Understanding Payment Protection Insurance - The Definitive New Zealand Guide

Our guide explains what PPI is and what it covers, the pros and cons of a policy, costs, what to watch out for, alternatives and frequently asked questions.

Updated 18 July 2024

Summary

To help explain Payment Protection Insurance, our guide covers:

Know This: When you take out a personal loan or car finance, many lenders will offer a PPI (and potentially other insurance policies such as GAP and MBI for cars) alongside the debt. However, the PPI you're offered may not be the most appropriate cover for you. It's also unlikely to offer the best price.

You are not required to take on PPI (or any other insurance) alongside your loan. There may be a strong sales push, but you're not obligated to buy any policy. Your loan offer cannot be withdrawn if you don't buy insurance.

Summary

- If you're taking out a personal loan or car finance and relying on your income to make payments, it's reasonable to worry about what will happen if you can't work or lose your job.

- Payment Protection Insurance (PPI) is a policy that makes repayments for your loan while you cannot work. It covers falling ill, accidents, redundancy and a limited number of other events such as death and terminal illness. In its simplest form, your loan repayments will be made until you recover and earn an income again to take care of the repayments.

- If you claim, payments are not instant - there is a waiting period before the insurer starts paying your loan repayments. This can be as high as 28 days, so your loan will likely become overdue if you don't have any spare money to keep up to date in the meantime. While policies will backdate the payments to the start of the 'claimable event' (for example, being made redundant, being declared bankrupt, business interruption etc.), this can add to an already stressful period.

- PPI usually won't cover any claims relating to pre-existing conditions, any psychiatric or psychological illness (including things like mental stress and/or depression), elective surgery, any back-related condition unless (with some exceptions) and specific other events.

- Despite a relative shortlist of what you're not covered for, there have been many instances of difficulties having claims paid out.

- Our view is that buying add-on insurance makes a car loan more expensive and offers little value for money. As outlined in this December 2022 Stuff.co.nz article, "Financial mentors have been fighting for a ban on car dealers selling high-cost, low-value insurance to unwitting car buyers, claiming it is helping push borrowers into a cycle of debt". This 2020 case highlights the issues of paying PPI and an insurer unfairly rejecting a claim.

To help explain Payment Protection Insurance, our guide covers:

- Why does Payment Protection Insurance Exist and What Does it Cover?

- How Much Does Payment Protection Insurance Cost?

- Payment Protection Insurance – Pros, Cons and Alternatives

- Who offers Payment Protection Insurance?

- Frequently Asked Questions

- Our View and Conclusion

Know This: When you take out a personal loan or car finance, many lenders will offer a PPI (and potentially other insurance policies such as GAP and MBI for cars) alongside the debt. However, the PPI you're offered may not be the most appropriate cover for you. It's also unlikely to offer the best price.

You are not required to take on PPI (or any other insurance) alongside your loan. There may be a strong sales push, but you're not obligated to buy any policy. Your loan offer cannot be withdrawn if you don't buy insurance.

Why does Payment Protection Insurance Exist and What Does it Cover?

Generally, a payment protection policy covers you for loan repayments if you:

There may be other covered events - checking your policy to understand what's included is essential. If you have any questions, contact the insurer - this may not be the company or person who sold you the policy.

How PPI Works: The benefits are payable directly to the lender. "Payment protection" insurance means the insurer makes the loan repayments to your lender until you'll well enough to return to work. Your loan balance won't be paid off in full unless you have a terminal illness or die, or, in extraordinary cases, remain off work for so long that the insurer's repayments clear the balance of the loan.

- Are diagnosed with an illness and can't work

- Have an accident and can't work

- Are made involuntarily redundant

There may be other covered events - checking your policy to understand what's included is essential. If you have any questions, contact the insurer - this may not be the company or person who sold you the policy.

How PPI Works: The benefits are payable directly to the lender. "Payment protection" insurance means the insurer makes the loan repayments to your lender until you'll well enough to return to work. Your loan balance won't be paid off in full unless you have a terminal illness or die, or, in extraordinary cases, remain off work for so long that the insurer's repayments clear the balance of the loan.

