Margin Loans and Margin Lending Explained

Disclaimer: Margin lending and borrowing to invest are extremely high-risk strategies and should be undertaken with significant caution. We recommend you fully understand the basics of investing before considering this strategy. Our guide explains must-know facts, risks and costs to help you make an informed decision.

Updated 26 January 2023

Why we published this guide: MoneyHub is dedicated to bringing transparency and accessibility to all New Zealanders. Using margin to support living expenses or lifestyle purchases can be a great alternative for some people with higher risk tolerances, and just because these strategies are difficult to implement doesn’t mean New Zealanders should be kept in the dark about this. We want to “open source” the strategies that high net worths use and equalise the playing field for all New Zealanders.

Margin Lending Background:

For example, these notable billionaires have all pledged shares as collateral to borrow against, per a 2022 article in Forbes:

Amongst high-net-worth individuals, borrowing against shares isn't unusual. For example, Tesla executives can borrow up to 25% of the value of their Tesla shares, using their shares as collateral for the loan. This borrowing can be used to do anything, including investing in other shares, paying university fees, buying property or overseas travel. Often, this is a much more optimal strategy than selling shares (especially if people expect the shares to continue to do well in the future).

However, these types of strategies aren't just for the rich. While wealthy people always borrow against their equity portfolios and shares, most New Zealanders think they don't have access to these loans or, if they do, don't know where to start. But in reality, New Zealanders do have access. This guide has been publishes to explore the options, risks, costs and must-know considerations.

Know This FIrst: Public perception of leverage on property versus leverage on shares

Our guide covers:

Margin Lending Background:

- In the Apple TV show WeCrashed, Adam Neumann (played by Jared Leto) is seen trying to open a bank account, with the main issue being that he has billions of dollars in privately held shares that aren't liquid and not easily bought or sold.

- Instead, he talks with his private banker at JP Morgan to provide him with a line of credit pledged against his shares of WeWork. Through this strategy, JP Morgan offers Adam Neumann a $100 million credit line as an ultra-high net worth individual (UHNWI) against his $10 billion+ of shares in WeWork.

- While stories like these seem far fetched, this is a legitimate strategy used by people in the real world to continue investing in assets while supporting their cash flow and funding their lifestyles.

For example, these notable billionaires have all pledged shares as collateral to borrow against, per a 2022 article in Forbes:

- According to regulatory filings, Elon Musk, CEO of SpaceX and Tesla and the richest person in the world, has pledged about 267 million Tesla shares against margin loans to fund and support his lifestyle purchases (which included his purchase of Twitter)

- Larry Ellison, founder of Oracle

- Jim Walton (part of the Walton family that owns Walmart)

- Stephen Schwarzman (the founder of the private equity group Blackstone)

- Carl Icahn (the founder of activist investor Icahn Enterprises)

Amongst high-net-worth individuals, borrowing against shares isn't unusual. For example, Tesla executives can borrow up to 25% of the value of their Tesla shares, using their shares as collateral for the loan. This borrowing can be used to do anything, including investing in other shares, paying university fees, buying property or overseas travel. Often, this is a much more optimal strategy than selling shares (especially if people expect the shares to continue to do well in the future).

However, these types of strategies aren't just for the rich. While wealthy people always borrow against their equity portfolios and shares, most New Zealanders think they don't have access to these loans or, if they do, don't know where to start. But in reality, New Zealanders do have access. This guide has been publishes to explore the options, risks, costs and must-know considerations.

Know This FIrst: Public perception of leverage on property versus leverage on shares

- New Zealanders will regularly put 20% down on a property (effectively leveraging [borrowing] 5X their equity) and risk losing all of their deposit with a 20% downward move, but feel awkward about borrowing 10% of their share portfolio value to either invest (such as investing 110% of their equity into a Vanguard S&P 500 index fund or withdraw the borrowed 10% as a way to supplement cash flow and support paying their living expenses without needing to sell shares.

- There is a stigma around using non-property leverage. While this is somewhat justified given the high-profile failures associated with leveraging investments (such as Long Term Capital Management and Archegos Capital), if done prudently and right, there are some unique benefits that New Zealanders could get by getting more comfortable and learning more about non-property leverage.

- Given this is a highly controversial and complex topic, this guide initially walks through the basics of margin lending. Then, it gets into practical ways to implement the strategy, like:

- Margin lending to invest in shares (e.g. borrowing against your portfolio to invest in more shares).

- Margin lending to fund lifestyle purchases (such as the “Buy Borrow Die” strategy and borrowing against your portfolio to pay living expenses, invest in property, buy a car or fund a holiday).

Our guide covers:

- The Basics of Margin Lending

- How Can I Take Advantage of Margin Lending? Why Would I Want to Do It?

- What Platforms Offer Margin Loans?

- What Must-Know Characteristics of Margin Loans?

