Compare the Best PIE Term Deposit Rates

If you're on the 30%, 33% or 39% marginal tax rate, PIE term deposits cap the tax you'll pay on the interest you earn at 28%. MoneyHub publishes the top deals available right now from trusted banks, as well as tips and FAQs.

Updated 20 July 2024

Summary

Summary

- As wages in New Zealand rise, more people are finding themselves in higher marginal tax brackets. When interest rates also increase, a higher marginal tax rate means that more of the interest earned on savings is taxed (as a proportion).

- PIE term deposits offer a solution - they cap the tax rate at 28% for interest earned, allowing you to keep more.

- Without PIE investments, high-income earners pay a higher proportion of tax on their term deposit earnings compared to low-income earners.

- This guide provides information on the best PIE term deposit deals currently available, along with tips and FAQs to help you maximize your savings.

- Keep in mind that banks possess varying credit ratings, which serve as indicators of the safety of your term deposit. For more information, refer to our comprehensive Bank Credit Ratings guide.

Our guide covers:

Want to see the pre-tax returns of a term deposit? Visit our Term Deposit Calculator

- Top PIE Term Deposit Interest Rates for up to 12 Months

- Top PIE Term Deposit Interest Rates for 18 Months to 5 Years

- Frequently Asked Questions

- Must-Know Facts and Tips

- PIE Term Deposit Pros and Cons

Want to see the pre-tax returns of a term deposit? Visit our Term Deposit Calculator

Know This: PIE Term Deposit vs Term Deposits on $10,000, $50,000 and $250,000 investments earning 5.00% for 12 months

- The table below illustrates how people in higher tax brackets, with a marginal tax rate of 30% or more, pay more tax on term deposit earnings than those in the lower PAYE tax brackets of 10.50% or 17.50%.

- However, it's important to note that PIE term deposit interest rates are typically lower than standard term deposit rates, as banks price their offers with the tax benefits of PIEs for higher earners in mind.

- Additionally, the table assumes that the 5.00% p.a. interest rate is compounded at maturity (e.g. after 12 months), while many PIE and standard term deposits pay interest quarterly or more frequently.

Investment Option |

Interest Earned After Tax on a $10,000 Investment (at 5% p.a for 12 months) |

Interest Earned After Tax on a $50,000 Investment (at 5% p.a for 12 months) |

Interest Earned After Tax on a $250,000 Investment (at 5% p.a for 12 months) |

PIE Term Deposit (28% PIE Tax Rate) |

$362 |

$1,804 |

$9,023 |

Term Deposit (30% Income Tax Rate) |

$351 |

$1,752 |

$8,770 |

Term Deposit (33% Income Tax Rate) |

$336 |

$1,679 |

$8,397 |

Term Deposit (39% Income Tax Rate) |

$307 |

$1,529 |

$7,644 |

Converting PIE Term Deposit Rates to Effective Returns (also known as Equivalent Gross Term Deposit Returns) to Compare Like for Like

You'll often see a PIE term deposit alongside 'effective returns' or something similar for the 30%, 33% and 39% tax rates. It's a point of confusion for many investors so we explain how these figures are calculated so you can compare with accuracy.

To convert a PIE term deposit rate to a normal term deposit interest rate to compare them side-by-side, you need to consider the different tax rates which are based on your taxable income. For example, if your taxable income is between $48,001 and $70,000, your tax rate is 30%, whereas you'll pay 33% if you earn between $70,001 to $180,000 and 39% on anything above $180,000.

To convert a PIE term deposit rate to a normal term deposit interest rate to compare them side-by-side, you need to consider the different tax rates which are based on your taxable income. For example, if your taxable income is between $48,001 and $70,000, your tax rate is 30%, whereas you'll pay 33% if you earn between $70,001 to $180,000 and 39% on anything above $180,000.

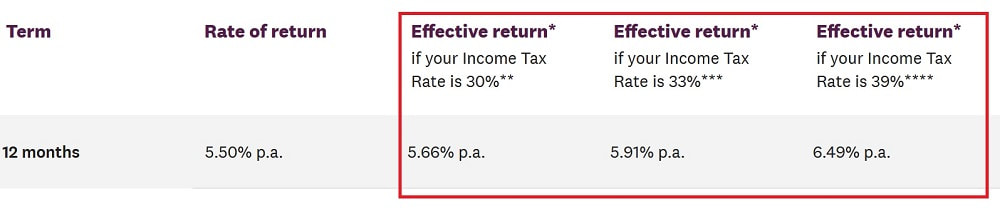

A historical example from Westpac showing a 5.50% PIE Term Deposit with 'Effective returns' also known as 'Equivalent Gross Term Deposit Returns'

Using the Westpac example above, to calculate the equivalent gross return for a 30%, 33%, and 39% taxpayer for a PIE term deposit with an advertised rate of 5.50% p.a. for 12 months, we follow a simple process using two factors:

To confirm, the equivalent gross return for a 30% taxpayer is approximately 5.66%, for a 33% taxpayer is approximately 5.91%, and for a 39% taxpayer is approximately 6.49%. This matches the Westpac calculations above.