Media reports and government research suggest PPI has a lot of traps

- Per this 2018 NZ Herald article, journalist Diana Clement states that at car yards, "too often it's added to the loan automatically via a check box without sufficient questioning to determine if the buyer qualifies. There may be no cover if (policyholders) work part-time, are unemployed or retired".

- Furthermore, Diana writes, "Another nasty sting is that the entire premium is added to the loan upfront rather than monthly. Because the borrower typically doesn't have the money to pay upfront, it's lumped in with the loan and with interest charged on the premium at the same rate as the car or other borrowing".

- Numerous reports have been published of people paying $1,500+ in insurance premiums on $5,000 or $10,000 loans. What's arguably terrible about many of these policies is that any payouts are often for less money than the total cost of the policy - a total ripoff.

The New Zealand Commerce Commission's Motor Vehicle Add-Ons Report Takes a Dim View on PPI

The 2021 NZ Commerce Commission Report was not positive about PPI. It noted a number of problems or limitations:

- Insured events covered vary by policy type and are generally driven by income source (salary/wage, self-employed and those not in full-time employment). So, for example, if you're salary/waged, your cover includes redundancy, whereas those self-employed are covered for bankruptcy. This means you'll need to purchase all of the covers offered by the applicable policy type rather than being able to choose insurance for specific events. If, for example, you just want redundancy cover, you'll also be paying for cover on medical events.

- Pre-existing conditions are the major reason for denied claims - per the 2022 NZ Commerce Commission Report, the most common reason that CCI/PPI claims were declined (equating to 57% of the declined claims) because the event claimed for was a pre-existing condition. This is based on three years of data.

- Cancelling altogether and getting a refund is unclear. If you decide to cancel the policy later on, most insurers won't specify whether or not you'll be refunded outside the standard "cooling off period". This is, in our view, completely unacceptable and at odds with how other insurance (for example, car, house, contents) operate.

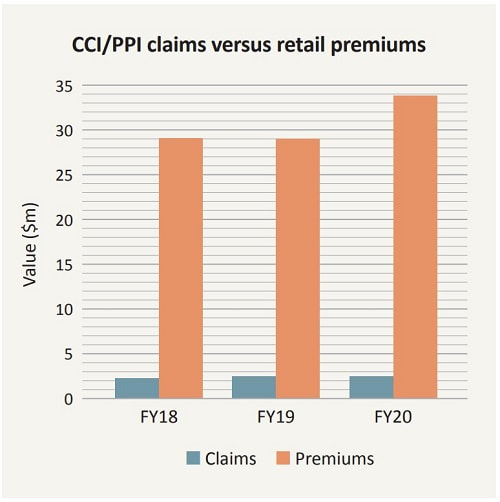

- Policy revenue is significantly greater than what's paid out. Insurance should never be this 'profitable' - the graph below, first published in the report on page 22, shows the difference:

PPI in Australia and the UK has been rife with ripoffs - New Zealand is arguably similar

- A Royal Commission into Banking in Australia found PPI-type policies were such poor value for money that banks and other lenders stopped selling them altogether.

- In the UK, PPI was mis-sold by banks and other lenders for 10+ years before the government stepped in. This Guardian article explains how banks sold millions of PPI policies based on their profitability rather than the suitability to their customer. The result was over £40b (NZ$78 billion) in refund claims.

- Our view: New Zealand hasn't tightened PPI regulation compared to Australia and the UK despite the policies being mostly the same. If you're considering buying a policy, what matters is the total cost, what you're covered for and how much you can claim. Better (and cheaper) PPI alternatives will likely cover your situation - income protection insurance, for example, is something you may want to consider first.

How Much Does Payment Protection Insurance Cost?

What you'll pay depends on many factors. Components that go into any PPI quote include:

If you're given a quote for a PPI policy without being asked these questions, then it's reasonable to be suspicious. The quote may be a 'standard issue' without consideration of your circumstances and risk profile.

Our view: Because PPI isn't openly sold outside of personal loans and car finance, obtaining a range of quotes is near-impossible. You can expect to be quoted around $1,000 for a $5,000 loan. We spoke to a budget advisor who believed "PPI's main function is to impoverish many people, my clients included".

