Retirement Drawdown Guide - Proven Strategies to Help Withdraw and Spend Your KiwiSaver and Retirement Savings

Our guide explains how to withdraw and spend your KiwiSaver and retirement savings wisely, with expert guidance on drawdown plans, spending insights, risks, must-know facts and essential tools.

Updated 7 June 2024

Summary

Retirement planning involves two key steps:

Why MoneyHub has published this guide

This guide primarily focuses on making the most of what you've got and the spending portion of retirement planning. Our guide covers:

Know This First:

- Many New Zealanders are close to reaching the traditional retirement age (65) and receiving their NZ Super. They will undoubtedly be looking forward to enjoying retirement and furthering their interests.

- However, one of the biggest fears for many is whether they have enough money to retire on - or if they think they've got enough, they might be unsure what the best way to draw down on the different funds they've got.

- From KiwiSaver to cash in the bank to term deposits to investing platforms to real estate to investment funds to inheritances to pulling equity out via reverse mortgage, there are many ways to go about the “Retirement Drawdown”, which can get increasingly complex with more funds and assets to manage.

- Once you've got a proper drawdown strategy, you might not be sure if you're doing it right (retirement is hopefully many decades-long). Knowing how to track and "manage" the retirement drawdown over time will help to ensure that you know that you're on the right track and won't run out of funds near the end of life.

Retirement planning involves two key steps:

- How much you should save for retirement

- How to best spend what you’ve saved in retirement

Why MoneyHub has published this guide

- As New Zealanders approach retirement, one of the most significant concerns is whether they have enough savings to support their desired lifestyle. We're in a long-term cost-of-living crisis, and the transition from regular income to relying on savings and investments can be daunting.

- Without a solid plan, there's a risk of outliving your funds and becoming solely reliant on NZ Super. With the complexity of managing various assets, be it KiwiSaver, term deposits, real estate, and/or other investments, it's essential to have a clear strategy for drawing down these resources effectively.

- This guide is designed to help you navigate the complexities of retirement drawdown strategies, ensuring you make the most of your retirement savings. We focus on what a retirement drawdown strategy is and why it's crucial and how to create a sustainable spending plan that balances your needs and goals.

This guide primarily focuses on making the most of what you've got and the spending portion of retirement planning. Our guide covers:

- What is a Retirement Drawdown Strategy? Why Do I Need One?

- Retirement Spending Insights

- How Much Can I Withdraw Each Year in Retirement?

- Understanding Popular and Trusted Types of Withdrawal and Drawdown Strategies

- Retirement Drawdown Calculators and Tools

- Must-Know Facts about Retirement Withdrawal and Spending

- Frequently Asked Questions about Retirement Withdrawals and Spending

- Concluding Comments

Know This First:

- Due to the complex modelling nature of retirement drawdown withdrawals and spending, and to make it easier to use and understand, we have listed a selection of online calculators, tools and reports to help assist with each unique retiree's retirement.

- By doing so, we avoid creating and sharing an Excel spreadsheet that might be difficult to use, problematic to consistently interpret and not easy to visualise.

- The free tools we list are the easiest, most accurate and most digestible way to get a bespoke retirement spending plan. MoneyHub doesn't have any affiliation with the calculators named below and we publish them in good faith.

- While we have tried to be as detailed as possible to capture all different retirement scenarios; most drawdown strategies (e.g., how you spend your retirement funds) are explained at a high level and are meant as an example guide and will almost certainly vary depending on the risk profile and how conservative retirees are.

- If you're still anxious or unsure about retirement after using the calculators below, you may want to consult with a fee-only financial advisor for personalised assistance and ensure alignment of incentives.

Our Top-Rated Savings Account With Day-to-Day FlexibilityBest Account for Wealth Creation and Flexibility:

What sets Savvy apart?

Savvy arguably redefines how we think about money management, merging the convenience of a debit card with the benefits of an investment fund, all while offering impressive returns. It's a forward-thinking solution for those who want their money to work harder for them without sacrificing accessibility or ease of use. More details: Our Savvy Review explains the product in detail, as does the Savvy website. |

|

What is a Retirement Drawdown Strategy? Why Do I Need One?

A retirement drawdown strategy is a plan that explains:

Know This: I’m not retired yet - why would I need to create a retirement drawdown strategy?

Far too many New Zealanders get to retirement age and know they can withdraw their KiwiSaver but don’t know what to do, specifically:

While most New Zealanders might think they'll be able to sort out retirement planning during retirement (e.g. after NZ Super payments commence), it's important to make sure you have a plan before you hit retirement age. The more you plan out your retirement drawdown strategy, the safer and more enjoyable your retirement will be.

- Where: You will find the cash flow to supplement the lifestyle you want against the income that comes in.

- How: You will invest and organise your assets to optimise your portfolio growth while in retirement.

- What: Assets you should be selling down first.

- When: You should withdraw and spend your money (e.g. earlier in retirement or later).

Know This: I’m not retired yet - why would I need to create a retirement drawdown strategy?

Far too many New Zealanders get to retirement age and know they can withdraw their KiwiSaver but don’t know what to do, specifically:

- The trade-offs of withdrawing it or leaving it in

- Whether to reinvest it into term deposits or invest it in ETFs

- How much to leave aside in cash in retirement

- When they should be making their withdrawals to support their cash flow during the year

- Whether they’re spending too much or too little in the early retirement years.

While most New Zealanders might think they'll be able to sort out retirement planning during retirement (e.g. after NZ Super payments commence), it's important to make sure you have a plan before you hit retirement age. The more you plan out your retirement drawdown strategy, the safer and more enjoyable your retirement will be.

What age do I need to be to think about retirement planning and drawdown strategies?

Anyone of any age can consider retirement drawdown strategies. However, those likely to have the most practical benefit will be nearing retirement age (e.g. 60 to 65 years old). If you plan to retire early, a retirement drawdown strategy also makes sense (but you'll have a longer retirement duration and won't be able to draw down your KiwiSaver or receive NZ Super payments, so the drawdown calculations will be slightly different - check out our FIRE guides at the end of the page).

Popular KiwiSaver Calculators:

Other Calculators and Resources

Popular KiwiSaver Calculators:

- Sorted KiwiSaver Calculator

- ANZ KiwiSaver Calculator

- MAS KiwiSaver Retirement Calculator

- Westpac KiwiSaver Scheme Calculator

- BNZ KiwiSaver Scheme Calculator

- AMP KiwiSaver Retirement Calculator

- Generate Wealth KiwiSaver Calculator

Other Calculators and Resources

Retirement Spending Insights

Before exploring the strategies and inputs required for calculating retirement spending and drawdown, it's important to map out what factors to consider when considering retirement holistically. Note that the majority of the graphs below are sourced from J.P. Morgan’s Guide to Retirement, which will be US-centric (but the insights are still relevant for New Zealanders).

