Tips for Seniors Renting or Paying Down a Mortgage – The Definitive New Zealand Guide

Our comprehensive guide demystifies housing choices for those nearing retirement, focusing on critical renting and mortgage management aspects. We cover practical repayment strategies, viable renting alternatives, essential facts, and answers to common questions about retirement living solutions.

Updated 19 July 2024

Introduction and Outline:

Our guide is published to explain everything you need to know should you be facing a mortgage or renting in retirement. We cover:

Important: The 2022 Retirement Commission housing survey of middle-aged New Zealanders sheds light on the living situations of people aged 45-64:

Headline homeownership data from the New Zealand Retirement Commission explains a growing issue:

- As the retirement age approaches for New Zealanders, some unique challenges arise regarding housing, especially for those still renting or with significant mortgage balances. For those who are already retired, an increasing number of New Zealanders are still renting.

- For retirees relying solely on the NZ Super payment, the burden of covering housing costs (either through rent or mortgage payments) is significant. The original premise of NZ Super was based on recipients being mortgage-free homeowners.

- The current reality, however, is markedly different, with declining homeownership rates, a necessity for prolonged working due to outstanding mortgages, ongoing rent obligations, or insufficient retirement savings. This situation leaves a slim amount for essential expenses like food, transportation and other basic needs.

Our guide is published to explain everything you need to know should you be facing a mortgage or renting in retirement. We cover:

- How Common is it to Rent While Close to Retirement?

- What are My Housing Options in Retirement?

- Is it Too Late For Me to Get a Mortgage If I'm Close to Retirement?

- Must-Know Facts about Renting (or Facing a Large Mortgage Balance) as a Senior

- Frequently Asked Questions

Important: The 2022 Retirement Commission housing survey of middle-aged New Zealanders sheds light on the living situations of people aged 45-64:

- Home Ownership: Around 70% of respondents in this age group own or partly own their homes, with a third paying off their mortgage. Inversely, 30% of respondents don't own or partly own their home (e.g. they're renting or are in other alternative accommodation situations).

- Future Retirement Plan Outlook: Half anticipate no change in their living situation post-retirement, but 20% expect improvements, while 16% foresee a decline, mainly due to financial constraints.

- Mortgage Concerns: 15% expect to still have a mortgage after 65. Among these, 23% have debts over $250,000.

- Desired Living Post-65: Two-thirds aim for standalone homes or townhouses, a shift from 81% currently in such homes. 10% of standalone homes plan to downsize.

Headline homeownership data from the New Zealand Retirement Commission explains a growing issue:

- Homeownership rates have significantly decreased over the last three decades, dropping from around 78% in the 1980s to approximately 55% in 2022/2023.

- Among individuals aged 55 to 64, only 38% have paid off their mortgages.

- There has also been a decrease in the number of people over 65 who are mortgage-free, from 78% in 2007 to 72% in 2017.

- Around 12% of those over 65 are either still paying off a mortgage or renting.

Why is renting during retirement increasingly becoming a problem?

- In the recent retirement commission study (2022 RRIP), a primary focus was on the housing sector and its influence on retirement in New Zealand. The research indicated a downward trend in home ownership, primarily due to the unavailability of affordable housing. This trend poses significant challenges for both present and prospective retirees.

- The foundational principle of NZ Super was based on the expectation that New Zealanders would enter retirement owning their homes outright, without any mortgage. However, with this scenario changing and more individuals working longer to clear mortgages or pay rent, NZ Super payments are increasingly being allocated to housing (through rent or mortgage payments).

MoneyHub Founder Christopher Walsh outlines his view of what is happening:"The harsh reality is that many of our seniors are entering retirement with the burden of a mortgage or the instability of renting. This starkly contrasts NZ Super's original vision, which assumed retirees would be mortgage-free homeowners.

The declining homeownership rates (outlined in graphs below) and the increasing necessity to work beyond retirement age due to mortgages and rent obligations are alarming trends. Seniors now find a significant portion of their NZ Super going towards rent or mortgages. This leaves little room for other essential expenses, marking a worrisome shift from previous generations. It's encouraging to see an increasing number of seniors actively planning their retirement, considering options like downsizing or moving into retirement villages, which can provide financial relief and a supportive community. This guide is the first of its kind - we want anyone planning the future to be fully informed and consider their options. If you have any comments or suggestions, please contact our research team - we want this guide to be as helpful and comprehensive as possible". |

Christopher Walsh

MoneyHub Founder |

How Common is it to Rent While Close to Retirement?