- Margin Lending vs Home Mortgages - Understanding the Difference

- Must-Know Facts About Margin Lending

- Frequently Asked Questions

MoneyHub Founder Christopher Walsh shares a Financial Risk Warning for Anyone Considering Margin Lending:

|

"Margin lending, while a tool for financial leverage, is not a one-size-fits-all solution. It's a high-risk strategy, akin to walking a tightrope without a safety net. Just because high-profile figures like Elon Musk successfully (for now) navigate this path doesn't mean it's the right choice for everyone.

The allure of amplifying investment returns can be tempting, but it is crucial to stay grounded and remember the potential for amplified losses. Before diving into margin lending, it's essential to understand that things can go wrong quickly. The markets are bearish and unforgiving, and a margin call can strike at the worst possible moment, forcing you into difficult financial decisions. I was at Auckland airport with a friend just after the GFC. We were having a great time as young grads in 'The Emirates Lounge' until ASB Securities notified him of their margin call. I remember the mood changing instantly and he had to sort things out. Margin calls are real and unforgiving. The debt accumulated through margin lending is not just numbers on a page; it's a liability that can have real-world consequences on your financial stability. Please take a moment to assess your financial situation. Many investing platforms make it easy for you to borrow, but are you prepared for the worst-case scenario? Do you have a solid plan to manage the borrowed funds? In the world of margin lending, common sense and a cautious approach are your best allies. Think critically about the downsides, and don't get swayed by the glamorous examples set by billionaires. Your financial health and peace of mind are paramount." |

Christopher Walsh

MoneyHub Founder |

The Basics of Margin Lending

What is Margin Lending?

Margin lending is a financial practice where an investor borrows money from a broker or financial institution to invest in the shares market or other financial securities. This borrowed money is typically secured against the investor's existing securities or cash deposits.

The amount an investor can borrow, known as the “loan-to-value ratio” (LTV or LVR), is typically a percentage of the value of their securities. This practice effectively increases the investor's buying power, allowing them to hold a larger position in shares or securities than they could with their funds alone.

For example, John invested $100,000 in his ASB Securities account (LINK) in Air New Zealand shares.

The amount an investor can borrow, known as the “loan-to-value ratio” (LTV or LVR), is typically a percentage of the value of their securities. This practice effectively increases the investor's buying power, allowing them to hold a larger position in shares or securities than they could with their funds alone.

For example, John invested $100,000 in his ASB Securities account (LINK) in Air New Zealand shares.

- Through a margin loan, John could borrow another portion of money (say 10%) from ASB Securities and invest an additional $10,000 into Air New Zealand shares (totalling $110,000 invested in Air New Zealand) by putting up his initial $100,000 as collateral in case the shares of Air New Zealand declines.

- Alternatively, if John didn’t want to add more shares but instead use the $10,000 to pay for his ongoing food and housing costs, John could withdraw $10,000 from his broker in cash (with his $100,000 in Air New Zealand shares held by the broker as collateral).

- This would effectively prevent John from having to sell $10,000 of his Air New Zealand shares, meaning he can keep this amount invested and avoid any potential tax complications of selling.

What is Margin Lending Used For?

Margin lending is used for various purposes, not just limited to investing in shares or ETFs. It can be a flexible financial tool for different needs:

- Buying More shares or ETFs: This is the most common use of margin lending. Investors leverage their investments to purchase additional securities, hoping to amplify returns.

- Everyday Living Expenses: Some investors use margin loans to access funds for daily expenses or to buy other assets, though this can be risky.

- Discretionary Expenses: In some cases, margin loans can be used as a temporary source of funding for things like car or real estate purchases, travel or other non-essential purchases. However, this is less common and comes with substantial risks over and above investing in shares or paying for everyday living expenses (namely, it is discretionary and may be putting people in higher risk situations without needing to).

Is Margin Lending Only for the Wealthy?

Contrary to common perception, margin lending is not exclusively for wealthy individuals with significant assets. You don't need millions of dollars in the bank or hundreds of thousands of dollars in income to access margin loans. Many brokerage firms offer margin lending services to typical investors. These investors can start with smaller loan amounts, using their existing investment portfolio as collateral.

Who Should be Doing Margin Lending?

While margin lending may be more widely accessible with brokerage platforms, it's still suggested that New Zealanders become comfortable and experienced with investing before trying this. This is a very high risk strategy and is not recommended for the majority of New Zealanders. Having said that, just because this is a high risk, unorthodox strategy doesn’t mean New Zealanders shouldn’t be aware of and understand how it works. For some, it can make a lot of sense (and as New Zealanders get wealthier over time, it pays to know all the potential options available to them).

Margin lending is generally suitable for more experienced investors who understand the risks and have a high risk tolerance. Margin lending is generally not suitable for conservative, risk-averse investors.