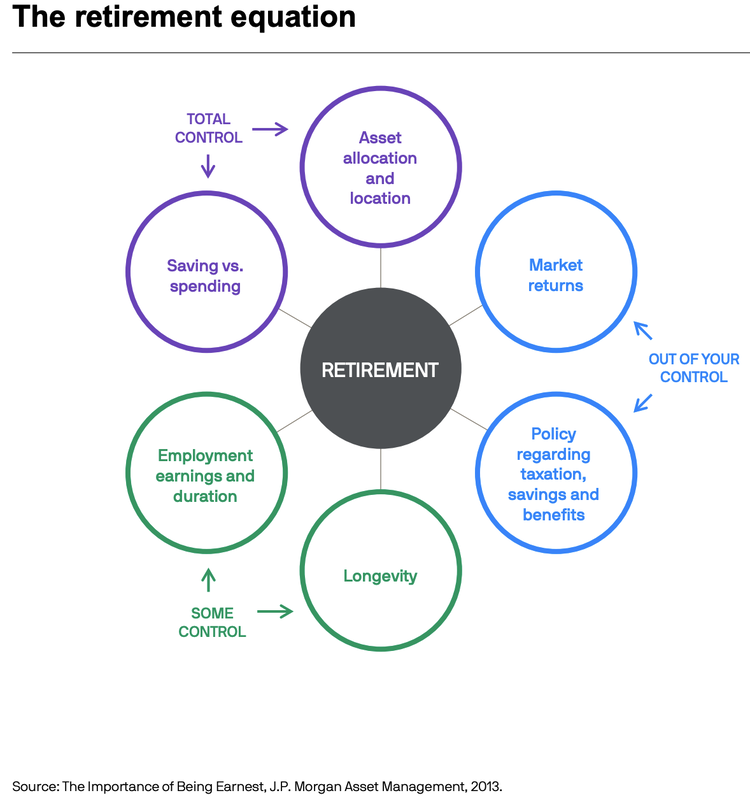

1. Understand What’s In Your Control

In retirement, there will be things that are in your complete control, things that are partially in your control and things that are not in your control at all. To make the most of retirement planning, focusing on making the most of the things you can control and understanding the things that are somewhat or completely out of your control will lead you to the most successful retirement. For example, while you can't know how long you'll live or what market returns you'll get, you can control your spending rate.

1. Understand What’s In Your Control

In retirement, there will be things that are in your complete control, things that are partially in your control and things that are not in your control at all. To make the most of retirement planning, focusing on making the most of the things you can control and understanding the things that are somewhat or completely out of your control will lead you to the most successful retirement. For example, while you can't know how long you'll live or what market returns you'll get, you can control your spending rate.

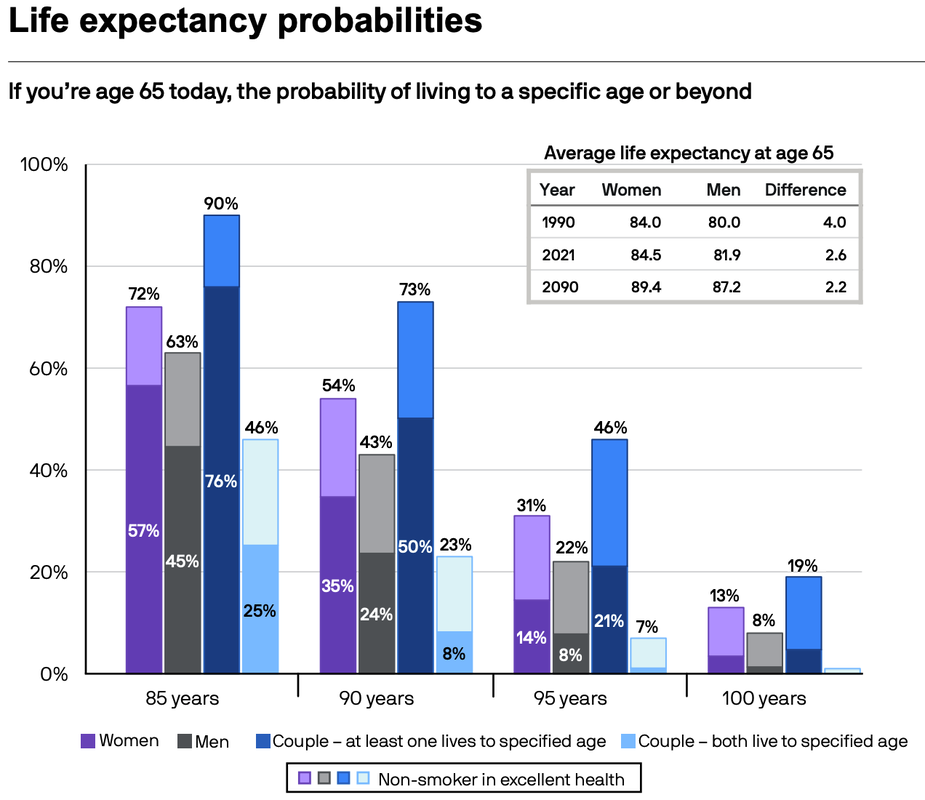

2. Consider How Long You’ll Live

While nobody can know how long they will live, it's better to have some idea (based on data) of how long you'll live to get as accurate a picture as possible regarding how much money you'll need. Note that average life expectancy is a midpoint, not an endpoint. You might need to plan on the probability of living much longer (e.g. 35 years plus), especially if you're in good health (or your parents and grandparents lived a long time). Generally, the longer you have to live, the higher your allocation to higher growth investments you should have (to ensure your portfolio keeps its purchasing power over time).

While nobody can know how long they will live, it's better to have some idea (based on data) of how long you'll live to get as accurate a picture as possible regarding how much money you'll need. Note that average life expectancy is a midpoint, not an endpoint. You might need to plan on the probability of living much longer (e.g. 35 years plus), especially if you're in good health (or your parents and grandparents lived a long time). Generally, the longer you have to live, the higher your allocation to higher growth investments you should have (to ensure your portfolio keeps its purchasing power over time).

Source: JP Morgan Guide to Retirement (page 4)

3. Understand Lifestyle Spending

The type of lifestyle you want to lead has a huge amount of variance. Some New Zealanders are happy to watch YouTube, spend time with family and eat at home. Others want to go out regularly, travel the world three months of the year on cruises and buy new gadgets, as well as help out younger family members.

As seen in the graphic below from JP Morgan, most of the time people spend working is likely substituted for social interactions, pursuing leisure activities (like hobbies or personal interests), and exercising. As such, the type of social events and leisure activities you pursue will significantly impact how much you'll spend in retirement (and, by extension, how much you need to have saved up).

The type of lifestyle you want to lead has a huge amount of variance. Some New Zealanders are happy to watch YouTube, spend time with family and eat at home. Others want to go out regularly, travel the world three months of the year on cruises and buy new gadgets, as well as help out younger family members.

As seen in the graphic below from JP Morgan, most of the time people spend working is likely substituted for social interactions, pursuing leisure activities (like hobbies or personal interests), and exercising. As such, the type of social events and leisure activities you pursue will significantly impact how much you'll spend in retirement (and, by extension, how much you need to have saved up).