To best avoid expensive policies, we suggest getting a quote for income protection insurance so you can compare the benefits and annual costs to any PPI quote you're offered. Based on the November 2021 research by the Commerce Commission, we believe that any PPI policy and quote will offer much less cover than a similarly priced income protection insurance policy.

- The size of the loan

- How long is the loan term (e.g. 12 months or five years etc.)?

- Your gross annual salary or income

- Your age

- Your job, how many hours you work per week and your employer

If you're given a quote for a PPI policy without being asked these questions, then it's reasonable to be suspicious. The quote may be a 'standard issue' without consideration of your circumstances and risk profile.

Our view: Because PPI isn't openly sold outside of personal loans and car finance, obtaining a range of quotes is near-impossible. You can expect to be quoted around $1,000 for a $5,000 loan. We spoke to a budget advisor who believed "PPI's main function is to impoverish many people, my clients included".

To best avoid expensive policies, we suggest getting a quote for income protection insurance so you can compare the benefits and annual costs to any PPI quote you're offered. Based on the November 2021 research by the Commerce Commission, we believe that any PPI policy and quote will offer much less cover than a similarly priced income protection insurance policy.

Payment Protection Insurance – Pros, Cons and Alternatives

Payment Protection Insurance policies may solve a problem at a cost. This cost can be expensive. We outline what's important when looking at taking out a policy:

Pros

Cons

Be Careful: If you decide to take out a PPI policy from your lender, read the policy documents to know how long it lasts and what's excluded. If you're unsure about anything, please ask the person selling you the policy to explain the answer clearly and get it in writing if you're not convinced. Our view is simple - it's very easy to buy PPI, but claims have a complicated history.

Pros

- Cover: You're covered for specific events should something unfortunate happen (such as involuntary redundancy, developing an illness or having an accident).

Cons

- Cost: With 85% of all insurance sold being taken as profit, it's clear that either the costs are too high or the cover is too limited (or a mix of both). Either way, PPI is usually an expensive policy, and many lenders add to your loan balance, so you'll pay interest on it.

- Uncertainty over the success of claims: Policyholders have a history of complaining about claims being rejected. The policies have been so controversial in Australia and the UK that few providers now sell PPI.

- Unclear as to whether it can be refunded - if your circumstances change or you decide you no longer need the policy, most insurers stay silent about whether you'll be refunded under the cooling-off period.

- Inflexibility: You may want redundancy cover but not medical cover, or vice versa, but PPI is an 'all-inclusive' policy which means you may pay for things you don't need.

Be Careful: If you decide to take out a PPI policy from your lender, read the policy documents to know how long it lasts and what's excluded. If you're unsure about anything, please ask the person selling you the policy to explain the answer clearly and get it in writing if you're not convinced. Our view is simple - it's very easy to buy PPI, but claims have a complicated history.

What are the alternatives to PPI?

Most (if not all) PPI policies are sold alongside personal loans and car finance. PPI will not cover mortgage repayments. Generally, the alternatives to PPI are as follows:

- Income Protection Insurance- Income protection insurance is designed to pay you an income if you cannot go to work for any reason covered by the insurance. With your income paid, you can continue to make loan repayments.

- Sick pay - If you have a job which pays sick leave, you can continue to be paid (and make your loan repayments) until you're well enough or until the sick leave runs out.

- ACC - If the reason you can't work is covered by ACC, you can use ACC payments to pay debts until you return to work. Our guide to Income Protection Insurance vs ACC explains the differences. Remember that 80% of long-term workplace absences are due to illnesses, not injuries. Common illnesses include cancer, significant surgeries, heart issues and depression. An income Protection insurance policy, by comparison, offers to pay up to 75% of your salary for as long as you initially agreed.

- Emergency Fund and Savings - Emergency funds are very difficult to achieve for many New Zealanders. Over 500,000 per this Stuff.co.nz article - have nothing saved. So our view is simple - if you're taking out a loan, it's essential to build up an emergency fund.

What's the difference between PPI and income protection insurance?

Income Protection Insurance and PPI offer income protection and are designed to help you repay certain debts. However, our research has confirmed that while income protection insurance is transparent with policy prices comparable online, PPI is arguably secretive with no online quotes available. In addition, Income Protection Insurance usually covers longer periods (for example, up to 2 or 5 years, or even up to retirement age) and pays a fixed monthly amount. On the other hand, PPI is usually specific to one debt and is shorter-term basis.