- Advertised Rate % p.a. = 5.50%

- PIE tax rate = 28%

- First, calculate the return after the PIE tax: After-tax return = Advertised Rate X (1 - PIE tax rate) = 5.50% X (1 - 0.28) = 5.50% X 0.72 = 3.96%

- For a 30% taxpayer, the equivalent gross return = After-tax return / (1 - 0.30) = 3.96% / 0.70 = 5.66%

- For a 33% taxpayer: Equivalent gross return = After-tax return / (1 - 0.33) = 3.96% / 0.67 = 5.91%

- For a 39% taxpayer: Equivalent gross return = After-tax return / (1 - 0.39) = 3.96% / 0.61 = 6.49%

To confirm, the equivalent gross return for a 30% taxpayer is approximately 5.66%, for a 33% taxpayer is approximately 5.91%, and for a 39% taxpayer is approximately 6.49%. This matches the Westpac calculations above.

Advertised PIE Term Deposit Interest Rates vs Equivalent Gross Return (for 30%, 33% and 39% taxpayers)

The table below shows a PIE term deposit's true interest earning rate for higher-bracket taxpayers. We assume for the calculations that all interest is paid on maturity (e.g. when the term deposit ends). If interest is paid more frequently, e.g. quarterly or monthly, the effective interest rate increases because your interest earnings start compounding.

Advertised PIE Term Deposit Interest Rate |

Equivalent Gross Return (30% tax payer) |

Equivalent Gross Return (33% tax payer) |

Equivalent Gross Return (39% tax payer) |

3% p.a |

3.09% |

3.22% |

3.54% |

4% p.a |

4.11% |

4.30 |

4.72% |

5% p.a |

5.14% |

5.37% |

5.90% |

6% p.a |

6.17% |

6.45% |

7.08% |

7% p.a |

7.20% |

7.52% |

8.26% |

8% p.a |

8.22% |

8.60% |

9.44% |

What is a PIE term deposit, and how does it differ from a normal term deposit?

A PIE (Portfolio Investment Entity) term deposit is an investment several New Zealand banks offer. It's a fixed-term investment with a guaranteed return at a fixed interest rate. The main advantage of a PIE term deposit is that it allows you to pay tax on your earnings at a lower rate (capped at 28%), making it a tax-efficient investment option for higher earners.

A PIE term deposit is a type of term deposit that is taxed differently from a regular term deposit. With a regular term deposit, the interest you earn is subject to your marginal tax rate, which can be as high as 39%. With a PIE term deposit, your earnings are taxed at a maximum rate of 28%. This can make PIE term deposits a more attractive option for higher earners.

It's important to note that PIE term deposits function similarly to regular term deposits, with fixed interest rates and penalties for early withdrawal. However, the tax benefits of PIEs can make them a more attractive investment option for higher earners.

A PIE term deposit is a type of term deposit that is taxed differently from a regular term deposit. With a regular term deposit, the interest you earn is subject to your marginal tax rate, which can be as high as 39%. With a PIE term deposit, your earnings are taxed at a maximum rate of 28%. This can make PIE term deposits a more attractive option for higher earners.

It's important to note that PIE term deposits function similarly to regular term deposits, with fixed interest rates and penalties for early withdrawal. However, the tax benefits of PIEs can make them a more attractive investment option for higher earners.

How is the interest rate for a PIE term deposit determined?

The interest rate for a PIE term deposit is typically based on the length of the term, the amount of money you invest, and prevailing market conditions. Banks may offer different interest rates for different term lengths and investment amounts, so shopping around is important to find the best deal.

How is the interest paid on a PIE term deposit?

The interest on a PIE term deposit can be paid at different times, depending on the bank's policies. For example, some banks may pay interest at maturity (i.e., at the end of the term), while others may pay interest quarterly, annually, or monthly. Some banks may also offer the option to compound your interest's interest, which means you earn interest on the interest you have already earned.

How is tax paid on PIE term deposit earnings?

With a PIE term deposit, the bank deducts tax on your earnings at source, and the remaining interest is paid to you. The amount of tax deducted depends on your Prescribed Investor Rate (PIR), which is based on your income and tax rate. The highest PIR under a PIE is 28%. If you're unsure what your PIR is, you can use the IRD's online tool to find out.

Warning - Investment Scams

- We are aware New Zealanders are being targeted by scammers hoping to get their hands on money otherwise destined for legitimate term deposits. This term deposit scam featured on Fair Go in March 2023 is one of many examples.