Source: JP Morgan Guide to Retirement (page 6)

Know This: Figuring out the necessary funds for retirement is a complex question with varied answers, depending largely on your desired lifestyle post-retirement.

Because many New Zealanders will be eligible for NZ Superannuation at 65, participate in KiwiSaver schemes, and have equity in their home or investment accounts, it can be difficult to determine whether what you've got is "enough". This is why utilising the various retirement calculators and tools online is one of the easiest ways to visually show how long your assets and NZ Super will last.

Upon reaching 65, you're likely to begin receiving NZ Superannuation. If we were to approximate most couples, they would receive $40,000 a year in NZ Super income. While this might be enough for some families (especially if they already own their house outright and are relatively frugal), this won't be enough for most.

Thus, additional savings from KiwiSaver and other investments must cover any shortfall in your expected spending and the NZ Super rate. The exact amount you'll need will depend on your desired lifestyle and lifespan (which is why the tools and calculators are useful for scenario planning).

You can see the current Super rates here.

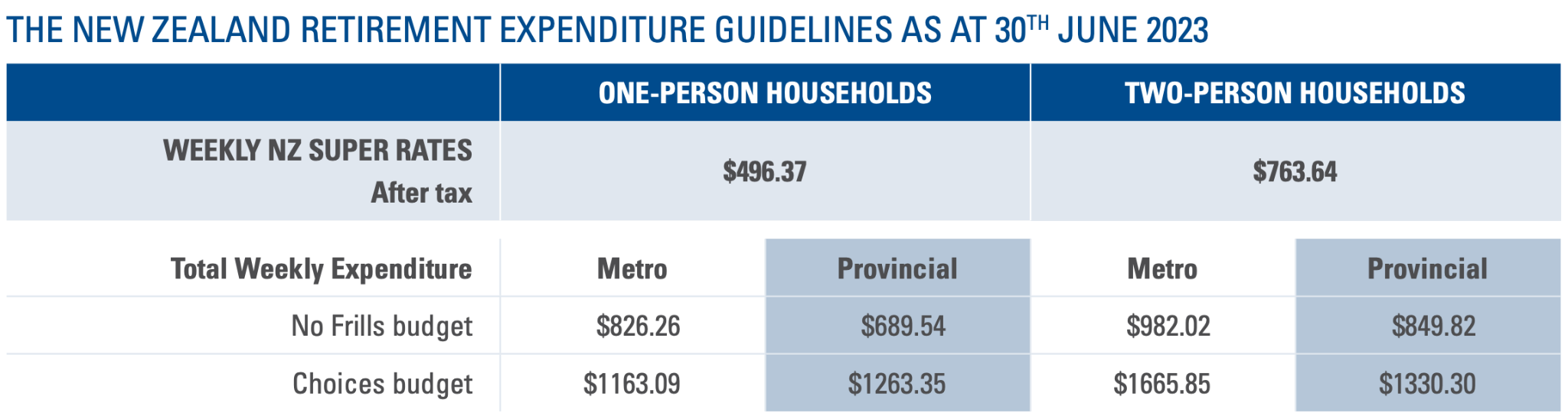

Based on Massey University's Retirement Guidelines (published June 2023) below, the weekly NZ Super rates are not enough for the typical one-person or two-person households in metro or provincial areas (in either a "No Frills budget" or "Choices budget").

Know This: Figuring out the necessary funds for retirement is a complex question with varied answers, depending largely on your desired lifestyle post-retirement.

Because many New Zealanders will be eligible for NZ Superannuation at 65, participate in KiwiSaver schemes, and have equity in their home or investment accounts, it can be difficult to determine whether what you've got is "enough". This is why utilising the various retirement calculators and tools online is one of the easiest ways to visually show how long your assets and NZ Super will last.

Upon reaching 65, you're likely to begin receiving NZ Superannuation. If we were to approximate most couples, they would receive $40,000 a year in NZ Super income. While this might be enough for some families (especially if they already own their house outright and are relatively frugal), this won't be enough for most.

Thus, additional savings from KiwiSaver and other investments must cover any shortfall in your expected spending and the NZ Super rate. The exact amount you'll need will depend on your desired lifestyle and lifespan (which is why the tools and calculators are useful for scenario planning).

You can see the current Super rates here.

Based on Massey University's Retirement Guidelines (published June 2023) below, the weekly NZ Super rates are not enough for the typical one-person or two-person households in metro or provincial areas (in either a "No Frills budget" or "Choices budget").

Exhibit: Massey University Retirement Budget (by Household and Lifestyle)

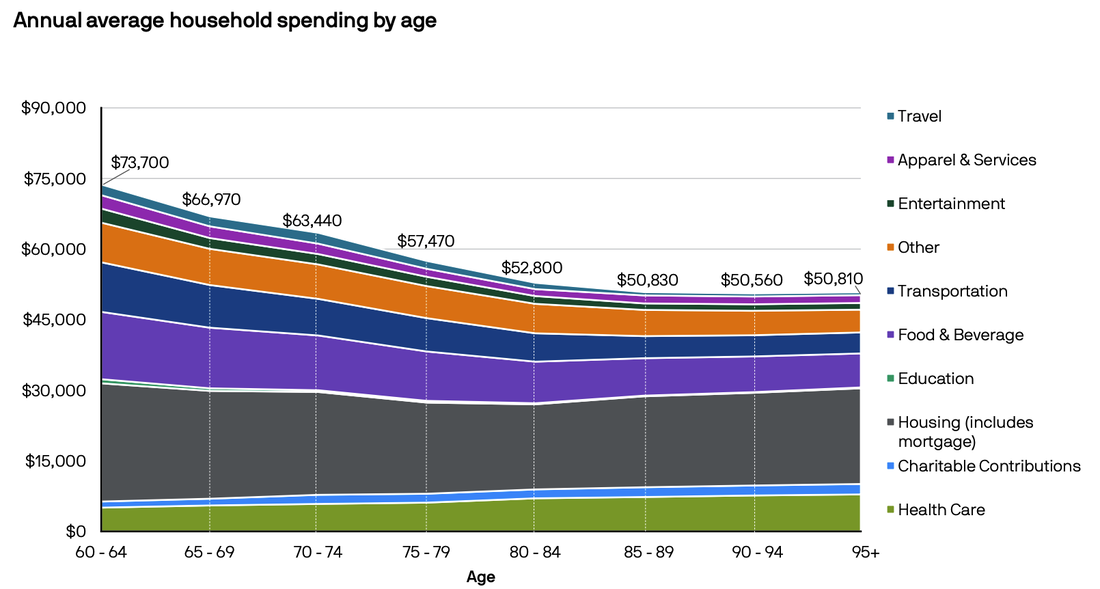

USA Average Household Spending by Age (Source: JP Morgan Guide to Retirement (page 28)

4. Your Retirement Spending Will Change Over Time

It’s well documented in the JP Morgan graphic below that your retirement spending will decay over time, usually in three phases:

It’s well documented in the JP Morgan graphic below that your retirement spending will decay over time, usually in three phases:

- Go-Go Years: Once you retire, there will be a long list of things you've been dying to pursue but didn't have the time to undertake. These "Go-go" years usually involve taking off and travelling, buying that equipment to pursue the hobby and generally just spending up.