According to the Retirement Commission, a recent report predicts a sharp rise in New Zealand retirees who will need to rent in the coming 25 years, prompting calls for a re-evaluation of housing support for older citizens. Following a survey on the housing status of older New Zealanders, a third of New Zealanders aged 55 to 64 do not own homes, and this issue extends to 20% of those over 65. This historical comparison of home ownership has more information.

A comparison over the past three decades shows significant shifts in housing patterns:

A comparison over the past three decades shows significant shifts in housing patterns:

- In 1986, 87% of individuals in their 60s owned their homes mortgage-free and were largely unemployed.

- By 2018, 80% of those in their early 60s were homeowners, yet 20% were still repaying mortgages, another 20% were renting, and many continued to work. The costs of mortgages and rents have escalated faster than outright ownership.

- Projected trends indicate a doubling in renters aged 65 and over.

- Long-term projections suggest a shift towards 60% homeownership and 40% renting by 2048. This 40% will represent around 600,000 New Zealanders per the Retirement Commission's study.

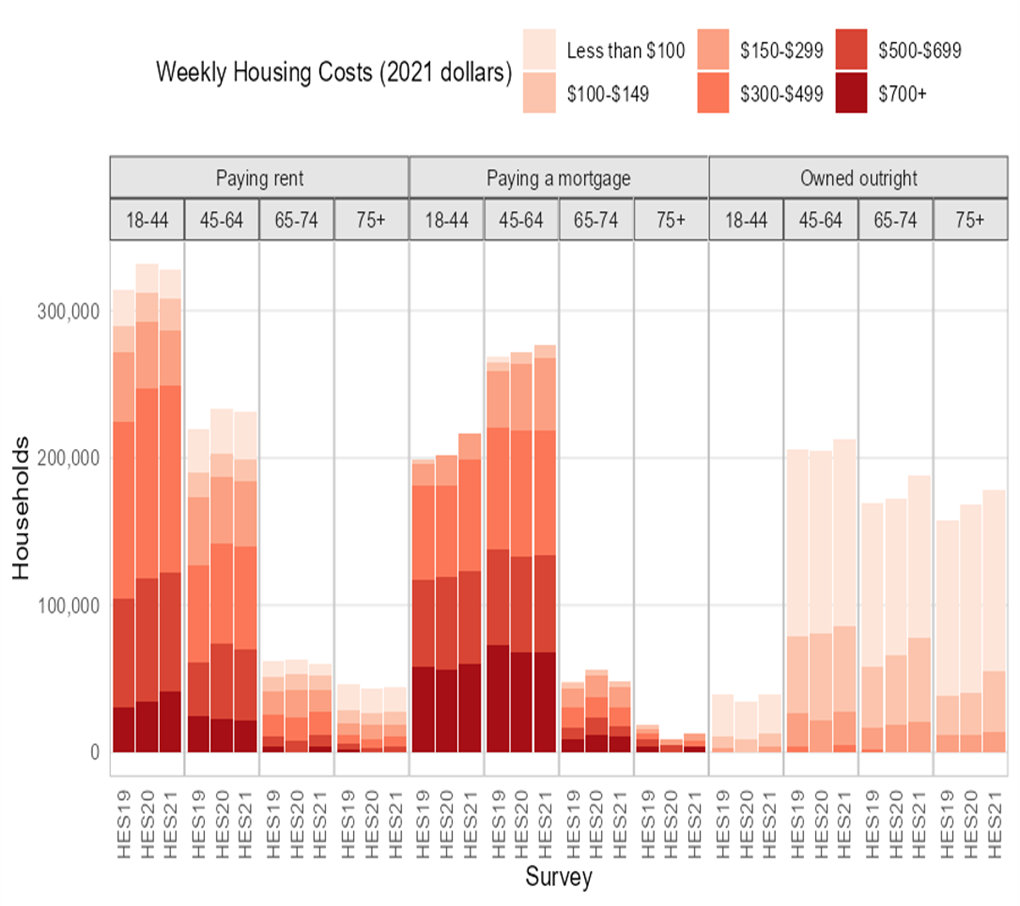

- Per the graph below, 66% of all senior households own their homes outright and 13% are paying a mortgage (with the remaining 21% paying rent).

