly dependent on the interest rate of the loans you invest in and the performance of those loans. The current interest rates of loans listed on Lending Crowd vary from 6.49% to 16.99%, from which Lending Crowd takes a fee". This fee will either be 10% or 25% on the interest received. For example, if you lent a borrower at 6.49% and your Lending Crowd fee was 10%, you would receive an interest return of 5.84% (6.49% less 10%).

Your actual return will also depend on any defaults - if the borrower is unable to repay the loan and Lending Crowd's procedures to have repossession of the security interest (i.e. the borrower's vehicle or property) do not lead to a recovery of the debt, your investment will be impaired. This means you could lose anything from 1 cent to $50 of each loan note lent. |