- Slow-Go Years: After the initial few months or years of the "Go-go" years, many retirees have done what they initially wanted and might want to settle into a more relaxed routine rather than doing everything on their bucket list. This is often when retirees may still go to restaurants and spend time with family. Still, the number of trips abroad to Europe may reduce (whether they've already "ticked off that bucket list item" or are generally less interested in going to the same places again).

- No-Go Years: Once you're deep into your retirement (think ages 80+), you tend not to have the desire, health or ability to spend on things you used to have at the start of retirement. As a result, your spending typically drops substantially (except in areas like private healthcare expenses, passing down inheritances early or charitable contributions).

Source: JP Morgan Guide to Retirement (page 26)

How Much Can I Withdraw Each Year in Retirement?

The New Zealand Society of Actuaries has formulated four key guidelines to help estimate a sustainable level of after-tax expenditure from your retirement savings. While imperfect, these guidelines offer a practical approach to retirement planning.

Know This: These guidelines do not include considerations for NZ Superannuation or other potential income sources in retirement, which should be evaluated separately.

1. 6% Guideline

Annually spend 6% of your initial retirement savings (flat amount not adjusted for inflation). For instance, if you retire at 65 with $500,000 in savings, you would spend $30,000 yearly (in addition to NZ Super). While this method is simple and easy to implement (given you only need to calculate the withdrawal amount once), it’s likely the worst of the four methods due to its inability to factor in inflation. For example, if your retirement was for 30 years, spending $30,000 in 2024 is a significantly different sum compared to $30,000 in 2054.

Additionally, spending 6% of your retirement savings each year is a significantly higher initial withdrawal rate than most other methods, which risks depleting savings faster (especially if the first few years of retirement are poor - known as the Sequence of Return Risk).

2. Inflation-Adjusted 4% Rule Guideline

This guideline involves spending 4% of your initial retirement savings, adjusting annually for inflation. For example, with a $300,000 savings at retirement, spend $12,000 in the first year. If inflation is 2%, then spend $12,240 the following year. While this method maintains spending power relative to inflation (which reduces the likelihood of outliving savings), it requires an annual calculation and adjustment to how much you withdraw.

3. Fixed Date Guideline

Divide your retirement savings annually by the number of years until a predetermined date. For example, if you retire at 65 with $300,000 and plan to spend until age 90, this method suggests you spend $12,000 in the first year and then adjust annually. While this guideline is useful in that it ensures all your funds are spent and distributed consistently until a specific date, it doesn't vary spending each year (meaning if you live longer than your specified date, you'll run out of money or need to recalculate how much you spend each year).

4. Life Expectancy Guideline

Spend an amount based on your retirement savings divided by your life expectancy annually. For example, a New Zealand male retiring at 65 with $300,000 would spend $14,300 in the first year, then adjust annually based on updated life expectancy. While this method is useful as it adjusts spending throughout your lifetime, you might live far longer than expected, requiring adjustments.

Know This: These guidelines do not include considerations for NZ Superannuation or other potential income sources in retirement, which should be evaluated separately.

1. 6% Guideline

Annually spend 6% of your initial retirement savings (flat amount not adjusted for inflation). For instance, if you retire at 65 with $500,000 in savings, you would spend $30,000 yearly (in addition to NZ Super). While this method is simple and easy to implement (given you only need to calculate the withdrawal amount once), it’s likely the worst of the four methods due to its inability to factor in inflation. For example, if your retirement was for 30 years, spending $30,000 in 2024 is a significantly different sum compared to $30,000 in 2054.

Additionally, spending 6% of your retirement savings each year is a significantly higher initial withdrawal rate than most other methods, which risks depleting savings faster (especially if the first few years of retirement are poor - known as the Sequence of Return Risk).

2. Inflation-Adjusted 4% Rule Guideline

This guideline involves spending 4% of your initial retirement savings, adjusting annually for inflation. For example, with a $300,000 savings at retirement, spend $12,000 in the first year. If inflation is 2%, then spend $12,240 the following year. While this method maintains spending power relative to inflation (which reduces the likelihood of outliving savings), it requires an annual calculation and adjustment to how much you withdraw.

3. Fixed Date Guideline

Divide your retirement savings annually by the number of years until a predetermined date. For example, if you retire at 65 with $300,000 and plan to spend until age 90, this method suggests you spend $12,000 in the first year and then adjust annually. While this guideline is useful in that it ensures all your funds are spent and distributed consistently until a specific date, it doesn't vary spending each year (meaning if you live longer than your specified date, you'll run out of money or need to recalculate how much you spend each year).

4. Life Expectancy Guideline

Spend an amount based on your retirement savings divided by your life expectancy annually. For example, a New Zealand male retiring at 65 with $300,000 would spend $14,300 in the first year, then adjust annually based on updated life expectancy. While this method is useful as it adjusts spending throughout your lifetime, you might live far longer than expected, requiring adjustments.

Understanding Popular and Trusted Types of Withdrawal and Drawdown Strategies

1. Guardrail strategy

The Guardrails Approach is a dynamic retirement withdrawal strategy that helps manage spending and asset preservation during retirement. It involves setting upper and lower limits on withdrawal rates, allowing adjustments based on market performance and personal financial circumstances.

For example, if you decided to spend 4% (inflation-adjusted) every year, the guardrail strategy would allow you to increase your spending in years in which you generate higher returns (meaning you might be able to withdraw 5% compared to 4% if your portfolio increased by 10%). Still, you would need to cut back on spending in years that generate lower returns (e.g. you might withdraw only 3% compared to 4% if the sharemarket has a downturn).

This method balances spending and saving, adapting to market fluctuations and life changes. It stands out for its flexibility compared to fixed percentage or inflation-adjusted withdrawal strategies, requiring regular management and monitoring to ensure sustainability and effectiveness.

2. Withdraw living expenses semi-regularly (e.g. once a year or every quarter)

The less money you have sitting in cash, the more money you have invested working for you in retirement. While it's always good to be prudent and have a little more than the bare bones in case of unexpected emergencies, the reality is that most share investment platforms and managed funds can be liquidated, and the cash can be transferred into your bank within days.

Having too much wealth in low-return assets (like savings accounts or term deposits) can harm your long-term prospects of having your portfolio last your entire retirement period. Consider setting a set amount to withdraw each year (e.g. on January 1st, you cash out one year's worth of living expenses - say $50,000 - to have in your everyday account that funds your retirement while investing all the rest) or a quarter (on January 1st, April 1st, July 1st and October 1st, you cash out three months worth of living expenses - say $12,500 - to have in your everyday account that funds your retirement, while investing all the rest). It’s common for retirees to put this money in a call account or consider everyday access accounts like Booster Savvy which offers a debit card, a 5% p.a. interest rate, expense tracking and bonus interest.