Exhibit: Breakdown of Senior New Zealanders' Housing Costs (Own Outright versus Mortgage versus Rent - Retirement Commission 2022)

Is NZ Super enough to cover living costs as well as rent or mortgage payments?

NZ Super rates are relatively tight, even for New Zealanders who own homes. The situation is even more challenging for those still paying mortgages in retirement.

Based on a study conducted by The Treasury that analysed New Zealand’s housing costs across different age demographics, a few insights were generated:

Based on a study conducted by The Treasury that analysed New Zealand’s housing costs across different age demographics, a few insights were generated:

- Superannuitants who are renters often spend 40% or more of their NZ Super income on housing. Future trends indicate a rise in the number of older individuals renting.

- About 80% of them allocate more than 40% of their NZ Super towards housing costs, with over half spending more than 80% of their NZ Super on these expenses.

- This starkly contrasts with outright homeowners, where approximately 80% spend less than 40% of their NZ Super on housing, and more than half use less than 20%.

- For 40% of those aged 65 and over, NZ Super is their sole income source, with an additional 20% having only a modest additional income.

- The Retirement Commission RRIP 2022's projected housing stages through the ages illustration is useful to help understand what's going on.

What happens if I hit retirement and I still have a mortgage?

- Nearly 1 in 5 New Zealand retirees still manage a mortgage into retirement per this August 2022 Stuff.co.nz story. While the banks try as hard as possible to ensure that most New Zealanders have paid off their mortgage by the time they hit retirement age, some still hold mortgage balances into retirement. Relying solely on NZ Super to cover mortgage and living costs is challenging given the current payout rates, especially with relatively high mortgage interest rates.

- As such, many New Zealanders delay retirement to continue working/earning and paying off their mortgage. This increase in New Zealanders continuing to work past 65 (the age of eligibility for NZ Superannuation) is partially out of choice/interest but increasingly out of necessity.

- If you retire (age 65+) and are still owing on your mortgage, even after depleting KiwiSaver funds, some tough decisions are necessary and will heavily depend on whether you've still got a job or have been out of the workforce for a while.

- While it's not ideal, it's common for older New Zealanders to struggle to find work of the same duration (full-time) or compensation (salary) that they were able to when they were at the peak of their careers (40s and 50s). As such, we will assume you aren't able or want to continue working full-time after you've retired (although this is possible, and some New Zealanders do this).