- We believe the scams start as adverts on third-party websites (e.g. not MoneyHub) and entice people to enter their contact details. Then, phone calls are made to lure the money to fake New Zealand and/or overseas-based companies promising returns above those you'll receive from term deposits.

- MoneyHub Founder Christopher Walsh explains this problem in a video that lists what you can do to avoid scams altogether.

- Remember, if it sounds too good to be true, or you have a funny feeling or anything else, do not proceed. There are too many scams out there to risk it, as you'll see in the video:

Top PIE Term Deposits Available Right Now

Investment Term: 1 to 12 months

|

Heartland Bank - 6.00% p.a. for 12 monthsInterest Rate: 6.00% p.a.

Term: 12 months Interest payment: Every three months Minimum deposit: $1,000 How to open: Apply via Heartland's website Want to see the pre-tax returns of a PIE term deposit? Visit our Term Deposit Calculator |

|

BNZ - 5.80% p.a. for 12 monthsInterest Rate: 5.80% p.a.

Term: 12 months Interest payment: Monthly Minimum deposit: $2,000 How to open: Apply via BNZ's website Want to see the pre-tax returns of a term deposit? Visit our Term Deposit Calculator |

|

Kiwibank- 5.80% p.a. for 12 monthsInterest Rate: 5.80% p.a.

Term: 12 months Interest payment: At maturity Minimum deposit: $10,000 How to open: Apply via Kiwibank's website Want to see the pre-tax returns of a term deposit? Visit our Term Deposit Calculator |

|

Westpac - 5.80% p.a. for 12 monthsInterest Rate: 5.80% p.a.

Term: 12 months Interest payment: Monthly Minimum deposit: $5,000 How to open: Apply via Westpac's website Want to see the pre-tax returns of a term deposit? Visit our Term Deposit Calculator |

|

ANZ - 5.70% p.a. for 12 monthsInterest Rate: 5.70% p.a.

Term: 12 months Interest payment: Quarterly Minimum deposit: $10,000 How to open: Apply via ANZ's website Want to see the pre-tax returns of a term deposit? Visit our Term Deposit Calculator |

|

ASB - 5.90% p.a. for 12 monthsInterest Rate: 5.90% p.a.

Term: 12 months Interest payment: Quarterly (or monthly for deposits $10,000 and above) Minimum deposit: $5,000 How to open: Apply via ASB's website Want to see the pre-tax returns of a term deposit? Visit our Term Deposit Calculator |

Disclosure:

- We have excluded credit unions, finance companies, mortgage trusts and other non-bank deposit takers. To see the current rates and credit ratings of the institutions, visit interest.co.nz.

- Rates are subject to change without notice - please confirm the latest interest rate, early withdrawal fees and interest payments before accepting any investment opportunity.

Investment Term: 18 Months to 5 Years

With over 30 PIE term deposit options available for terms exceeding 12 months, interest rates are constantly fluctuating at an unprecedented pace. With so many options, we suggest visiting each bank's website directly to find a term that best fits your specific needs. To help you get started, we've compiled a list of interest rates from all six banks that offer PIE term deposits:

How do I pick the best PIE term deposit offer?

The best PIE term deposit is likely going to have the highest interest rate for the term you want to invest (i.e. three months or two years) from the most stable bank. You’ll also need to meet the minimum deposit threshold, which can be $1,000, $2,000 or as high as $10,000. Other considerations include:

How can I check the balance?

PIE term deposits can be viewed online or via an app to help manage your money. Most banks offer this.

Our view: With interest rates increasing since the OCR increases, the best way to pick a PIE term deposit is by length and interest rate. If you’re prepared to complete the forms and set up an account with a new bank, the difference in interest rates can be significant. 0.50% or even 0.25% can make a $50 or $25 difference on a $10,000 PIE term deposit (before tax).

- How often is interest calculated? The best PIE term deposits pay interest monthly, meaning it compounds, while others pay interest ‘at maturity’. With interest rates increasing with the OCR, this is something to be aware of.

- Is there a break fee or penalty? If you think you’ll need the money before the term ends, you’ll pay a break fee. It’s likely to be an interest penalty, rather than an actual charge. However, check the details to be sure. If you may need the money, a savings account which allows instant access to your money could be a better option.

How can I check the balance?

PIE term deposits can be viewed online or via an app to help manage your money. Most banks offer this.

Our view: With interest rates increasing since the OCR increases, the best way to pick a PIE term deposit is by length and interest rate. If you’re prepared to complete the forms and set up an account with a new bank, the difference in interest rates can be significant. 0.50% or even 0.25% can make a $50 or $25 difference on a $10,000 PIE term deposit (before tax).

PIE Term Deposit Frequently Asked Questions

While PIE term deposits are fairly simple, there are a few important details to be aware of. We answer the most common questions below:

Who offers PIE term deposits?