3. Laddering term deposits and cash flows

The biggest practical consideration for many New Zealanders will be when your cash comes in - known as cash flow. If you know when you'll likely be spending your cash across the year (e.g. you spend more in winter because you like to fly down to Queenstown to stay in a hotel and ski), you can structure your term deposits or other investments to "come off" their investment period at the right time you need them. This is called Laddering your Term Deposits.

The Guardrails Approach is a dynamic retirement withdrawal strategy that helps manage spending and asset preservation during retirement. It involves setting upper and lower limits on withdrawal rates, allowing adjustments based on market performance and personal financial circumstances.

For example, if you decided to spend 4% (inflation-adjusted) every year, the guardrail strategy would allow you to increase your spending in years in which you generate higher returns (meaning you might be able to withdraw 5% compared to 4% if your portfolio increased by 10%). Still, you would need to cut back on spending in years that generate lower returns (e.g. you might withdraw only 3% compared to 4% if the sharemarket has a downturn).

This method balances spending and saving, adapting to market fluctuations and life changes. It stands out for its flexibility compared to fixed percentage or inflation-adjusted withdrawal strategies, requiring regular management and monitoring to ensure sustainability and effectiveness.

2. Withdraw living expenses semi-regularly (e.g. once a year or every quarter)

The less money you have sitting in cash, the more money you have invested working for you in retirement. While it's always good to be prudent and have a little more than the bare bones in case of unexpected emergencies, the reality is that most share investment platforms and managed funds can be liquidated, and the cash can be transferred into your bank within days.

Having too much wealth in low-return assets (like savings accounts or term deposits) can harm your long-term prospects of having your portfolio last your entire retirement period. Consider setting a set amount to withdraw each year (e.g. on January 1st, you cash out one year's worth of living expenses - say $50,000 - to have in your everyday account that funds your retirement while investing all the rest) or a quarter (on January 1st, April 1st, July 1st and October 1st, you cash out three months worth of living expenses - say $12,500 - to have in your everyday account that funds your retirement, while investing all the rest). It’s common for retirees to put this money in a call account or consider everyday access accounts like Booster Savvy which offers a debit card, a 5% p.a. interest rate, expense tracking and bonus interest.

3. Laddering term deposits and cash flows

The biggest practical consideration for many New Zealanders will be when your cash comes in - known as cash flow. If you know when you'll likely be spending your cash across the year (e.g. you spend more in winter because you like to fly down to Queenstown to stay in a hotel and ski), you can structure your term deposits or other investments to "come off" their investment period at the right time you need them. This is called Laddering your Term Deposits.

Retirement Drawdown Calculators and Tools

Online retirement calculators allow New Zealanders to map out their spending visually over the coming years (including NZ Super, any additional income, and the "shortfall" made up by investment returns or nest egg cash freed up). These calculators also projected nest egg growth and returns (on the portion still invested and not put aside for living costs).

Important: The Calculators Have Limitations

Most retirement calculators are built to approximate your total retirement income, considering potential benefits from NZ Super and other investments. Calculators will often have the option to include your spouse or partner's retirement savings details, if applicable. Additionally, it allows you to assess the impact of significant life events, such as career breaks or transitioning to part-time employment, on your future retirement funds.

Take note of:

Inputs You’ll Need For Retirement Planning

Some initial questions that you’ll need before completing the various retirement drawdown calculators:

The Two Main Types of Calculators

Case Study One: Mercer New Zealand Retirement Income Simulator

Using Mercer's New Zealand Retirement Income Simulator, New Zealanders can put in their relevant inputs (listed above) and generate a five-page report that shows:

Important: The Calculators Have Limitations

Most retirement calculators are built to approximate your total retirement income, considering potential benefits from NZ Super and other investments. Calculators will often have the option to include your spouse or partner's retirement savings details, if applicable. Additionally, it allows you to assess the impact of significant life events, such as career breaks or transitioning to part-time employment, on your future retirement funds.

Take note of:

- Unforeseen circumstances: Note that many calculators will not predict future personal circumstances or actual investment returns, might not adjust spending for inflation or factor in potential alterations in NZ Super (such as if the minimum eligible age for NZ Super payout changes) and tax laws (such as FIF taxes or trust income.

- Default Assumptions: Most tools will incorporate default assumptions regarding future investment returns and inflation based on current long-term economic projections. These assumptions are adjustable to suit different scenarios.

- Foreign Exchange: Calculators often denominate their results in the home country they are based in (for example, Sorted's Retirement Calculator

- will be denominated in NZD, but HonestMath’s calculator uses USD). While it won’t always make a difference in the drawdown strategy, just be mindful of what currency they’re projecting in.

Inputs You’ll Need For Retirement Planning

Some initial questions that you’ll need before completing the various retirement drawdown calculators:

- Current Age

- Are you an individual or a couple?

- Net worth (assets & liabilities)

- What income sources will you have post-retirement (none, part-time work, NZ Super, KiwiSaver, share investment dividends, interest from term deposits, etc.)?

- What likely expenses will you incur post-retirement?

- Expected Fortnightly NZ Super Payments

- KiwiSaver balance

- Savings or Term Deposit accounts

- Investment accounts

- Select anticipated future returns on the above Kiwisaver, investments, etc. (depends on what fund the person's in & its risk level – conservative/balanced/growth or combination)

- Anticipated inflation rate

The Two Main Types of Calculators

- Retirement Calculators (intended for managing expenditures during retirement).

- KiwiSaver Calculators (designed for the phase of accumulating retirement savings).

Case Study One: Mercer New Zealand Retirement Income Simulator

Using Mercer's New Zealand Retirement Income Simulator, New Zealanders can put in their relevant inputs (listed above) and generate a five-page report that shows:

- Statistics on how long your funds are expected to last you.