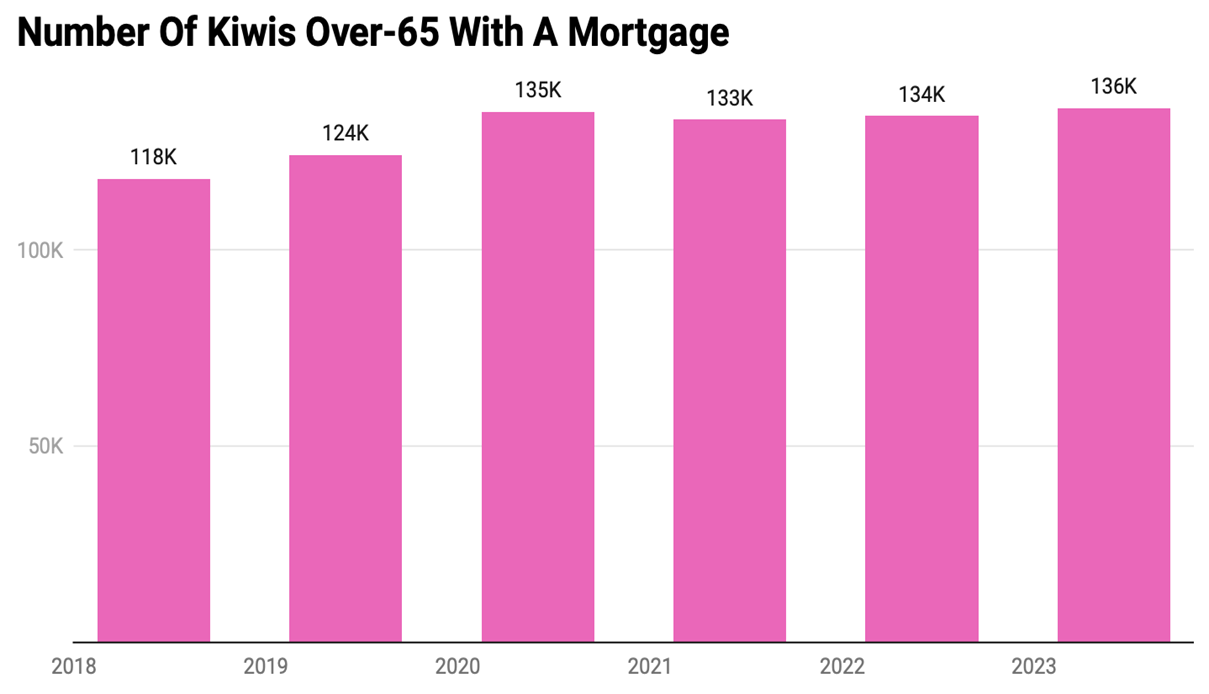

- The graph below, sourced from OneRoof, shows that 136,000 New Zealanders over 65 still have a mortgage.

What are My Housing Options in Retirement?

As New Zealanders approach retirement, there are a few main options for those who may not own their home outright or who are still renting:

1. Continue to rent

2. Move into a retirement village

3. Downsize (if you own a home with a mortgage)

4. Move into community (social) housing

5. Move in with your kids

1. Continue to rent

- Renting remains a viable option for seniors who appreciate its flexibility and freedom. Renting a home allows you to move with relative ease, making it a suitable choice for those who want to be close to family members, downsize, or explore different locations.

- However, as New Zealanders age, they may not have the desire or flexibility to consistently move between rentals (especially since 12 months is the norm). Moving every year would likely be a pain for New Zealanderretirees, and there's no guarantee that the new rental you move into will meet the accessibility requirements you may need in old age.

2. Move into a retirement village

- Retirement villages are purpose-built communities designed to cater to the needs of seniors. These communities often offer a range of accommodation options, from independent living units to serviced apartments and care facilities. Retirement villages typically provide various amenities and services, such as communal spaces, social activities, and healthcare services. This housing option is ideal for those seeking a supportive and social environment with access to care as needed.

- While there are many benefits to moving into a retirement village, and the weekly/ongoing costs are typically lower than paying rent, they require a significant upfront cost (known as buying a licence to occupy). Our guides to retirement villages and retirement in a nutshell have more information.

3. Downsize (if you own a home with a mortgage)

- As New Zealanders age and you become less active, some homes become less ideal for you. The rural five-bedroom lifestyle block you might have lived in with your kids when you were 50 was perfect for you then, but it may not be ideal for you now when your kids may have left to work abroad, and you'd much rather live closer to the shops or city.

- The fastest way to pay off your mortgage with little effort on your part is to downsize - whether that's selling your property and buying one with fewer bedrooms or less space or relocating to a more affordable area, the differential in the value of your old home and your new home can be used to pay off the mortgage.

- In some circumstances, you’ll be able to sell your current property, buy a new property and pay off the mortgage entirely - enabling you to live mortgage-free, as well as having a sum of cash on hand.

- As a practical example, you may own a $1.6m million five-bedroom property in central Auckland with a $500,000 mortgage. It's just you and your partner; your kids have left home (or you don't have kids), and you likely have much more space than you need. You decide to sell your property and it sells for $1.5 million net of agent fees. You then pay off the $500,000 mortgage in full and buy a $750,000 apartment on the North Shore of Auckland. In this example, you've paid off the mortgage and moved into a place that's much more suitable to your post-retirement lifestyle, and have cash of $250,000 to use in retirement.

- Downsizing options include moving into an apartment or a granny flat (A granny flat or secondary dwelling is a self-contained living space on the same property as the primary residence).

4. Move into community (social) housing

- Community housing refers to affordable rental properties managed by non-profit organisations or the New Zealand Government. These properties are intended for those struggling to afford private rental accommodation. Seniors on a fixed income might find community housing an affordable option that meets their needs (but know that there are strict eligibility criteria, including income and cash asset caps, to be considered for social housing).

5. Move in with your kids

- While it might seem odd, moving in with your children is much more common (particularly in Asian or Indian cultures). In some cases, moving in with your adult children can greatly benefit you and your kids.