Who offers Payment Protection Insurance?

Payment Protection Insurance is mainly sold by many personal lenders and car finance lenders, brokers and car yards (acting as a broker).

Brands behind the policies include (but are not limited to):

Important: None of the above insurers offers online quotes, making it difficult/impossible to compare options.

Brands behind the policies include (but are not limited to):

Important: None of the above insurers offers online quotes, making it difficult/impossible to compare options.

Frequently Asked Questions

Important: If you have any questions before signing up to a PPI policy, you must ask the person selling it to you. Do not sign unless you fully understand the answer to your question. There is no urgency to buy a policy - the lack of clarity about whether you can get refunds should you want to cancel the policy later is alarming. We list common queries below to help you understand more about PPI:

If I'm behind on loan repayments and then get sick or made redundant, will my PPI policy clear the overdue balance?

No. PPI policies won't cover any pre-existing overdue balance or arrears at the time of your claim. They will only pay the repayments while you can't earn an income. So, for example, if you're already $1,000 behind on a car loan and then get made redundant, a PPI policy will cover your repayments while you're out of work, but it won't settle the existing $1,000 overdue.

Is Payment Protection Insurance worth the cost?

We don't think so. The Commerce Commission's November 2021 report and Australian investigations conclude that car dealers, car lenders, personal lenders and insurance companies make lots of money every time someone signs up for PPI. No insurance can be so profitable without there being a cost. We believe the cost is paid by the policyholder who pays too much for the benefit, can't claim, or a mixture of both. The fact that PPI is rarely sold in Australia now suggests how useful and beneficial the policies are.

Can I buy Payment Protection Insurance separately from my loan?

Yes - some insurers offer policies outside of a personal loan or car finance agreement, but this is rare as most policies are initiated by the lender. We believe that PPI is an 'upsell' on typical lending and car finance.

Can I cancel a Payment Protection Insurance later?

If you decide to cancel the policy later on, most insurers won't specify whether or not you'll be refunded outside the standard "cooling off period". This is, in our view, completely unacceptable and at odds with how other insurance (for example, car, house, contents) operate.

Do I pay Payment Protection Insurance upfront or weekly?

You can do both. The policy is usually sold upfront, i.e. $50/month for 6, 12, 24, 36, 48 or 60 months etc. This ongoing cost can be "rolled up" into the personal loan or car loan cost, meaning you'll pay for your PPI policy as you make repayments. Be very careful - when PPI is rolled up into the loan, you'll pay interest on the balance as the money is lent to you.

Payment Protection Insurance - Our View and Conclusion

- We're not fans of PPI and are surprised it's still actively sold in New Zealand. We believe the policies are expensive for what they offer and appreciate the Commerce Commission investigating the practices in its November 2021 report. Worse still, we don't like the sales process. Consumers experience "point-of-sale pressure" which means it's hard to make a complete comparison.

- Having reviewed the nature of the policies and ways PPI is sold, we believe borrowers offered PPI often buy a policy that's not in their interests while offering no cover to pre-existing conditions. Further to this, PPI costs are wrapped up in the cost of a personal loan car finance which makes it hard to understand the cost. Some customers are, arguably, unaware of what they're buying.

- We don't like the fact that many policies, per Commerce Commission research, stay silent on whether a policyholder can be refunded for unused policy later on after the "cooling-off period". Not specifying that is, in our view, very alarming and speaks a lot about PPI policies in general.

- The net effect of PPI is that it makes personal lending and car finance more expensive. The added costs directly harm consumers because adding PPI (or any other add-on insurance) to loan repayments makes the ongoing costs more expensive. Australian investigations found that insurance commissions paid to car dealers could be as high as 79% of the insurance premium. While the Commerce Commission report didn't uncover this, the fact that 85% of premium income becomes profits for insurance companies suggests the policies are expensive.

- We're well aware that many personal lenders and car yards across New Zealand sell PPI alongside their loans. We suggest anyone considering PPI take a look at Income Protection Insurance first so they know what they can be covered for and how much it will cost.

|

Related Guides:

Popular Guides

Car Finance Company Reviews: |