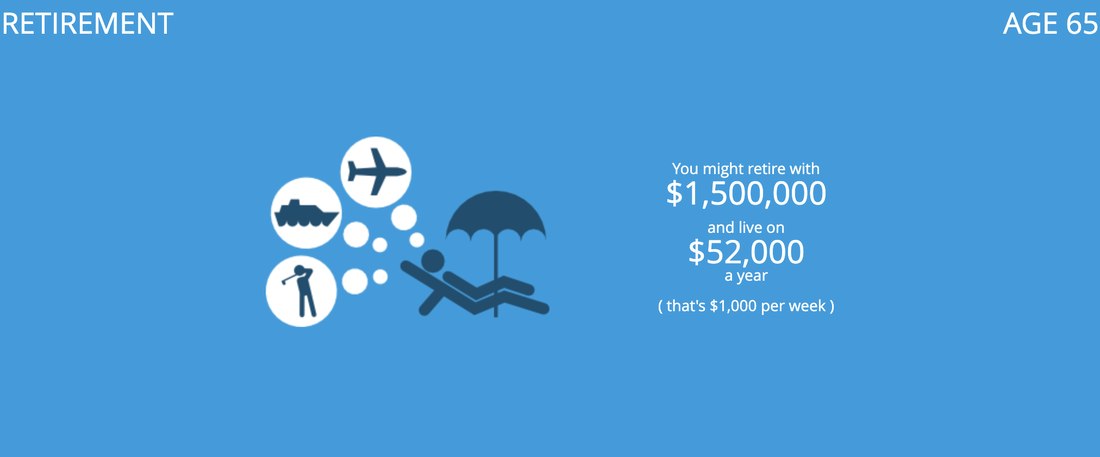

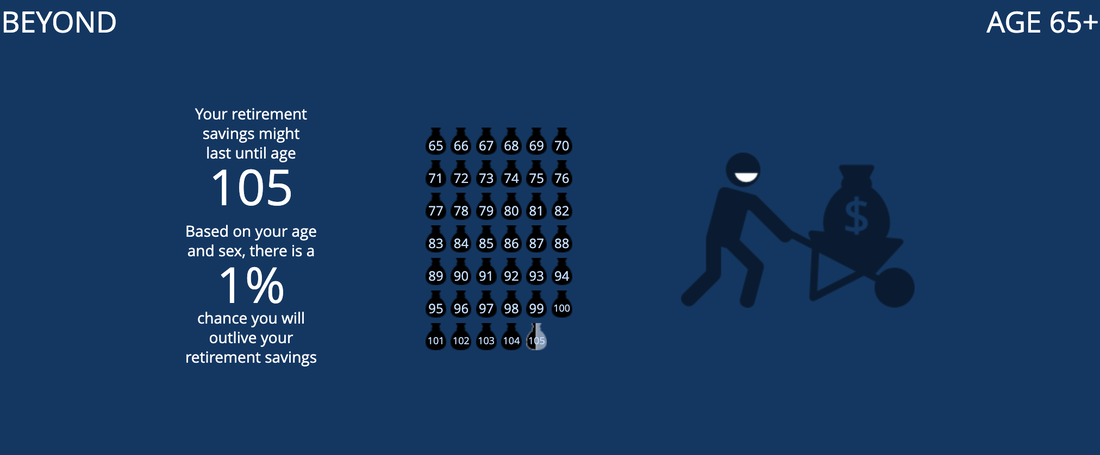

- What your likely income shortfall is (in this example, to reach a $52,000 a year spending/withdrawal amount, they would need to fund around a $25,000 a year shortfall through sell off portions of their $1.5m investment portfolio).

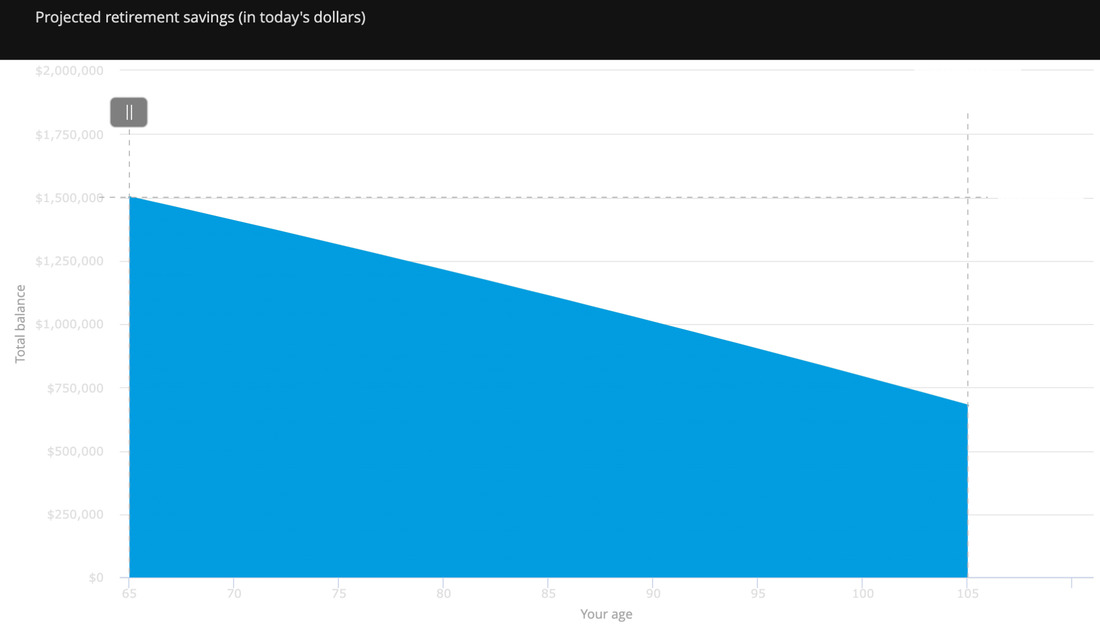

- Your portfolio value over time (as they end up selling their portfolio each year to meet the shortfall).

Exhibit: High-Level Net Worth and Forecasted Living Expenses.

Exhibit: Forecasted Calculations on How Long Your Savings Will Last.

Exhibit: Forecasted Income in Retirement (NZ Super + Retirement Savings Drawdown).

Exhibit: Mercer New Zealand Retirement Simulation Report Across Time.

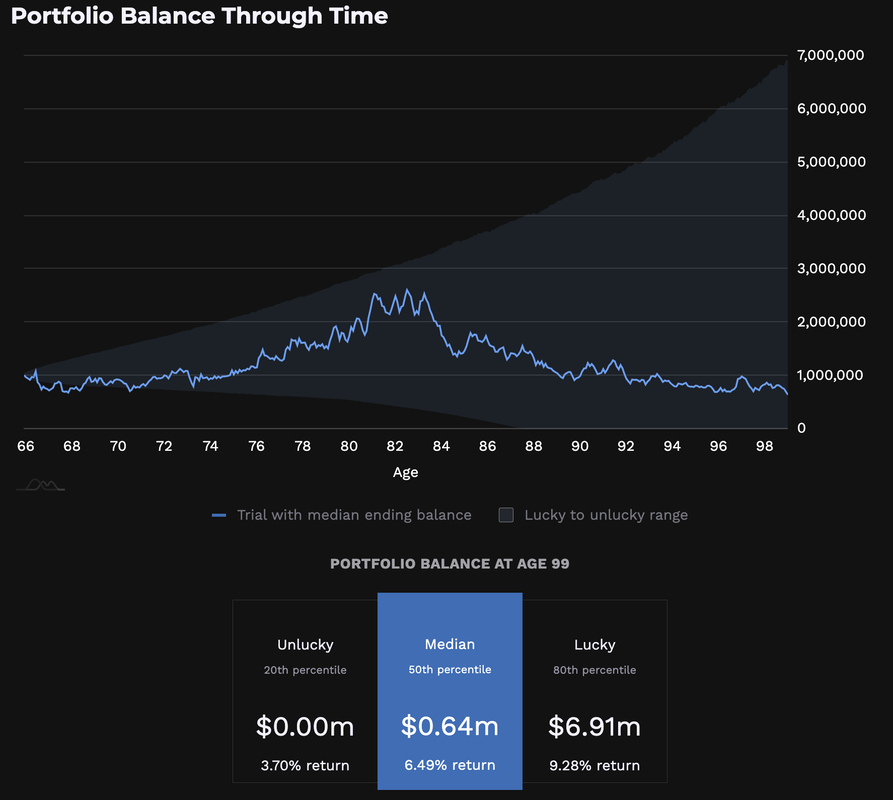

Case Study Two: Honest Math Retirement Portfolio Simulator

As an alternative, Honest Math has a portfolio simulator to show whether your existing investments (and NZ Super - which is called Social Security in the calculator, given it's a USA-based company) will last your entire retirement duration (given various inputs like return profile, asset allocation etc.). This can be a useful sense-check to see whether your portfolio will likely last you through retirement.