- If you can move in with your kids, you can potentially rent your property to pay down the mortgage or sell the property and free up the equity to reinvest. For your kids, having parents living in the same household (multigenerational living arrangements) can significantly help to take care of the household chores or babysitting (if your kids have young children). Alternative arrangements can include older generations living with their kids and gradually transferring home ownership to their children as they age.

What are other ways to pay down a mortgage in retirement above and beyond downsizing?

If you've still got a sizeable mortgage at retirement age and are not working full-time, here are some other alternative or unorthodox ways to approach your mortgage:

- Work a side hustle in retirement: Whether it's renting out a room in your property, driving for Uber or picking up part-time or casual work, working a side hustle in retirement can provide additional income that, combined with NZ Super payments, might make it possible for you to continue supporting yourself and pay off the mortgage.

- Sell non-housing assets: Selling high-value personal assets (think things like a car, jewellery, shares, funds, gold, etc.) on places like Trade Me can help to free up some cash and pay down the mortgage, especially if there's not a large amount of debt remaining.

- Postpone property rates: Some regions, like Auckland, offer over-65s the option to defer property rates until death or sale of the home, acting as a form of equity release mortgage.

- Apply for the Accommodation Supplement: The Accommodation Supplement is available for some retirees with mortgages, but note that it is means-tested and may make most retirees ineligible (especially those who've built up significant equity in their properties).

Is it Too Late For Me to Get a Mortgage If I'm Close to Retirement?

Securing a home loan later in life can involve additional complexities in the approval process. Given that home loans often span up to 25-30 years, New Zealanders beyond a certain age might struggle to settle their mortgage before retiring.

However, some lenders accommodate clients nearing or have entered retirement, even if the loan period surpasses their retirement age. Lenders are obliged to ensure borrowers can feasibly repay their loans over time. Consequently, older applicants may encounter more challenges in securing loan approval given the difficulties of servicing a mortgage as you get older.

Age Limits for Home Loan Approval:

Important: You can't rely on NZ Super to meet your mortgage payments. The most common plan to pay back the mortgage when nearing retirement age is to pay off the entire loan outright with additional cash. Common exit strategies include:

Banks will assess your exit strategies based on your age, financial status, income, retirement plans, and ability to demonstrate loan repayment capability. If doubts arise regarding repayment feasibility, they may not approve your mortgage.

Unsuitable Exit Strategies

Lenders must ensure loans don't lead to significant financial stress for borrowers. Certain exit strategies might be deemed unreliable, such as:

Know This: Some lenders might approve loans with these strategies if there's substantial evidence of future financial resources. However, the majority of the above are speculative or highly volatile and won't be able to be relied upon in the mortgage application.

Our general estimate of applying for home loans by age:

Lender policies on retirement age vary, but some common age-related guidelines from banks include:

However, some lenders accommodate clients nearing or have entered retirement, even if the loan period surpasses their retirement age. Lenders are obliged to ensure borrowers can feasibly repay their loans over time. Consequently, older applicants may encounter more challenges in securing loan approval given the difficulties of servicing a mortgage as you get older.

Age Limits for Home Loan Approval:

- While age discrimination is prohibited among lenders, applicants must still fulfil standard lending criteria based on their ability to repay loans consistently. Proving the capacity to repay the loan might require additional persuasion for those nearing retirement.

- Approval for home loans becomes more difficult for individuals aged 65 and above, but it's not unattainable. Regardless of age, a lender will evaluate an application based on financial stability and the ability to pay back the loan.

- If the loan extends past retirement, lenders will want to understand how you intend to repay it. This is known as an "exit strategy" and should outline how you plan to manage the loan repayment after retirement, avoiding financial strain.

Important: You can't rely on NZ Super to meet your mortgage payments. The most common plan to pay back the mortgage when nearing retirement age is to pay off the entire loan outright with additional cash. Common exit strategies include:

- Selling and downsizing to a smaller home (and using the difference to pay the mortgage)

- Liquidating assets like shares and funds

- Relying on ongoing income from NZ Super for everyday bills

- Make a lump sum payment from when your KiwiSaver is paid out post-retirement

Banks will assess your exit strategies based on your age, financial status, income, retirement plans, and ability to demonstrate loan repayment capability. If doubts arise regarding repayment feasibility, they may not approve your mortgage.