Margin lending is generally suitable for more experienced investors who understand the risks and have a high risk tolerance. Margin lending is generally not suitable for conservative, risk-averse investors.

How Can I Take Advantage of Margin Lending? Why Would I Want to Do It?

Anyone interested in margin lending can start by:

You may choose margin lending for several reasons:

- Opening a Margin Account: The first step is to open a margin account with a brokerage. This requires fulfilling certain eligibility criteria (like minimum account balances) and agreeing to the terms and conditions of margin trading.

- Understanding the Requirements: Familiarising oneself with the requirements, such as minimum equity, margin calls, and interest rates, is crucial.

- Assessing Risk Tolerance: Investors must assess their risk tolerance and investment goals before engaging in margin lending.

You may choose margin lending for several reasons:

- Leverage to Amplify Returns: By borrowing money, investors can purchase more securities than they could with their funds alone, potentially increasing their investment returns.

- Flexibility: Margin loans offer flexibility to quickly access funds for various needs, including taking advantage of investment opportunities. Access cash flow without needing to sell existing shares (and letting those shares grow in value).

- Low interest rates: Margin loans are often lower than credit cards, payday loans and traditional mortgages (depending on the broker). Effectively, there might be cost savings from withdrawing on margin to fund living expenses than spending on other sources of debt. Having said that, margin loans can be called back at any time compared to mortgages and credit cards, which have fixed rate, period payback periods, so are much more volatile and can introduce far more uncertainty.

- Diversification: Borrowing through margin lending can allow investors to diversify their portfolios without providing the full amount of capital upfront.

What are the main risks of margin lending?

Margin lending carries significant risks:

- Amplified Losses: Increased leverage can lead to greater losses if the asset value decreases.

- Margin call: If the value of the securities purchased on margin declines, the investor may be subject to a margin call, where they must deposit more funds or sell some of the securities to maintain the loan’s minimum margin requirements. Failure to meet a margin call can result in substantial losses, including the possibility of losing more than the initial investment.

- Interest Rate Risks: Often, interest rates on margin loans are floating and are tied to central bank interest rates, meaning any changes in interest rates (like the fed funds rate or the RBNZ OCR) can increase the cost of loan repayment, potentially leading to financial strain or asset liquidation at a loss.

- Risk of debt snowball: The longer you borrow money from your broker, the more interest you will rack up on that balance. Because you aren't on a fixed repayment schedule, assuming your portfolio is stagnant for periods, your margin loan will continue to accrue and grow, increasing your liabilities and putting more pressure on your portfolio.

- Added stress and repayment uncertainty: With alternative debt arrangements like a mortgage or personal loan, there is far more certainty and less complexity in paying down the debt (and a lender's ability to call the loan back).

What Platforms Offer Margin Loans?

Brokerage platforms and financial institutions typically provide margin lending. The most popular New Zealand financial services providers of margin lending are:

- Interactive Brokers (IBKR) (and relevant margin loan rates)

a. IBKR also offer Portfolio Margin accounts for customers with > USD 110,000 (NZD 180,000), offering better margin rates and less stringent margin requirements). - ASB Securities (with the associated margin lending application form and approved securities)

- Tiger Brokers (and related risks and disclosures)

- Hobson Wealth (see the terms and conditions for more information)

- Forsyth Barr (explained in this PDF brochure) and Leveraged Equities New Zealand (a related entity to Forsyth Barr)

How Does the Interest Accrued Work for Margin Lending? Is There a Repayment Schedule?

The interest structure for margin loans is unique:

- Interest Accrual: Interest on margin loans typically accrues daily based on the outstanding loan balance and is added to the margin loan balance monthly. The rate is usually variable and can change with market conditions.

- Repayment Schedule: Unlike traditional loans with fixed repayment schedules, margin loans are generally flexible. They are effectively interest-only loans, where the interest accrued is added to the loan balance. This means that there is no set schedule for repaying the principal (but will continue to grow over time so you ideally need a plan to pay this off over time).

- Payment of Interest: Interest payments are usually made monthly, but there is no requirement to pay down the principal as long as the account maintains the required level of equity.

- Loan Balance and Market Conditions: It's important to note that if the value of the securities purchased on margin declines significantly, it can trigger a margin call, requiring the investor to deposit additional funds or sell some securities.

What are the Must-Know Characteristics of Margin Loans?

1. You must keep a minimum amount of equity in the account (known as maintenance margin)

A critical aspect of margin lending is maintaining a minimum equity level in the margin account to ensure loan repayment in case of a collateral value drop. A formula and a margin percentage unique to each borrower determine this level. If asset values fall below this threshold, the lender issues a margin call, requiring the borrower to either reduce the loan amount or increase the collateral. Failure to comply could lead to the lender liquidating the collateral, whether shares, cryptocurrency, or other investments.