As an alternative, Honest Math has a portfolio simulator to show whether your existing investments (and NZ Super - which is called Social Security in the calculator, given it's a USA-based company) will last your entire retirement duration (given various inputs like return profile, asset allocation etc.). This can be a useful sense-check to see whether your portfolio will likely last you through retirement.

Exhibit: Honest Math Retirement Portfolio Simulator.

In addition to the two case study Retirement Calculators above, here are some related links and alternatives that New Zealanders might find useful:

In addition to the two case study Retirement Calculators above, here are some related links and alternatives that New Zealanders might find useful:

Must-Know Facts about Retirement Withdrawal and Spending

|

Ease yourself into retirement - it’s not a race.Many New Zealanders think it'll be a seamless transition to retirement, and they'll never have any issues or worries to think of again - this couldn't be further from the truth. Often, the lack of structure, connection to others and meaningful work can make the transition to full-time retirement rough. Transitioning into retirement can be much more seamless if you have a clear plan for what you're retiring to.

|

|

Planning for retirement is one thing, but don’t forget to live it and enjoy yourself.A common oversight is focusing solely on the amount needed for retirement rather than envisioning your retirement activities. Retirement is your time to relish life and celebrate your decades of hard work and consistent saving. Concentrating merely on the financial side of retirement overlooks the richness of lifestyle opportunities and overall well-being from not having to be at the whim of a boss or manager.

|

|

If possible, take a "mini-retirement" and test your retirement plan.While the numbers can tell a story and comfort you that you've got enough, the only real way to know if you're ready to retire is to leap. However, for those who don't want to hand their hats up permanently, a "mini-retirement" is one way to check and see whether your current plan would work.

Whether that's taking a six-month or one-year sabbatical from work, paying for extra leave off or leaving your job with the hope of finding another role in twelve months, taking a "mini-retirement" gives you a level of insight and comfort that numbers and theory just won't give you. |

|

Plan for unexpected costs in retirement (especially medical related).Retirement is notoriously unpredictable. While most types of spending are relatively easy to forecast and can often be paid far in advance (such as housing, food and travel), be careful of the unexpected and significant costs (like a cancer diagnosis).

While insurance is a great way to offset this risk, if you're relatively young compared to most in retirement (e.g. you're in your 60s), you might not have thought to get insurance. If you unexpectedly got stage 4 cancer and the waitlist for an operation through the New Zealand public health system was twelve months, you'll likely seriously consider going through private healthcare (which will cost significant amounts). While we all hope to live to 100, some unlucky New Zealanders will get these diagnoses far earlier than actuarial tables suggest. Anticipating potential retirement expenses such as healthcare will ensure you get peace of mind and are ready for any situation. |

|

The longer you spend in retirement, the more accurate you’ll be able to forecast expenses.Unless you've taken a mini-retirement or fully retired already, it's always difficult to get a true sense of your retirement life. Your expenses will almost always be slightly different than you've projected - you might want to travel less than you thought, spend more on restaurants, or find an unexpected windfall/inheritance from a long-lost uncle.

Either way, as you get deeper into retirement, you'll get better at accurately assessing how much money you'll be spending and your projected returns on your invested assets. This can help determine whether you're spending too much or too little. Try not to sweat the small stuff and take comfort that you’ll get better at forecasting things like income, expenses and net worth growth. |

|

Beware of overspending as soon as you retire.Try not to go on a spending spree once you can access money (NZ Super, Inheritance, KiwiSaver, etc). Most New Zealanders will have a relatively large/significant KiwiSaver sum once they retire (especially when Millennials and Gen Z eventually retire, having had their full working lives to contribute to KiwiSaver and get the government tax credit, matching 3% employer contributions and time in the market for decades).

However, many Kiwi retirees will want to try to avoid spending it all at once (especially given the fear of overspending and potentially running out of cash into old age). There is a natural tendency to spend much of it once you get your hands on it (given it's been locked away for many years). Remember that your working life is over, and the money diligently saved up has to last you the rest of your lifetime - so try to err on caution. $1 usually has far more utility to you in your 60s than in your 90s, so make sure you don't end up with a humongous amount left over in your 90s when you won't have the time or desire to use it. |

|

When you hit 65, don’t leave the entire sum sitting in cash.It's all too easy to reach age 65 and be so overjoyed that you can withdraw your KiwiSaver balance that you end up doing so, but it sits in cash in your bank account. The longer your KiwiSaver balance sits in cash, the less time it has to continue growing (and the more chance inflation has to whittle away).

While ensuring you have enough cash to fund your near-term retirement needs is important, any excess or additional cash above and beyond this number (say 12 - 24 months of living expenses) should be invested. |

|

Retirement planning is not a set-and-forget exercise.Retirement planning is a continuous journey - you don’t just do it once and never look at it again. Don’t expect the calculator, tool or report you generate at the start of retirement to be valid and last for two or three decades.

Reassess how you track at least every few years (if not yearly). Ultimately, there is no guaranteed way of ensuring you'll have a reasonable lifestyle in retirement and not outlive your savings. You can increase your chances of success by erring on the conservative side with matters within your control. |

Frequently Asked Questions about Retirement Withdrawals and Spending

Should I withdraw my KiwiSaver straight away?

It depends. Generally, if you can withdraw it, it makes sense to do so as you'll be able to use the drawn-down funds more flexibly (like reinvesting them, paying off living expenses, etc.).

There are no additional benefits to keeping your retirement funds invested in the KiwiSaver system after age 65 (other than the psychological benefits of staying invested so you don't spend it all).

If you're prudent and can control your spending, withdrawing it is the most common strategy. Otherwise, if you're unsure of what to do once you withdraw the funds, leaving the KiwiSaver funds in (which will continue to grow and compound while you plan and figure out what to do with it) can make sense. Leaving the KiwiSaver balance invested is also a good alternative if you struggle with controlling your spending and are worried you might not spend it wisely. If you're still unsure, talking to a financial advisor can help to ease this anxiety.

There are no additional benefits to keeping your retirement funds invested in the KiwiSaver system after age 65 (other than the psychological benefits of staying invested so you don't spend it all).

If you're prudent and can control your spending, withdrawing it is the most common strategy. Otherwise, if you're unsure of what to do once you withdraw the funds, leaving the KiwiSaver funds in (which will continue to grow and compound while you plan and figure out what to do with it) can make sense. Leaving the KiwiSaver balance invested is also a good alternative if you struggle with controlling your spending and are worried you might not spend it wisely. If you're still unsure, talking to a financial advisor can help to ease this anxiety.