Most (but not all banks) offer PIE term deposits – our top term deposits has the latest offers and all the details you need to know. PIE options aren't offered by smaller banks - TSB, Co-operative, Rabobank and SBS being examples. Our editorial policy excludes the publication of any PIE or term deposit offers from finance companies, specialist mortgage lenders or unregulated issuer.

Can I open a joint PIE term deposit?

Generally not. However, high-interest savings accounts offer joint-control.

Are there any fees associated with PIE term deposits?

In most cases, there are no fees associated with PIE term deposits. However, if you need to withdraw your money before the end of the term, you may face a penalty in the form of lost interest.

Can I access my money before the end of the term?

Generally, you cannot access your money before the end of the term without incurring a penalty. However, some banks offer the option to break your term deposit early if you need to access your funds for an emergency.

Is a PIE term deposit safe?

While no investment is 100% safe, PIE term deposits fall into the category of ‘low risk’ (just as standard term deposits do). They also offer a guaranteed return – the interest rate is fixed for the term of the deposit. This differs from savings accounts where the interest rate can change at any time.

What are the tax implications of interest earned on term deposits?

Per the NZ government, when you make a term deposit, you need to tell your provider (i.e. the bank):

- Your IRD number

- The tax rate you should pay, based on your income.

How do I open a term deposit?

The best way is to open a term deposit online on via the bank's website, or by visiting the bank’s branch. You’ll need to provide a few documents (like an ID and proof of address) to validate your ownership and source of funds. Once approved, your money will be locked in for the agreed term.

What happens at the end of the investment's term?

Once term deposits reach the end of the term, it ‘matures’ and you’ll be given two options. Firstly, you can roll it over for the same term length at the market interest rate (which may be the same or higher or lower than the rate you first signed up for). Alternatively, you can transfer the money to a regular bank or savings account. If you want to withdraw the money before the term ends, you’ll pay a penalty for doing so.

Can I roll over my PIE term deposit when it matures?

Yes - most banks offer the option to roll over your PIE term deposit when it matures. This means that your investment will automatically be reinvested for another term at the prevailing interest rate. If you don't want to roll over your investment, you'll need to notify the bank before the end of the term.

Can I make additional deposits to my PIE term deposit?

No, a PIE term deposit is a fixed-term investment that cannot be added to once established. To make additional deposits, you must open a new PIE term deposit or consider other investment options, such as a savings account.

Can I have multiple PIE term deposits with different banks?

Yes, you can have multiple PIE term deposits with different banks or many at the same bank. There is no limit.

What happens if I need to withdraw my money early?

If you need to withdraw your money from a PIE term deposit before the end of the term, you may face a penalty in the form of lost interest. The penalty amount depends on the bank's policies and the time remaining in the term. Some banks may offer the option to break your term deposit early in certain circumstances, such as for an emergency or a major life event, but this will generally result in a penalty.

PIE Term Deposits - Pros and Cons

PIE term deposits offer security, but they may not be for everyone. We discuss the pros and cons below:

Pros:

Pros:

- Low risk – you’ll earn the interest rate you agree to, and there’s next to no chance of losing your money if you invest with a New Zealand bank.

- Tax advantage - you'll benefit if you pay 30%, 33% or 39% marginal tax given PIE cap taxes on interest earned at 28%.

- Compound interest - some PIE term deposits offer the option to have interest compounded, which means you earn interest on the interest you have already earned.

- Guaranteed return - with a fixed interest rate, you know exactly how much interest you will earn over the life of your investment.

- Diversification - term deposits can be a useful component of a diversified investment portfolio, providing a low-risk, stable source of income.

- No fees – you don’t pay anything to invest (unless you break the term to access your money).

- Locks in an interest rate – unlike most other investments, your return is fixed. No matter what the sharemarket or Reserve Bank does during your term, you will receive the interest you agreed on.

- Encourages good savings habits – a term deposit is locked in, so without the hassle of breaking it and incurring penalties, having the money invested (and rolling it over when the term ends) keeps your finances in order.

- You can’t access your money until the term ends – this means you’ll need to budget accordingly and have enough money

- You can’t add to the term deposit while it’s invested – savings accounts allow and encourage you to keep saving, but term deposits are fixed until maturity. If you want to save more, you’ll need a savings account.

- No flexibility – term deposits are fixed for a period of time, and if interest rates increase, you won’t benefit. However, you’ll be protected if they fall.

- Opportunity cost - because your money is tied up in a term deposit, you may miss out on other investment opportunities that arise during the term of your deposit.

- Inflation risk - because the interest rate is fixed, there is a risk that inflation could erode the value of your returns over time - New Zealand's inflation continues to be higher than any PIE term deposit offer.