2. The more volatile an asset is, the lower the amount you’ll be able to borrow against it

Liquidity plays a vital role in securing favourable loan terms. More liquid collateral assets require a lower margin in the account since they can be easily converted into cash if the borrower defaults. Cash is considered the most liquid asset, followed by bonds and shares. For example, you’ll be able to borrow far more margin against an S&P 500 index fund compared to an individual high risk growth shares like Tesla.

3. The cost of borrowing can be very high depending on who’s providing the margin loan

Margin interest rates vary hugely depending on the broker. For example, as of January 2024, IBKR is charging 6.83% p.a. to borrow USD for balances up to $100,000 USD. In other words, if you borrowed $1,000 USD from IBKR for one year, you would incur $68.30 of interest at the end of the year (assuming the margin rate stayed the same for the entire year). This $68.30 would be added to the total loan balance (so your final balance would be $1,068.30). These numbers are approximate and might vary given interest accrues daily and rates change.

A critical aspect of margin lending is maintaining a minimum equity level in the margin account to ensure loan repayment in case of a collateral value drop. A formula and a margin percentage unique to each borrower determine this level. If asset values fall below this threshold, the lender issues a margin call, requiring the borrower to either reduce the loan amount or increase the collateral. Failure to comply could lead to the lender liquidating the collateral, whether shares, cryptocurrency, or other investments.

2. The more volatile an asset is, the lower the amount you’ll be able to borrow against it

Liquidity plays a vital role in securing favourable loan terms. More liquid collateral assets require a lower margin in the account since they can be easily converted into cash if the borrower defaults. Cash is considered the most liquid asset, followed by bonds and shares. For example, you’ll be able to borrow far more margin against an S&P 500 index fund compared to an individual high risk growth shares like Tesla.

3. The cost of borrowing can be very high depending on who’s providing the margin loan

Margin interest rates vary hugely depending on the broker. For example, as of January 2024, IBKR is charging 6.83% p.a. to borrow USD for balances up to $100,000 USD. In other words, if you borrowed $1,000 USD from IBKR for one year, you would incur $68.30 of interest at the end of the year (assuming the margin rate stayed the same for the entire year). This $68.30 would be added to the total loan balance (so your final balance would be $1,068.30). These numbers are approximate and might vary given interest accrues daily and rates change.

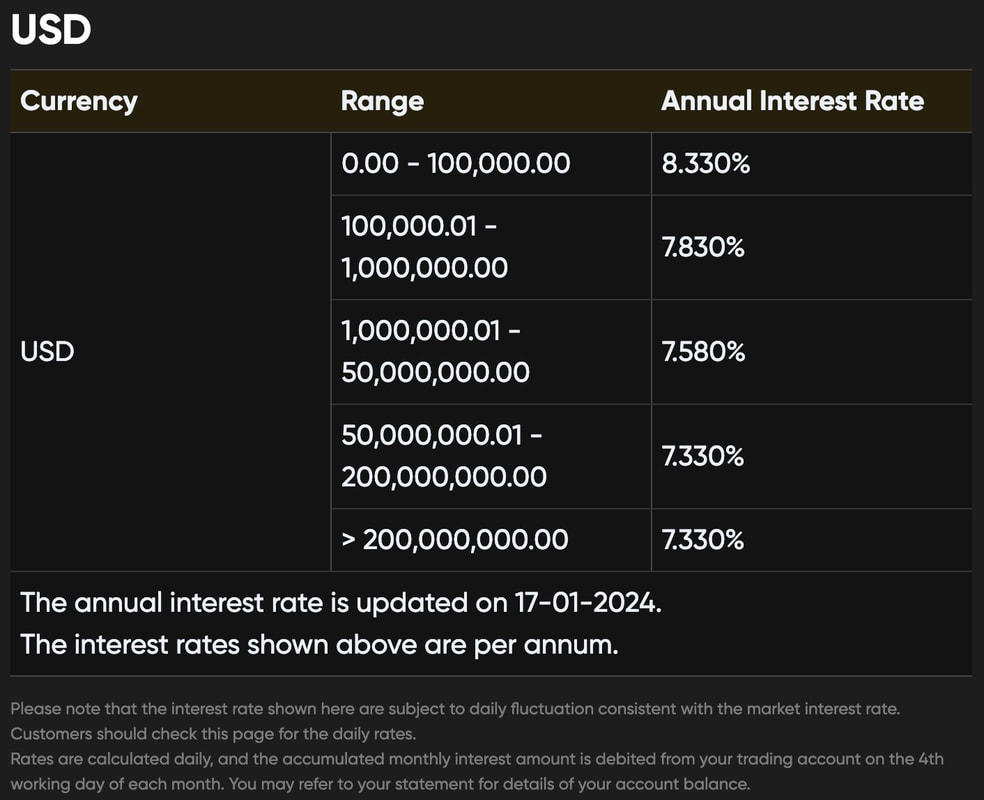

Exhibit: IBKR margin lending rates (per IBKR’s website)

Exhibit: Tiger Brokers Margin Rates (Per Tiger Brokers’ website).