Which account should I pull funds from first?

Generally, the order in which you sell your assets will depend on the most liquid (e.g., what you can sell down the easiest). For example, in descending order from most liquid to least liquid:

Your risk appetite depends heavily on how much you sell down and keep in cash (or short-term deposits). If you're more conservative, you might choose to have more than 12 months of living expenses in the bank. If you're less conservative (or plan to withdraw/sell down assets more regularly), you could have less than 12 months of living expenses in the bank.

- Cash

- Savings accounts

- Investment accounts (like shares or an investment platform account)

- KiwiSaver (assuming you’ve kept it invested and haven’t withdrawn it yet)

- Short Duration Term Deposits (e.g. six-month duration)

- Long Duration Term Deposits (e.g. five-year duration - although you can withdraw these, there's usually a 30-day wait time, and you may get penalised for doing so)

- Reverse Mortgage (Withdrawing equity from your properties)

Your risk appetite depends heavily on how much you sell down and keep in cash (or short-term deposits). If you're more conservative, you might choose to have more than 12 months of living expenses in the bank. If you're less conservative (or plan to withdraw/sell down assets more regularly), you could have less than 12 months of living expenses in the bank.

How can I retire before NZ Super starts at the typical retirement age (before 65)?

Retiring before your typical retirement age is called early retirement (Financial Independence Retire Early, or FIRE). At the end of the guide, we've included a list of all the relevant guides on retiring early.

I completed the retirement planning. What happens if I find out I have a shortfall and will run out of money?

If you find a shortfall in meeting your retirement spending goals, you might still be able to retire - it’s just that you’ll have to tweak a few variables:

- Increase your income: assuming you’re still working and haven’t yet retired, picking up other jobs and considering other sources of income can supplement your savings and meet the shortfall gap of retirement savings.

- Decrease your expected expenses: By returning to the drawing board and re-estimating your expenses, you may still be able to retire (just not how you initially thought). If you can reduce discretionary expenses on things like travel (for example, taking two international trips each year rather than four), you might still be able to keep the same quality of life but remove some of the non-essential things you don't need.

- Delay your retirement date: by prolonging your retirement phase, you not only need less money (as you'll likely still live the same length of time - but just have fewer years in retirement), but you also can continue working past age 65 (or whatever date you set as your retirement date)

Why do I need to plan my retirement drawdown? Isn’t NZ Super and KiwiSaver enough?

Even if your KiwiSaver balance is more than large (say NZD 5 million) to cover any living expenses, it still makes sense for everyone to plan their retirement drawdown.

Learning the best ways to sell down assets and withdraw living expenses (while making sure not to have too much or too little set aside) is a skill that needs to be learned at any wealth level.

Learning the best ways to sell down assets and withdraw living expenses (while making sure not to have too much or too little set aside) is a skill that needs to be learned at any wealth level.

Other Related Retirement Guides, Graphs and Insights

Financial Independence Guides:

Related Guides:

Financial Independence Guides:

- Retirement in a Nutshell

- How to Retire Early

- FIRE Explained

- Five Types of FIRE Plans

- Getting FIRE’d in New Zealand

- FIRE and NZ Real Estate

- Achieving Financial Independence, Faster

- The Four Percent Rule for FIRE - The Definitive New Zealand Guide to a Financially Secure Retirement

Related Guides:

- Managed Fund Fees Calculator

- Our Favourite KiwiSaver Funds

- Our Favourite Managed Funds

- Our Favourite ESG Investments

- Maximising Income in Retirement in New Zealand

- The Best Retirement Income Products in New Zealand - Funds, Term Deposits and Bonds.

- Massey University New Zealand Retirement Expenditure Guidelines

Concluding Comments: Retirement spending is broken down into fixed, variable and legacy:

Source: JP Morgan Guide to Retirement (page 44).

Whether New Zealanders want to continue growing wealth, preserve wealth (e.g. just spend the “interest” and not touch the principal) or spend down the principal.

Whether New Zealanders want to continue growing wealth, preserve wealth (e.g. just spend the “interest” and not touch the principal) or spend down the principal.

Source: JP Morgan Guide to Retirement (page 45).

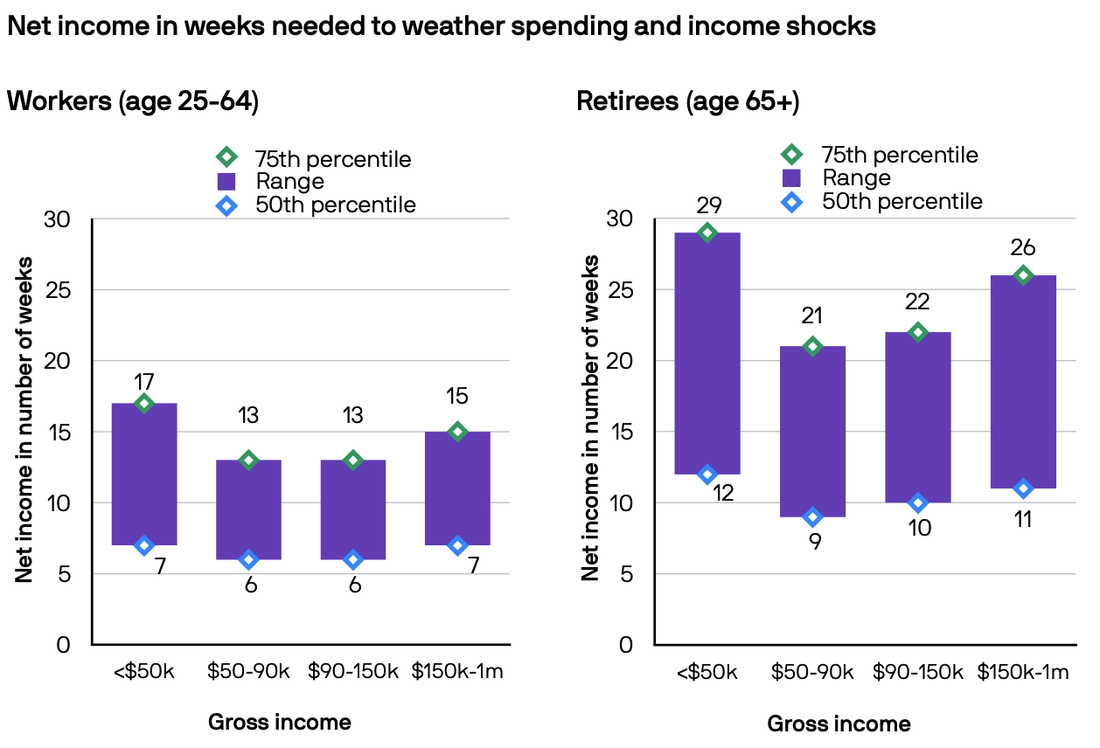

How much income should retirees have set aside to adjust to shocks in income/spending?

How much income should retirees have set aside to adjust to shocks in income/spending?

Source: JP Morgan Guide to Retirement (page 49).