Unsuitable Exit Strategies

Lenders must ensure loans don't lead to significant financial stress for borrowers. Certain exit strategies might be deemed unreliable, such as:

- Expected inheritance (after all, you can’t know for certain when your parents might pass away)

- Projected income or KiwiSaver balances (especially given the markets can be very volatile)

- Pending family law settlements (where the outcomes are unclear, and the payouts may never come through)

- Anticipated bonus payments or salary increases (given their uncertainty)

- Business sale proceeds

Know This: Some lenders might approve loans with these strategies if there's substantial evidence of future financial resources. However, the majority of the above are speculative or highly volatile and won't be able to be relied upon in the mortgage application.

Our general estimate of applying for home loans by age:

Lender policies on retirement age vary, but some common age-related guidelines from banks include:

- Thirties: Professional career and expected retirement age are evaluated. Usually, New Zealanders in their thirties will have little to no problems related to age, given they’ll likely have 30 years of working life left, and the ability to pay off their mortgage is reasonable. Lenders are unlikely to require an exit strategy.

- Fourties: As there are at least twenty years of working life left, applicants might need to present additional information related to an exit strategy for post-retirement loan repayment (if the bank anticipates you'll still have a mortgage when you retire based on the loan repayment schedule).

- Fifties: Because you’ve likely got less than 20 years before you hit retirement age, nearly all lenders will request a detailed exit strategy and evidence of financial resources for debt repayment.

- Sixties: Banks are likely to reject applications due to age, given there is a significantly shorter working window (<10 years) before you hit retirement age and are unlikely to be able to meet 20 or 30-year mortgage repayment schedules. However, in unique circumstances, if you can prove ongoing income or asset liquidation, you might still be able to get approved. But generally speaking, most New Zealanders in their 60s will either not want to continue working past 65, struggle to find work or not have the assets to pay off their remaining mortgage balance when they stop work).

Must-Know Facts about Renting (or Facing a Large Mortgage Balance) as a Senior

1. Employment has its benefits, especially as people remain healthier into older age

- While it’s culturally accepted that most New Zealanders stop working in retirement, that doesn’t have to be the case for everyone. Work usually provides a sense of purpose and connection to the wider community and doesn’t need to stop just because you hit an arbitrary age. Many New Zealanders find a sense of meaning from the work they do, and continue to work well past retirement age.

- However, those who choose to work after 65 need to be mindful of the tax implications of working alongside receiving NZ Super.

2. You'll need a plan to avoid common issues in retirement

If you’re near retirement, it can be really helpful to plan out and ensure you avoid common pitfalls that people run into when they hit retirement age. A few good goals to provide peace of mind include:

- Aim to clear all debts before retiring (such as a mortgage, high interest credit cards, personal loans, car loans etc.)

- Identifying a target date when you want to reduce work hours or resign and stop work entirely (or alternatively, if you want to continue working, and delay retirement to pay off more of your debts and accumulate more wealth, figure out when that retirement point will be).

- Identify potential ways to generate additional income without relying on employment (such as interest from term deposits, dividends from shares, etc.).

3. If you’re finding a lot of resistance with banks, try going through a mortgage broker

If you want to buy a home, there are issues as you age. If you’re running into trouble with traditional bank applications and you suspect the reason is partially to do with age, going through a mortgage broker might help to improve your odds of getting a loan approved. Generally, mortgage brokers:

- Can get better rates than the standard or carded rates available to the public.

- Can negotiate on your behalf and will save you time going back and forth with the bank.

- Might be able to get approvals or find options that you wouldn't have thought to pursue (due to their reputation or their ability to shop around other banks).

Frequently Asked Questions

Can I use my KiwiSaver funds to buy a home when I'm close to retirement age?

Yes, there’s no age limit when using KiwiSaver to buy a home. You can use your KiwiSaver funds to purchase a home if you meet certain eligibility criteria, such as being a first-time homebuyer or having been in KiwiSaver for at least three years.

However, you should consider whether using your KiwiSaver funds for a home purchase is the best option, as it may impact your retirement savings. The KiwiSaver money you withdraw for a house deposit will be taken away from the money you can cash out for retirement when you hit 65.