In contrast, From the example above, Tiger Brokers is charging 8.33% on balances up to USD $100,000, more than 150 basis points above IBKR. You would effectively be charged 1.50% more a year to borrow the same amount of money. It would be the equivalent of you borrowing from ASB bank at 8.33% but then finding out that Westpac was offering the exact same terms and loan for 6.83%.

The above example emphasises the point that you need to do your research and compare all the different brokers, knowing that margin rates vary drastically.

4. Margin loans come with the risk of a margin call

If the collateral value falls below a certain level, a margin call can be triggered, requiring additional funds or the sale of securities. Sometimes, your broker will automatically liquidate/sell your holdings to pay off the loan if you fall below a certain level.

The above example emphasises the point that you need to do your research and compare all the different brokers, knowing that margin rates vary drastically.

4. Margin loans come with the risk of a margin call

If the collateral value falls below a certain level, a margin call can be triggered, requiring additional funds or the sale of securities. Sometimes, your broker will automatically liquidate/sell your holdings to pay off the loan if you fall below a certain level.

Margin Lending vs Home Mortgages - Understanding the Difference

Margin lending is distinct from other forms of leverage like home mortgages in several key aspects:

- The asset it’s collateralised against: Mortgages are long-term loans used specifically for purchasing real estate. The property itself serves as collateral for the loan. In contrast, margin lending is primarily used for investing in securities (or for living expenses whilst staying invested in equities), and the share portfolio typically serves as collateral.

- The duration: With mortgages, you're usually signing up for a 20-year or 30-year fixed loan period by which the loan has to be paid back. With margin loans, there is an undefined loan period. You can take out a margin loan and pay it off fully the next day with no early repayment penalties (unlike mortgages, which penalise you for paying off the loan early). In contrast, you could hold the margin loan for 100 years, and as long as you remain within the loan-to-value ratio and have the minimum amount of equity (known as the maintenance margin), you can continue to hold that margin loan.

- The paperwork: Home mortgages often require significant paperwork to set up. In contrast, margin loans usually don't require paperwork once approved to hold a margin account at various brokerage firms.

- The paydown period: With home mortgages, you must follow a fixed paydown period each month or quarter, comprising a portion of principal and interest repayment. With margin loans, you have no fixed schedule to pay the margin loan at certain periods. Margin loans operate more similarly to interest-only loans, whereby interest will accrue on the loan continuously until you decide to pay it back.

- The interest rate: Mortgage interest rates are usually fixed or variable and will be a few percentage points above some benchmark rate. Margin loans are typically always variable rates and can often be lower interest rates than mortgage rates.

- Ability to call back the loan: Mortgages usually have specific provisions that explicitly state when loans can be called back (e.g. they can't randomly be called back without notice). In contrast, margin loans can be called back at any time, and the broker can automatically sell your shares to pay back the loan (especially in periods of extreme volatility).

Alternatives to Margin Lending

For anyone looking to leverage their existing investments and increase equity exposure (e.g. not using margin for lifestyle reasons like paying living expenses or discretionary purchases) without the hassle of margin loan mechanics, there are a few alternatives:

- Derivatives/Options: These are financial instruments whose value is derived from the value of underlying assets, indices, or securities. Derivatives allow investors to gain exposure to the underlying asset without owning it outright. However, Derivatives can usually be quite complex and particularly difficult to deal with.

- Leveraged ETFs (Exchange-Traded Funds): These ETFs use financial derivatives and debt to amplify the returns of an underlying index. They are designed to achieve daily returns multiples of the index performance they track. However, they are generally considered suitable for short-term trading due to their compounding effect on returns and are usually not suitable for long-term investing (due to volatility decay).

- Bank Loans or Personal Loans: Investors may take a conventional loan from a bank or financial institution to finance their investments. Unlike margin loans, these loans are not secured against the investment, so the interest rates might be higher.

- Home Equity Loans: New Zealanders can use the equity in their home as collateral to secure a loan (known as a top-up loan in New Zealand). This can then be used to invest in the shares market or other investment vehicles. The risk here is that if the investment performs poorly, the investor still owes the mortgage or loan, potentially risking their home. They will also likely be paying a higher interest rate on the loan, especially if they already have a mortgage taken out on the property.

The Practical Implications of Margin Lending

Understanding the “Buy Borrow Die” strategy: Wealthy individuals use the "Buy, Borrow, Die" strategy to minimise taxes and preserve wealth. This strategy involves three key components:

- Buy: The first step involves investing in appreciable assets, such as shares, real estate, or other investments likely to increase in value over time. The idea is to buy and hold these assets for a long time, allowing them to appreciate.

- Borrow: Instead of selling their appreciable assets to fund their living expenses, wealthy individuals borrow money, using their appreciable assets as collateral. The advantage of this approach is that loans are not taxable, and the assets don't need to be sold, so they can continue to grow and compound in value. The interest rates on such margin loans are typically low, and the interest expense can sometimes be offset against investment income for tax purposes. This borrowing strategy allows the individual to access the value of their assets without selling them (and potentially triggering capital gains taxes, although this is less relevant in New Zealand except in the context of FIF quick sales and for share traders).

- Die: Upon the individual's death, their heirs inherit the assets (an in New Zealand, there are no capital gains tax and estate taxes, meaning the estate is passed on largely tax-fee).

How can I practically withdraw cash on margin to fund lifestyle purchases? What are the mechanics?

While each process will differ depending on each broker, the typical steps include:

- Depositing money into your brokerage account.

- Upgrading your account to a margin account.

- Invest your money into assets (like ETFs and shares).

- Withdraw a proportion of your assets as cash (e.g. 10% of your portfolio value).

- Use the cash for its intended purpose, such as:

- Purchasing additional shares.

- Paying living expenses such as rent, transportation and food costs without having to sell down assets each month.

- Putting a deposit down on an apartment in Queenstown (or buying it outright if you have a large enough shares account).

- Buying a $10,000 car on TradeMe.

- Pay down the margin loan over time.

What are some examples of people who have funded lifestyle purchases on margin loans?

On the surface, the above sounds extremely high risk and we are absolutely not recommending people overspend and over-leverage themselves to purchase things they don’t need. However, this strategy has been done by “normal” people around the world (e.g. those with modest incomes) and has augmented and improved their lives by having access to margin loans. Some notable people who have used margin loans share their experiences below:

Using margin to buy property:

Using margin to fund living expenses:

Using margin to buy property:

- FIRE vs London: Using IBKR margin loans to buy a home in the UK

- FIRE vs London: Using IBKR margin loans to buy a second property (holiday home) in the UK

- EREVN: Buying a house in Vietnam on margin

- Mr Money Moustache: Buying a $400,000 house on margin

Using margin to fund living expenses:

What are the Different Ways to Act Prudently When Using Margin Loans?

If you decide to take out a margin loan, it's important to have a clear pathway to pay down the loan over time, reduce the loan-to-value ratio (also known as LTV or LVR) and ensure you're not overleveraging your position.

This is usually done through:

By creating a plan to reduce the LTV/LVR and pay down the loan over time, you can mitigate the risk of steep portfolio declines and avoid margin calls.

This is usually done through:

- Consistently pay down the loan over time (either through income gained from a job or otherwise).

- Sell assets or shares periodically to reduce the outstanding loan balance.

- Increase the total portfolio value through share gains (which would reduce the relative size of the margin loan compared to the total portfolio). Nobody can predict what the market will do, so this usually can't be relied upon as a consistent way to reduce the margin loan.

By creating a plan to reduce the LTV/LVR and pay down the loan over time, you can mitigate the risk of steep portfolio declines and avoid margin calls.

Must-Know Facts About Margin Lending

|

Be wary of the tax implications (and potential benefits) when borrowing to investBe mindful of the tax considerations when using margin loans (such as FIF taxes and interest deductibility on margin loan interest costs).

|

|

If you’re considered a trader, there will be tax implicationsIf you’re consistently buying and selling shares, you may be deemed a trader and will be

|

|

Understand FIF taxesIf your cost basis is NZD 50,000 or higher (irrespective of whether that amount is your own money or borrowed from a broker), you will be potentially liable to pay FIF tax (effectively a c. 1.4% wealth tax per year on unrealised capital gains).

|

|

Get Familiar With Margin Interest DeductibilityUse the IRD calculator to figure out if the interest costs associated with borrowing to invest in shares are tax deductible. For example, if:

Then, you can claim the interest you paid on money you borrowed to invest as an expense in your tax return (IR3) under "non-business expense". You'll need to ensure that your investment produces a profit or taxable income. Such as if you earned interest or had dividends paid to you due to your investment. The IRD may ask you for proof of the expenses you would like to claim (such as a report generated on the interest expense you paid on the margin loan). |

|

The more you borrow, the higher the riskThe larger your margin loan relative to your account equity, the less it has to drop before you’re issued a margin call. As such, it’s best to borrow far less than you think you might want, especially if you want to avoid a margin call.

|

|

Brokers can change your margin requirements at any time (and usually at the worst time possible)As assets drop, brokers may get worried you might not be able to repay the initial loan. When this happens, brokers will raise margin requirements (usually at the worst possible times) to ensure they don’t lose money. This can put you in an even tougher position as you will either need to find more money or risk the broker selling your pledged assets.

Some brokerage platforms (like Interactive Brokers) will not issue margin calls but instead start liquidating your positions until your account gets back in line with the minimum margin requirements. |

|

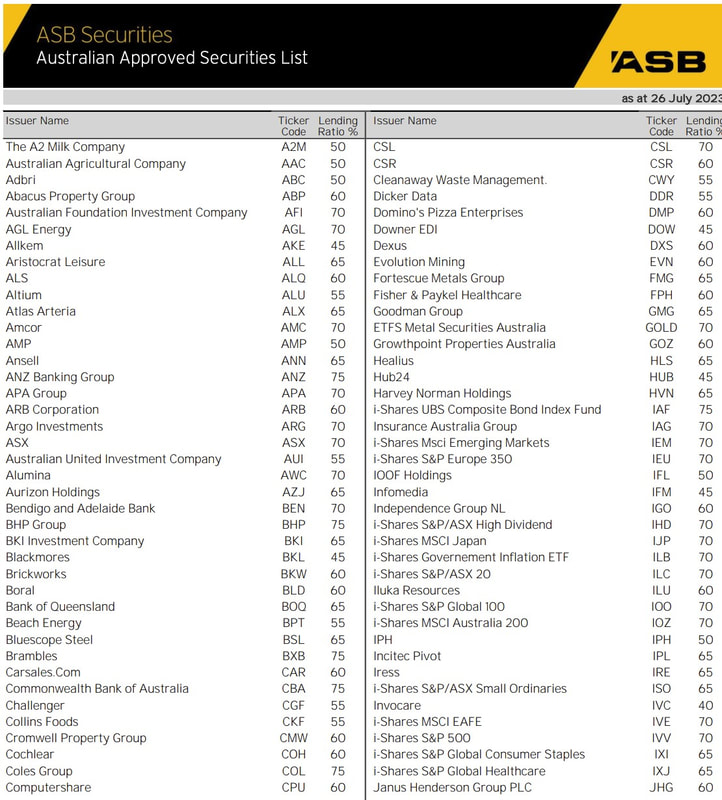

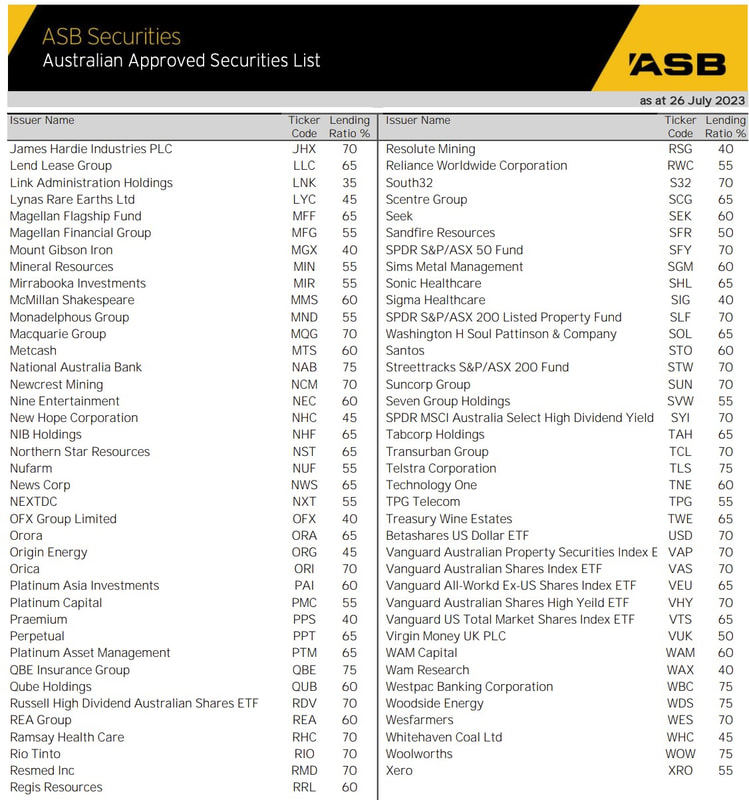

The more volatile the asset, the less likely a brokerage platform is to provide margin lending on itEach broker will have a certain cap on how much they are willing to lend out against (known as the margin requirement or lending ratio). The more risky or volatile the underlying shares you’re pledging, the less likely the broker is willing to lend large amounts.

For example, ASB Securities has the following lending ratios for Australian and New Zealand equities:

Exhibit: ASB Securities Australian Approved Securities List (as of 26 July 2023).

|

|

Investing on margin might be more suitable for younger investors with higher risk tolerancesThe rationale behind using leverage, such as margin lending, when young lies in the concept of 'time in the market' and the potential for higher returns over a long investment horizon. Young investors often have a longer time to recover from potential market downturns and can potentially reap larger returns over time due to the compounding effect. Additionally, younger investors typically have a longer career ahead, which can provide them with more opportunities to earn and save, offsetting the risks associated with leverage.

|

|

The more diversified you are, the less likely margin loans will wipe you outInvestors using margin loans are often advised to diversify their investments to mitigate risk. Also, having a clear strategy for when to enter and exit positions can be crucial in managing the risks associated with leverage.

|

|

Watch out for interest rate changesMargin loan rates are often tied to some floating metric (like the RBNZ OCR or the Fed Funds Rate in IBKR's case). The higher the interest rate on the margin loan, the more expensive it will be to borrow and invest in shares (or borrow to use as a loan to pay living expenses).

|

|

Take margin loans in baby stepsIf you take out a margin loan, do it with a low amount and get familiar with it BEFORE putting large amounts of money at risk. Focus on long-term, stable (less volatile) investments like ETFs. If possible, maintain a larger cash reserve for unforeseen circumstances and try to err on the conservative side when leveraging up, especially with margin loans (that can be called back).

If you’re unclear about margin loans at all, it’s better to borrow far less than you need (or not borrow margin at all). |

|

You may lose more than your initial investment (e.g. you will owe the brokerage or bank)In margin lending, there's a possibility of needing to contribute additional collateral to avoid margin calls. However, brokerages typically liquidate positions to cover the loaned amount, capping potential losses at the initial investment level. In some circumstances, the assets can drop faster than the broker can liquidate, and the liquidation sale proceeds are below the margin balance you owe. This means you'll need to pay the difference to your broker.

|

|

You can’t withdraw more money than you put into your accountFor example - you cannot deposit $100 to ASB Securities and withdraw $110. However, you CAN deposit $100 to ASB securities, invest $100 in NZ shares, and then withdraw $20 as cash (as a margin loan).

|

|

If the cost of borrowing is higher than the expected return, it's probably not worth itThe viability of a margin loan depends on whether the after-tax returns surpass the margin loan interest costs. For example, if you borrow from ASB Securities at a 7% annual interest cost to invest in Air New Zealand shares that only return you 5% a year, it’s likely not worth it for you to borrow to invest.

|

Frequently Asked Questions about Margin Lending

What is a Margin Call?

A margin call occurs when the equity in the margin account falls below the broker's required amount, requiring additional funds or the sale of assets.

Can I Lose More Than My Initial Investment?

Yes, losing more than your initial investment in margin trading is possible. If your portfolio drops quicker than your broker can liquidate, then you will owe the difference to your broker (which will be stipulated in the terms and conditions that you signed when you applied for the margin account).

How is Interest Calculated on Margin Loans?

Interest is typically calculated daily based on the current balance and is charged monthly.

Can you take a margin loan out on cryptocurrency?

While this guide is a starting point for many New Zealanders, some platforms allow margin lending on cryptocurrency (e.g. Binance Loans). However, note the significant risk with borrowing on extremely volatile assets (which cryptocurrency tends to exhibit).

What are the best ways to avoid the downside when using margin loans?

Risk management strategies include:

- Comparing and contrasting different brokers for the best loan terms (e.g. IBKR versus Tiger Brokers).

- Not maxing out LVR limits (e.g. borrowing far less money than you can).

- Periodically paying down your margin loan over time.

- If you need to pay down the margin loan quickly, maintain an emergency cash fund in another account.

- Ensure your pledged portfolio is diversified across many different investments (reducing the likelihood the entire portfolio drops all at once).

What are the minimum amounts needed to access margin lending?

This will depend on the brokerage platform in question. Generally, you'll need a few thousand in a brokerage account to be eligible for margin accounts on brokerage platforms like IBKR or Tiger Brokers.

What are the different names for margin loans?

- Collateralised line of credit

- Pledged Asset Loan (PAL)

- Securities Based Line of Credit (SBLOC)

More Information: Practical Examples from blogs that have written about margin lending:

Relevant Margin Lending News Articles:

- Borrowing to Invest in Property, Shares or Funds

- Fire v London: Using IBKR margin loans to buy a home in the UK

- Fire v London: Using IBKR margin loans to buy a second property (holiday home) in the UK

- Fire v London: Commentary on Margin Loans in the UK

- Jason Debolt: Holding Tesla and using margin loans to pay living expenses (instead of selling shares)

- Mt Money Moustache: Forum post on margin loans

- Indeedably: Margin loan analysis

- Monevator: Alternatives to margin loan

- MoneyBren: Borrowing to invest in Japanese shares

- Chad Jens: Using margin loans to pay living expenses

- Wealthspire: The benefits of margin borrowing

- Johnsoninv: The case for margin borrowing

Relevant Margin Lending News Articles:

- How Larry Ellison Actually Funds His Lavish Lifestyle

- How Elon Musk Dodged a Potential Margin Call Bullet by Following His Own Advice

- Musk's bankers mull new Tesla margin loans to slash Twitter debt - Bloomberg News

- How America’s Richest People Can Access Billions Without Selling Their shares

- Financial Times: How the super-rich buy their homes

- BMO: Why do the wealthy borrow?