However, you should consider whether using your KiwiSaver funds for a home purchase is the best option, as it may impact your retirement savings. The KiwiSaver money you withdraw for a house deposit will be taken away from the money you can cash out for retirement when you hit 65.

What should I look for in a rental property as an older New Zealander?

The older you get, the more your needs change. You're unlikely to need a massive Olympic-sized swimming pool in your 70s, and you might find you need far less space than you used to (especially if it's just you or your spouse).

Generally, senior New Zealanders find that low-maintenance properties with easy access to public transport are close to essential amenities like supermarkets or hospitals and are single-level (e.g., you don't have to climb stairs to the bathroom every night) ideal. You may also want to prioritise properties with accessibility features, such as handrails or ramps, especially as you get deeper into retirement (think 80+ years of age).

Generally, senior New Zealanders find that low-maintenance properties with easy access to public transport are close to essential amenities like supermarkets or hospitals and are single-level (e.g., you don't have to climb stairs to the bathroom every night) ideal. You may also want to prioritise properties with accessibility features, such as handrails or ramps, especially as you get deeper into retirement (think 80+ years of age).

How can I ensure I have enough income to cover my housing costs during retirement?

If you're not yet retired and want to ensure the finances will work out in retirement, consider creating a retirement plan. Retirement plans typically involve tallying up all the relevant income streams (such as NZ Super payments, part-time income, potential rental income or dividends from shares) and subtracting your relevant expenses (like food, housing/mortgage payments, rates and insurance).

If you find that you've got a "shortfall" (e.g. the projected retirement expenses are higher than the income), you'll need to find a way to plug that gap (either through savings you've accumulated, selling down assets or a reverse mortgage (if you own a home and have built up equity, and are comfortable with this arguably wealth-eroding product).

If you find that you've got a "shortfall" (e.g. the projected retirement expenses are higher than the income), you'll need to find a way to plug that gap (either through savings you've accumulated, selling down assets or a reverse mortgage (if you own a home and have built up equity, and are comfortable with this arguably wealth-eroding product).

I'm applying for a mortgage with my partner, but there's a significant age gap (e.g. I'm 55 and they're 40). How will banks look at the mortgage application?

When couples apply jointly, lenders may base the need for an exit strategy on the age of the younger or older partner. For example, if one of you is nearing retirement age and they are the main source of household income, the bank will assume this person will retire earlier than the other (meaning their ability to pay the mortgage will be significantly diminished after they stop work). As such, banks may require an exit strategy for your application, given the proximity of one of your retirements.

Older applicants can enhance their loan approval chances by:

Older applicants can enhance their loan approval chances by:

- Opting for a shorter loan duration to ensure repayment before retirement (such as a 20-year mortgage rather than 30 years).

- Presenting a robust exit strategy for loans extending beyond retirement.

- Applying to multiple lenders or working with a mortgage broker to find the bank with the most lenient lending to older New Zealanders.

Do I need to own a house by the time I hit retirement age?

No, you don’t. Buying a house is a deeply personal choice. A significant portion of New Zealanders still rent near retirement age.

Is it bad to still be renting near retirement age?

While it's more common than not to be living in a home that you partially or fully, there are no inherent downsides to renting near retirement age. The biggest consideration for renting versus owning is down to personal preferences. Assuming you have sufficient savings or investments that are growing, renting people can be in a stable or even better position than people who own a home and are paying down high mortgage balances/rates.

Should I take out a mortgage and buy a home when I only have a decade of income-earning years left?

It depends. You might not have to choose at all, given that banks may not be willing to lend to applicants with < 10 years of income earning years left. Whether you get approved for a mortgage depends heavily on your current financial position (assets and debts), what kind of property you want to buy and your current lifestyle.

Ultimately, there's no harm in applying for a mortgage, but the older you get, the harsher the banks may treat your application. A bigger question will be whether you think it's appropriate or makes sense for your lifestyle to be taking out large sums of debt close to retirement.

Ultimately, there's no harm in applying for a mortgage, but the older you get, the harsher the banks may treat your application. A bigger question will be whether you think it's appropriate or makes sense for your lifestyle to be taking out large sums of debt close to retirement.

External Government Reports:

Other Relevant Guides:

- Housing Tenure by Age, Cost, Ethnicity, and Time

- Housing Intentions for People Living in New Zealand Aged 45-64

- Retirement Income Policy Review 2022

Other Relevant Guides: